Banks and investors are finding that the derivatives business can pay dividends amid an uptick in volatility and higher trading volumes.

There is far more to Asia’s equity capital markets than initial public offerings. That’s just as well, given the disappointing volumes and sliding fees in Hong Kong and China IPOs – the traditional engine of any Asian ECM franchise. Most of the equity derivatives business goes on behind the scenes, and the decline in trading volumes that followed the 2008 financial crisis had forced many banks to scale back their ambitions in the sector. But the use of warrants and more complex products in some unusual recent fundraisings shows the asset class remains as important as ever – perhaps even more so.

When Thai tycoon Dhanin Chearavanont’s Charoen Pokphand Group needed to finance the bulk of a US$9.4bn purchase of a stake in Ping An Insurance Group in January at short notice, his advisers at UBS constructed a margin loan backed in part by shares in other listed companies in the CP Group, such as CP All and CP Foods.

The financing package, said to total around US$5.5bn, came with a series of equity options designed to protect both Dhanin and UBS from big swings either in the stock prices of Ping An or in the shares posted as collateral.

Multiple banks participated in the share-backed financing, and UBS is understood to have managed much of its equity exposure by structuring related products to distribute to its private client base.

While the Ping An trade is by far the biggest example in the Asia Pacific in the past decade – some say on record – many other investors have turned to similar corporate equity derivatives to build stakes, or to hedge or monetise their existing positions.

Certainly, business has been picking up in recent months, said Siddhartha Hari, head of strategic equity derivatives for Asia at Barclays.

“An increase in M&A activity is often one of the biggest motivations, as derivatives can allow investors to use leverage and hedging strategies to manage risks when they are building a stake.”

Transactions in the private space can be larger, and banks face less pressure to split fees with dozens of their rivals – an increasingly common feature of the public equity market. There is no league table to worry about, another benefit to those who work behind the scenes, and business continues whether the public markets are open or not.

“The derivatives market tends to counter-balance the cash business, and it can ride on the back of trends and emerging flows,” said Hari.

The recent slump in debt capital markets issuance following a spike in US Treasury yields has also added to the appeal.

“There’s a strong pipeline. With credit spreads up 200bp–300bp in high-yield bonds, the idea of using shareholdings to bring down the cost of borrowing is more attractive now,” said Sue Lee, co-head of Asia Pacific strategic equity solutions at Citigroup.

Lucrative

Deals can be incredibly lucrative. UBS won’t comment on the Ping An trade, but the bank’s global ECM revenues more than doubled in the first quarter. Its earnings statement said the near US$300m increase reflected “the result of a large private transaction”.

Fee opportunities have not gone unnoticed, especially at a time when revenues from public capital markets financings are under pressure. While many banks have cut derivatives teams since the 2008 crisis, signs of investment are emerging in the institutional-focused, strategic derivatives business.

“Jumbo deals are a feature of this business. Most of the opportunities come from more flow-type transactions, but often a structure can be adapted to suit a certain set of circumstances, and deal sizes can be very large,” said Stephen Albutt, co-head alongside Lee at Citigroup.

Societe Generale recently hired Catherine Bradley as head of its strategic transactions group, Asia Pacific, focusing on equity derivatives. Until last year, Bradley was head of Credit Suisse’s equity-linked solutions group in Asia Pacific.

Deutsche Bank, meanwhile, is moving Keyvan Zolfaghari, its head of strategic equity transactions for EMEA, to Singapore to lead the same group for Asia Pacific, focusing on corporate equity derivatives as well as equity-linked capital markets.

Citigroup recently recruited Vincent Au, another former Credit Suisse banker, and has plans to expand its corporate derivatives business further.

“The strategic equity transaction business is important in getting to clients first. It’s extremely competitive, because it can strengthen key relationships that then feed secondary volumes,” said Timothee Bousser, head of global equity flow, Asia Pacific, at Societe Generale.

“It’s also a way to leverage the strength of a top flow business in the primary market. Volumes are key in cash equities as the fixed costs are huge, and you need to be one of the top houses to really be profitable.”

Volume boost

Declining volumes in recent years had left many international players facing difficult decisions over the future of their cash equities business in Asia.

“The retail structured note side has always been the biggest part of the primary derivatives market, and that forced some banks to cut back dramatically when volumes there fell a lot,” said one derivatives specialist.

“Business has traditionally been driven by the big European houses, while the US firms focus on more niche products or don’t have a big Asian presence. But it’s changing. We’re seeing more US firms coming in, possibly because they have access to cheaper funding.”

Equity businesses remain plagued by high fixed costs and thin margins, leaving banks highly dependent on volumes. After years of decline, however, trading data in Asia have again turned positive.

Hari at Barclays believes emerging-market equities are once again returning to favour, despite the recent sell-off.

“The principal desks in banks may have decreased their risk-taking, but there are many big long-only funds and private equity houses that have filled the void,” he said.

Average daily turnover in Hong Kong securities for the first five months of 2013 is up 16% on the same period last year at HK$68.2bn (US$8.8bn), with derivatives contracts also registering an 8% increase, according to HKEx.

