Efforts to connect emerging Asian issuers with conservative Japanese investors have proven frustrating, but Abenomics is giving the yen a bigger role in funding Asian growth.

The Japanese yen presents an attractive option for international borrowers, offering ultra-low yields in a depreciating currency. So far, Asian issuers have been rare visitors to the yen debt capital markets, but recent activity suggests this may be about to change.

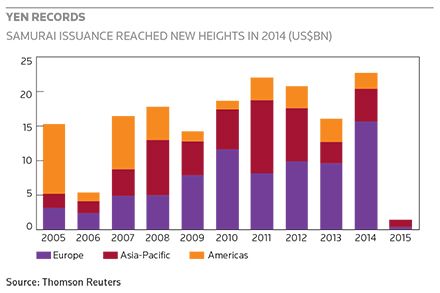

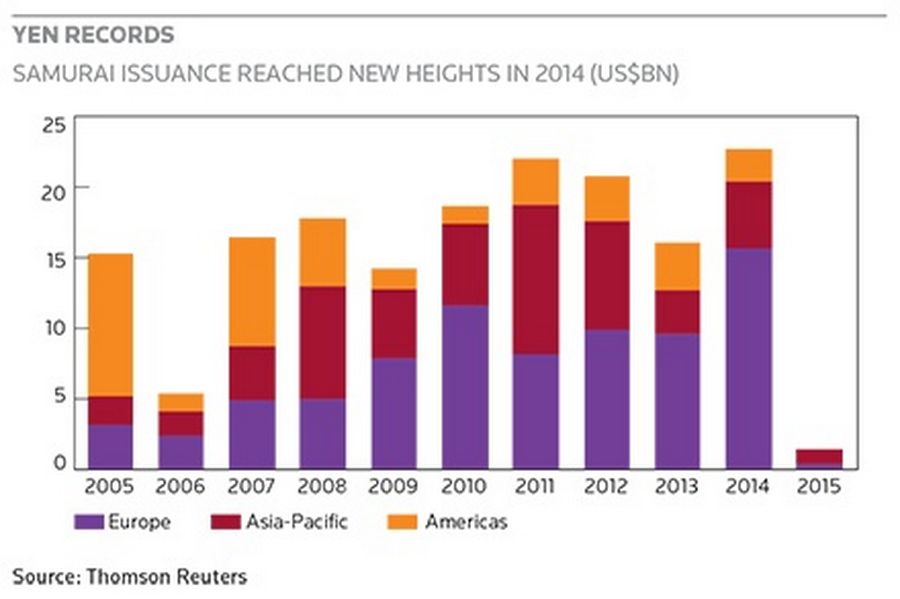

The Abenomics regime, the brainchild of Prime Minister Shinzo Abe, has created a bullish structural backdrop for yen issuance, thanks to a massive monetary stimulus, low interest rates and a concerted effort to weaken the yen. As a result, the Samurai issuance in calendar 2014 jumped 57% to a record ¥2.62trn (US$22.0bn).

“We see the high pace of issuance continuing this year given the relatively high spread of Samurais versus domestic yen paper. And because yen yields are at historic lows, we see Japanese investors widening their investment target in the quest for yield,” said Kenichi Kanda, head of international debt origination at Daiwa Securities in Tokyo.

Still, despite a radical policy backdrop, the essential flavour of the yen bond market remains intact: it is a high-grade market, where issuance from financial institutions is dominant. Abenomics has forced investors to search for higher yields, but fund managers remain extremely conservative, leaving the lower rungs of the credit ladder off limits.

Yen records

“The yen long-term offshore funding market is more or less of the same nature as it has been over recent years. It is dominated by FIG and anything below investment grade still remains very challenging,” said Steve Apted, head of debt syndicate at SMBC Nikko in London.

Nevertheless, with the perception taking hold among Japanese investors that the yen is set to weaken further over the next couple of years as Abenomics remains in place, the mindset among investors is changing.

“There has been a greater receptiveness towards offshore fixed-income assets from the Japanese investor base as the yen has weakened. Japanese investors continue to diversify, both in terms of credit and currency. In the Samurai space, this trend has manifested itself in terms of larger deal sizes,” said Apted.

Test drives

As the new fiscal year gets under way, two Samurai offerings from Asia have raised hopes of more from the region. Maybank was in the process of pricing a bond as this report went to press, while the Republic of Indonesia is preparing a return to the Samurai market, with partial backing from the government’s Japan Bank for International Cooperation.

Also working in favour of potential Asian issuers is the gap left by the absence of US bank issuers – traditionally big providers of Samurai supply – as they work through compliance issues with Japanese regulators surrounding the US Foreign Account Tax Compliance Act. FATCA is the US tax authorities’ attempt to reduce monies lost to US citizens’ offshore tax non-compliance.

Recent developments have also created an easier path for potential issuers. The yen Pro-bond market has emerged as an alternative for foreign issuers looking to access Japanese investors.

While the Samurai format is cumbersome, requiring extensive documentation in Japanese, the Pro-bond format allows overseas issuers to sell yen bonds simply with the registration of an existing MTN programme with the Tokyo Stock Exchange.

Maybank took that route with two Pro-bonds – for ¥31bn and ¥20bn – and its planned Samurai brings forth the intriguing possibility of a new template for issuance in yen. To coin the phrase of a Tokyo syndicate head, Asian issuers can “test drive” the idea on the Pro-bond market, before graduating to a full-blown Samurai programme if demand justifies the effort.

Certainly, the Pro-bond market is no match for Samurais when it comes to size. A handful of the biggest Samurai investors have yet to embrace the format, and Tokyo bankers see ¥30bn and a three-year tenor as the limits of the Pro-bond investor base.

A Tokyo-based DCM head at a European bank suggested that Indonesia’s forthcoming Samurai would provide a definitive test of the yen bond market’s to move down the credit curve.

While JBIC has guaranteed the principal and part of the interest for all of Indonesia’s previous Samurais, Indonesia is expected to roll out a partial guarantee as it begins to market itself as a standalone credit.

Indonesia is rated Baa3/BB+/BBB–.

“Moving into Double B territory is going to be a challenge and, if successful, the deal will mark an opening up of the credit mentality among Japanese investors,” the DCM banker said.

“It’s about time that Japanese investors seek out new playgrounds away from the usual European and Latin American sovereigns. As far as Asia is concerned, likely candidates in that regard are the Philippines and Thailand.”

The first quarter of 2015 got off to a slower start than the same period last year, something which bankers partially attributed to a less than benign basis swap. At five years, the yen/dollar basis is minus 65bp and the yen/euro basis is minus 30bp. That is around 20bp worse than six months ago for issuers looking to swap yen proceeds into dollars or euros.

“The worsening basis would have kept some issuers away, but I think also it was uncertainty about whether the Fed would tighten rates and a wariness among investors that explains the slower start,” said the DCM head.

To view all special report articles please click here and to see the digital version of this report please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com .