The Taiwanese chip packager has launched Asia’s first corporate Green bond, pioneering the development of a new market for socially responsible investing.

In search of green shoots

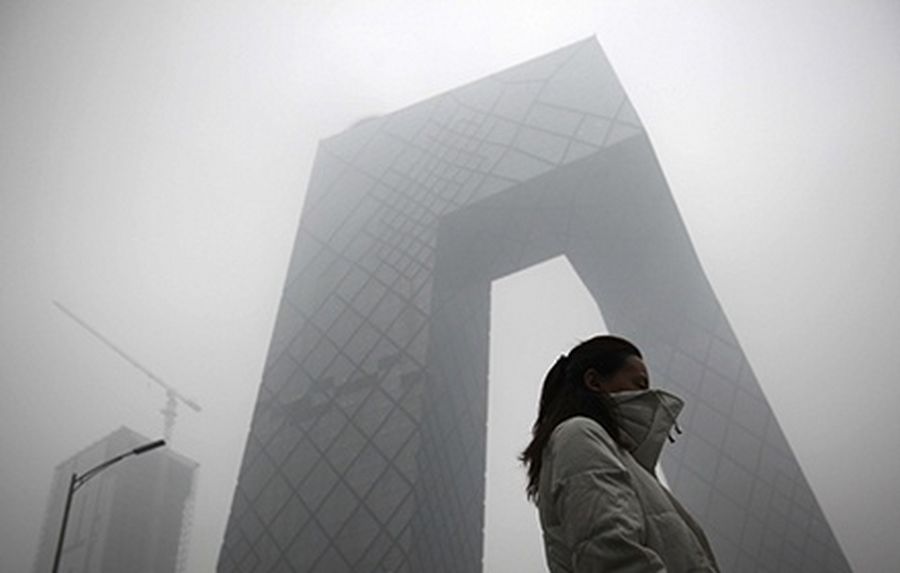

Source: REUTERS

A woman walks past the new China Central Television (CCTV) building amid heavy fog in Beijing.

Climate change now tops the agenda in Asia, with China, India and Japan, which together account for over a third of global emissions.

In Beijing, heavy smog is now a common sight and, in Japan, the need for renewable energy took on a new significance after the 2011 Tohoku earthquake threatened the stability of the Fukushima nuclear power plant.

Financial markets are also beginning to respond to the growing demand for environmentally sustainable investments. Green bonds are becoming an alternative source of funding for issuers looking to finance projects that support renewable energy and other low-carbon projects, offering a chance to diversify into a new investor base.

Although issuance in Asia has been tepid so far, the global enthusiasm for the product is starting to reach Asia.

Taiwan’s Advanced Semiconductor Engineering provided some regional momentum in July with the first Green bond from Asia’s corporate sector, raising US$300m of three-year money.

ASE is the world’s largest independent provider of semiconductor packaging and testing services, based on 2013 revenues. In the competitive industry, it has been positioning itself as a low-carbon, climate-friendly company, giving it a strong incentive to issue a Green bond.

The company also had an additional motive – to repair its environmental image after the Kaohsiung City Environmental Protection Bureau fined it NT$110.0m (US$3.7m) last October for dumping waste water into the environment.

“Aside from fundraising, we wanted to make a statement to show that we are really committed to helping the environment and energy-saving efforts,” said Joseph Tung, chief financial officer at ASE. “We were able to get our message across, since we were the first corporation to do this in Asia.”

Green bond issuance has hit US$26.2bn so far this year, according to the Climate Bonds Initiative. That is more than double the volume for all of last year, when it hit US$11bn. HSBC expects the outstanding Green bond volume to reach as much as US$60bn at the end of the year and to exceed US$100bn next year.

However, while investors and issuers are showing more interest, the product has yet to become fully established as a source of corporate funding. Issuing a Green bond costs the same, if not more, than conventional paper.

ASE had to pay around 30bp over its local currency funding levels for its Green bond, Tung said. That was a cost the company was willing to pay for marketing purposes, but other issuers may not have the same needs.

“If it’s purely for fundraising, then a Green bond doesn’t make a difference,” said Tung. “We had a specific purpose.”

Green bonds also require companies to receive third-party approval for the projects they will finance, a process that can take the issuer a few months.

“Aside from fundraising, we wanted to make a statement to show that we are really committed to helping the environment and energy-saving efforts.”

ASE already knew which projects it would be using the proceeds on, which meant that receiving approval for their use of proceeds from Oslo-based Center for International Climate and Environmental Research (Cicero) was relatively fast, only taking about a month.

Even then, the Taiwanese chip company had to answer questions from the agency about its projects, as well as provide numerical proof of how much energy it would be saving. ASE is also required to provide regular updates to bondholders on how the proceeds are being used.

For some Asian issuers, a longer process and a lack of pricing competitiveness could make it harder to justify issuing a Green bond.

“There needs to be more issuer education,” said Daniel Kim, a banker at HSBC. “They’re not pressured to do one, but it does provide them with a more diverse investor base.”

At least on the other side of the globe, Green bond issuance is growing rapidly, and bankers are optimistic that Asia will catch on.

The Development Bank of Japan is poised to sell its first Green bond, and is targeting Asia’s first euro-denominated issue. The first Green issue from Asia came last year, when Export-Import Bank of Korea set the precedent with a US$500m five-year print.

According to HSBC’s Kim, the way to build things is for higher-rated credits to kick off issuance before going down the credit spectrum and opening the doors for blue-chip companies.

Once the market develops further, China presents a significant opportunity for Green issuance, says Kim. Manufacturers of electric cars and batteries, as well as power companies looking for renewable energy projects, are all contenders for potential issues.

Greenhouse gas emissions have risen to unprecedented levels this year, according to findings that the Intergovernmental Panel on Climate Change, a UN body that studies the environment, published in April.

The hope is that governments and companies will be able to attract sufficient funding to construct buildings, plants and facilities that will help decrease the release of harmful chemicals and protect the environment before it is too late.

To see the digital version of this report, please click here.