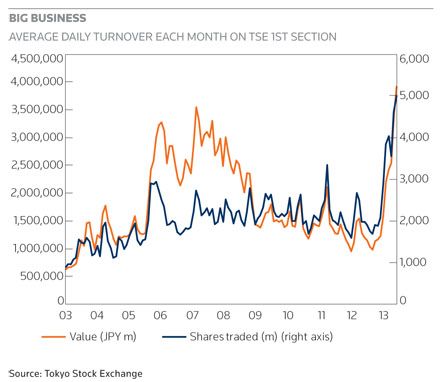

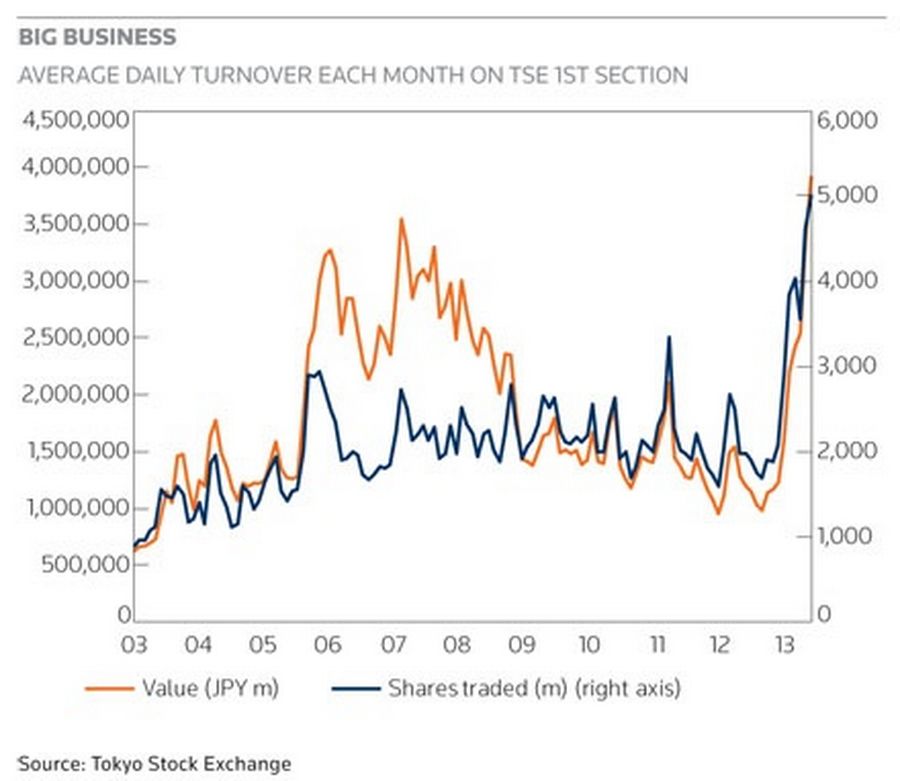

The first five months of 2013 have been the busiest on record on Tokyo’s main board, as measured by the average number of shares changing hands each day. By value, turnover in May 2013 beat all records, with a daily average of ¥3.9trn (US$39.7bn) topping the market’s 2007 peaks.

Resurgent Japan

If any single trend has united the Asian equity markets, it is the resurgence of interest in Japan.

“Notional volumes and number of deals were declining in recent years and hit a low last year, but then the Japan rally has brought a lot of interest back. Investors have cleaned their books, and appetite is coming back from those looking to monetise or hedge their positions,” said Bousser.

Enthusiasm for Prime Minister Shinzo Abe’s fiscal and monetary reforms powered a nearly 80% gain in the Nikkei 225 index in six months to May 22. Recent moves have cast some doubt as to the sustainability of that rally, with the index down 17% in the next month, but while investors have adjusted their trading strategies, volumes remain elevated.

“When Abenomics began after the third quarter of 2012, the retail products that had dominated the market meant that Japan was looking very cheap, both in terms of volatility and valuation. When the Nikkei was at 11,000 people were buying calls at 18,000 to get long volatility and upside,” said Bousser. “That trade worked very well.”

“Investors are still bullish on Japan but we’re seeing a lot more buying hedges, and the game now is all about volatility.”

The enthusiasm for Japanese derivatives has allowed early-stage growth companies to raise funding that may otherwise have been off the table.

Some smaller companies, for example in the biotech industry, have used private warrants to access new capital at a better price. In such a deal, the arranging bank will typically take the equity risk on its own principal book before repackaging the exposure for investors.

If Abe’s policies succeed in stimulating inflation, companies will no longer be able to borrow at zero rates. That shift in debt yields may also play into the hands of alternative structures.

Emerging opportunities

Replicating the success of derivatives strategies in the wider region remains difficult. Only a handful of stocks beyond Hong Kong, Tokyo and South Korea are liquid enough for options to be cost-effective, and derivatives rarely feature on public financings.

Two exceptions to that rule came earlier this year in Singapore, when under-fire commodity trader Olam International and cash-strapped Tiger Airways combined equity options with rights issues to maximise their access to capital. Olam added warrants, while Tiger offered convertible bonds.

Bankers aren’t expecting such structures to become a trend, but they note that deeper liquidity is creating more opportunities as regulators enforce free-float rules and as more funds shift from debt to equity.

The Philippines, for instance, boasts a far deeper equity market than it did before regulators imposed a 10% minimum free float requirement. Primary capital raisings are getting bigger. India, too, has insisted that private sector listed companies maintain a free float of at least 25% since the start of June.

“Liquidity is the lifeblood of our business,” said Albutt at Citigroup. “The Philippines is still relatively illiquid, and India is highly regulated, but it’s at a starting point. It’s a move in the right direction, but not a game-changer yet.”

While bankers elsewhere are feeling the pressure from newly empowered regulators, little has changed in the strategic derivatives business. Basel III and Dodd-Frank rules have had a muted impact on liquidity, and equity bankers are accustomed to complex compliance rules.

“Since retail and other minority investors have a big role in the equity markets, the regulators have always been very mindful of protecting their interests and have always had rules in place, even pre-crisis. The regulatory burden hasn’t increased substantially since the financial crisis,” said Hari.

To see the digital version of this report, please click here.