The renminbi’s overseas push may have taken a back seat to China’s monetary easing, but the currency’s global importance can only grow in the years to come.

China’s currency is no longer a fledgling tender. For better or worse, the renminbi will define the 21st Century, just as the US dollar and pound sterling embodied the two that preceded it. Yet, many questions remain unanswered. How fast is it growing? What are the obstacles holding it back, and the incentives fostering its development? Also, what does Beijing really want its increasingly global currency to become?

So far, it has been surprisingly smooth sailing. The turbulence that typically accompanies a rapidly developing currency has been kept to a minimum, thanks to the creation of an onshore (CNY) and an offshore (CNH) renminbi, with a thick wall of capital controls separating one from the other.

The widely held assumption that Beijing’s ultimate plan is to reunite the two to create a single universal currency, has encouraged the development of a thriving offshore market. Outstanding Dim Sum debt, as the offshore bond market is known, has risen steadily over the past eight years to hit Rmb564bn in 2014, according to Standard Chartered. Primary renminbi debt issuance in Hong Kong last year nearly doubled to Rmb202bn, data from Bank of China (Hong Kong) show.

Moreover, the renminbi is being used every day, and in every way, to settle commercial trades. Data from payment messaging network SWIFT show the renminbi jumping from the 20th most commonly used global currency in January 2012, to the fifth most widely used as at end-2014, leapfrogging the Australian and Canadian dollars. In December 2014, the renminbi accounted for 2.17% of all global payments, against just 0.25% three years previously.

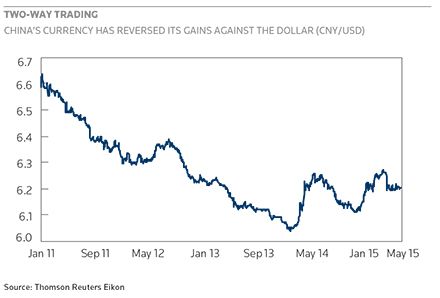

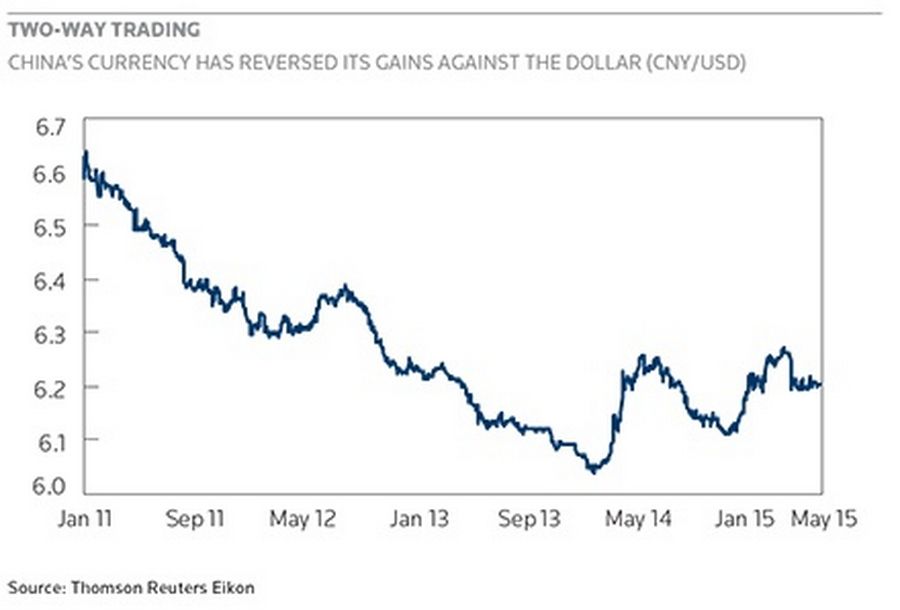

Two-way trading

Christy Tan, a currency expert and National Australia Bank’s Hong Kong-based head of markets strategy, reckons that up to 35% of all annual trade with Chinese corporations will be conducted in renminbi by the end of the decade, against 22% last year.

It will not always be plain sailing. China’s determination to create a global currency opens huge new opportunities for the country’s leaders, but also imposes on them new responsibilities – a burden they may not entirely be ready to bear.

“RMB liquidity must be fostered outside Hong Kong and Asia to support investors’ confidence in trading in these assets on a daily basis – addressing both time-zone differences, and daily clearing and settlement needs.”

A series of onshore rate cuts suggest the currency is in for a rocky 2015. The Dim Sum market’s recent expansion benefited from allowing borrowers to raise money cheaply in Hong Kong. Yet, that trend is likely to end this year, due to sharply higher funding costs, a weaker currency, and a sprinkling of bond defaults by mainland corporations. StanChart’s projection is for outstanding offshore bonds to shrink to around Rmb480bn–Rmb500bn this year, with HSBC forecasting around Rmb520bn.

The challenge for China is to find a way to open up the renminbi without allowing too much chaos and uncertainty to penetrate a cooling economy. In order to create a global currency, says David Olsson, banking and finance partner at Hong Kong-based law firm King & Wood Mallesons, China “still needs to develop accessible, deep and broad domestic financial capital markets. This is a precondition to RMB convertibility.”

Beijing is heading in that direction, enforcing rules designed to permit local capital to move offshore, while allowing foreign investors to shunt money into domestic securities. A “through train” scheme now allows shares to be traded between Hong Kong and Shanghai. New free-trade zones are being set up in Fujian, Guangdong and Tianjin, following in the footsteps of the Shanghai pilot. In early May, Beijing approved applications from HSBC, Morgan Stanley and 30 other foreign institutions to invest in the Rmb36.3tn onshore bond market.

