The private credit boom is shaking up conventions in derivatives markets, providing an opening for banks without large lending books to win more corporate hedging transactions.

Private credit funds have swelled in recent years, with the largest of these investors now able to deploy enough capital to compete against banks’ syndicated loan desks on many deals. That has had a knock-on effect on one of banks’ mainstay businesses: selling corporate clients derivatives to hedge their debt payments against moves in interest rates or currencies.

Borrowers traditionally traded these derivatives with one of their relationship banks as a reward for lending them money. But the emergence of direct lending has disrupted this practice, with most private credit funds unable to offer hedging capabilities. That, in turn, is sparking fierce competition among banks not involved in the loan deals to provide what have become known as “orphan” hedges.

"We’ve certainly seen an increase in situations where borrowers are not using their lender for their hedging,” said Jackie Bowie, head of EMEA at consultancy Chatham Financial. “If a bank is providing your lending, that typically influences who you end up doing your hedging with as there’s a relationship play there. As more borrowers are not completely reliant on their relationship banks, they're more likely to go to market for their hedge.”

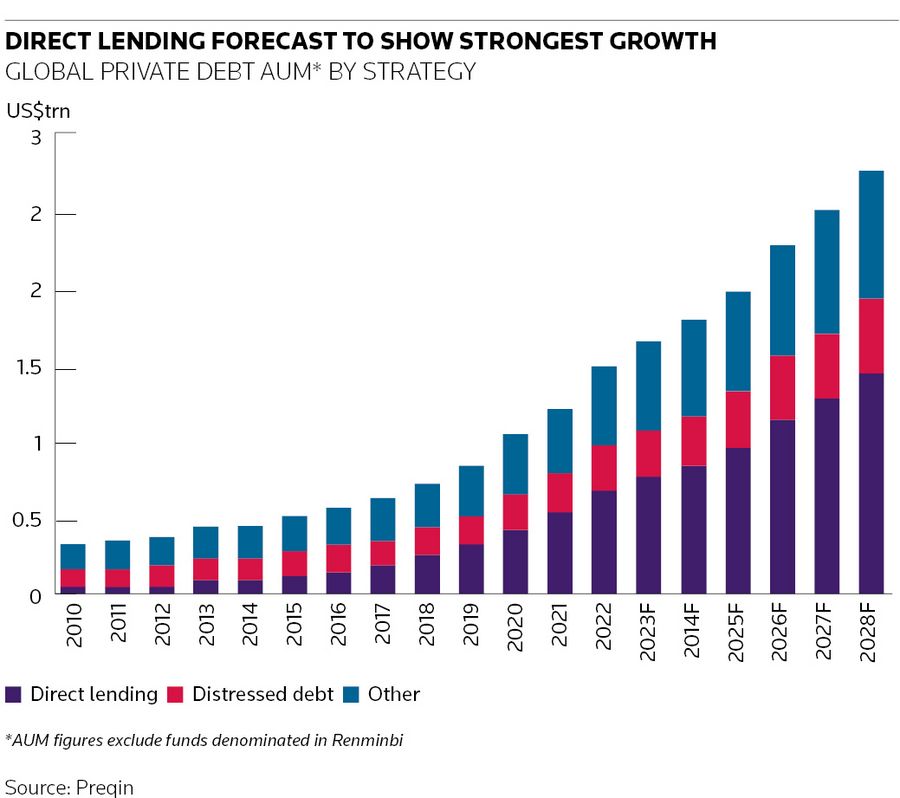

Assets in private credit funds have nearly doubled since 2020 to US$1.6trn and are expected to grow to US$2.3trn by 2027, according to an AllianceBernstein analysis of Preqin data. That firepower has allowed direct lenders to encroach on banks’ core business of lending money to companies and the inability of private credit funds to offer derivatives to the companies they lend money to has left a void for banks to fill.

No loan, no problem

The resulting growth in “orphan” hedges has upended the cliche of banks having to lend money to corporate clients in order to win higher margin business such as selling them derivatives. That has been particularly helpful for banks that have slashed back lending books in recent years but remained active in derivatives markets, where strict regulations and expensive infrastructure ensure the barriers to entry remain high.

“There are many banks out there in a similar position to us that have a very strong derivatives franchise but a reduced focus on lending, so this trend is one that suits us well,” said Adrian Bracher, global head of macro structuring in global markets at UBS.

Bowie said several banks have looked to increase their market share in providing interest rate caps, a simple form of derivative where borrowers can pay an upfront premium to shield against rising interest rates. Third-party hedging advisers often run a competitive pricing process for these trades.

“The volume of inbound requests related to standalone hedging has been increasing for years,” said Andrew Moreton, head of interest rate sales at Investec. "It is a competitive marketplace. For simpler, commoditised deals the winning banks tend to be those names who can be ready to trade swiftly and who will be reliable in delivering agreed pricing.”

Some large banks are also offering interest rate swaps as orphan hedges, which are often longer-term contracts and involve the bank taking more counterparty credit exposure to the company on the other side of the trade.

Deal upturn

Private equity backed companies are some of the most prominent users of direct lenders, making them an obvious candidate for orphan hedges. Many analysts are expecting an upswing in activity from private investors more generally this year amid signs of a brightening outlook for mergers and acquisitions. Global M&A volumes are up 38% so far this year after hitting a decade low in 2023, according to LSEG data.

“As the dealmaking cycle continues to turn, there is a growing spillover effect into financial markets,” said Daniel Aksan, co-head of European rates sales and trading at Morgan Stanley. “Increasingly, any sort of private market transaction – whether it’s M&A, private equity, or a private credit trade – requires some sort of hedge now that people are a lot more alert to interest rate risk than they were before.”

Some banks are already seeing an increase in demand for more complex transactions popular among private investors. Those include deal-contingent trades and pre-hedges, where companies look to hedge their interest rate or FX risks ahead of a major transaction closing.

“Often clients who are looking to hedge a loan aren’t just in need of derivatives for that specific loan. They’re often looking for a full suite of derivatives and hedging services, which we’re happy to provide even though we’re not lending to them,” said Bracher at UBS. “There’s definitely still cross-selling opportunities available from providing only a hedge, not the loan, to clients.”