Every one of these developments, notes Scott Farrell, a securitisation and derivatives partner at King & Wood Mallesons, is key to China’s long view of its currency.

“Each reform serves to test elements of an international currency,” Farrell said. “While the sequencing of reforms may not be the same as some might have expected, this is not extraordinary. China is going to internationalise its currency in the way in which it chooses: it can afford to.”

Global reserves

October is the next key date in the currency’s development as that is when the International Monetary Fund will decide whether or not to include the renminbi in its basket of Special Drawing Rights (SDR). Beijing has lobbied the IMF hard on this and for good reason. Inclusion in the SDR basket, Olsson notes, will “give greater credibility to the RMB. Global investors will, over time, have no option but to include a greater proportion their allocations in the Chinse stock market.”

Adding the renminbi to the basket is a tough call. On the one hand, IMF rules demand that any SDR currency must be freely usable. (The renminbi is not). On the other, the next time the basket will be evaluated is 2020. Wait that long, and the Chinese currency’s clout and weight may well destabilise the SDR’s fragile mechanism.

Wei Yao, chief China economist at Société Générale, reckons there is a “50-50 chance” of the renminbi making it in this time. “If it is included, it will require some bending of rules,” he said.

With an 85% approval rate required for inclusion, Washington, the IMF’s biggest shareholder, will control the swing vote.

Then, there is the issue of including Chinese A shares in the MSCI indices. Many expect this to be a case of “when” rather than ”whether”. Evan Goldstein, global head of renminbi solutions at Deutsche Bank, says inclusion in the MSCI will “certainly have an impact on overseas asset managers’ holdings of domestically listed Chinese equities”.

More overseas investors are also likely to plough into onshore bonds. Foreign institutions owned just 2% of domestic Chinese debt at end-2014, according to data from the People’s Bank of China, against half of all US Treasury debt.

This will not happen overnight as foreign investors need to believe that Beijing is committed to cultivating deep, well-stocked capital markets.

“There must be more RMB-denominated assets available offshore for investors to build up a position in the currency,” said Deutsche’s Goldstein. “RMB liquidity must be fostered outside Hong Kong and Asia to support investors’ confidence in trading in these assets on a daily basis – addressing both time-zone differences, and daily clearing and settlement needs.”

A key boost to the currency should come from the offshore renminbi hubs being set up from London to Frankfurt and Singapore to Sydney. At least 10 new currency centres are to be launched this year, with an emphasis on emerging markets strongly wedded to China’s economy.

“It is likely that a number of (the new hubs) will be in countries targeted by China for the New Silk Road” stretching from Beijing to Europe through Russia and Central Asia,” said King & Wood Mallesons’ Olsson. “Having new development banks will support this initiative, as well as boost the acceptance of RMB in those regions.”

Olsson also highlights an increasing sense of collaboration, rather than competition, between these offshore trading hubs, pointing to ongoing discussions between Hong Kong and Sydney for new ways to enhance cross-border clearance and settlement mechanisms. “There is now much more willingness and desire for centres to focus on ways in which they can work together and also drive their own domestic market reforms and initiatives,” he said.

Trust issues

The renminbi still faces a slew of challenges, as well as opportunities. On the one hand, the currency will become more volatile as it matures. When the capital account opens (the official target is 2020), “you won’t see a big bang, but you will see much more volatility in terms of FX movement,” said Christy Tan, head of markets strategy at National Australia Bank in Hong Kong.

Trust issues also remain, notably when it comes to the relationship between onshore lenders and offshore investors. “The bulk of foreign corporates are hesitant to engage local banks, so there is a lingering trust issue there,” said Tan. “There’s room for improvement there.”

On the other hand, corporate treasurers are becoming ever more comfortable dealing, trading and funding in renminbi. Foreign issuers, including German development bank KfW, French carmaker Renault and the financial services division of US heavy equipment maker Caterpillar, have sold renminbi-denominated debt over the past six months. NAB’s Tan points to companies becoming “increasingly comfortable pooling cash in RMB and remitting it out of China. Looser regulations also help corporates overcome operational challenges.”

China’s leaders have a few more cards up their sleeves. The new development banks Beijing is leading or creating, notably the Asian Infrastructure Investment Bank, will more firmly embed China and its currency into the global financial economy, with AIIB-led financings, particularly in frontier markets, likely to be priced in renminbi.

The long view on China’s currency is harder to see. So many hazards and pitfalls remain – from how to open the capital account to the timing of full current account liberalisation. Unspoken in all of this, in part because Beijing speaks more about narrow ambitions than about broad concepts, is what the country’s leaders want from its currency. Does Beijing want the renminbi to become one of the world’s two most-traded units, alongside the US dollar? Is it all about creating a currency that can accompany mainland corporations and citizens, wherever they roam – or turning the renminbi into a favoured denomination for financial products issued both onshore and offshore?

King & Wood Mallesons’ Farrell believes the answer is all of the above and more, with China’s ambitions stretching far beyond mere currency-related goals.

“The liberalisation of the RMB is fundamental to the deregulation of exchange rates and interest rates in China; to the creation of liquid markets for managing risks in China; and to creating developed domestic financial markets that are open to the world,” he said.

“These goals serve China’s overall reform agenda, as well as serving an economy in the process of transitioning to a dependency on consumption, not manufacturing.”

To view all special report articles please click here and to see the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com .