IFR ASIA: We’ll move on now to a special session on green finance. Sandeep, what recent developments have you seen in Green finance, and what’s going on here in India?

Sandeep Bhattacharya, CBI: In India the capital markets have been blessed by some recent INR bonds that refinanced green projects, mostly from renewable energy developers. When this trend started in 2015, the underwriters used to say that partially guaranteed instruments were very difficult to sell down. I am happy to say that they were singing a different tune on the one that got placed in January!

We have had a fair amount of issuances from large public sector borrowers, and the pioneer was EXIM Bank, of course. Then we had IREDA, NTPC and IRFC [Indian Railway Finance Corporation] who then followed suit and did offshore issuances. Some of them were Masala, some of them were US dollars.

EXIM Bank started off with mass transportation, but the asset mix is heavily weighted towards renewable energy with a little bit of Green buildings and a little bit of mass transportation with the IRFC deal.

If you go beyond the capital markets, there is increasing acceptance of financing of equipment, like solar recharging systems. There are plenty of relatively small finance companies doing risk business there, and I must say that the size of the equipment is getting larger and larger. What started off with mobile phone chargers is going up to maybe a whole housing system and these non-banking financial corporations are keeping pace. Of course their balance sheet sizes are still small. They still need to scale up a bit.

There is intense demand for rooftop solar systems but practically no financing. So what the smaller operators are doing is setting up equipment and selling it to the big developers, and in the process strengthening their competition. There is a huge dearth of financing there – it comes from crowdsourcing, maybe some wealth management firms. In fact Barclays wealth management has done a good job of financing the equity of some of these SPVs which do rooftop solar.

There are a plethora of business models and I must say it is difficult for financial institutions to keep pace with the different models. There’s a tremendous demand but a huge financial crunch.

This is the Indian scenario. It’s very different from what you’re seeing in Europe. Investors are all over the clean stuff. The next step there is looking at Green bonds from the ‘dirty’ industries, which means the refineries, the metal extraction companies that are transitioning to a business model which aligns with the Paris Agreement.

There’s a fair amount of capital available, and a lot of Indian companies have tapped it, but in India we are still dealing with a lot of basic needs for water, for agriculture. They are at a very start-up stage and a bit far away from the capital markets.

IFR ASIA: David, I think this is a good one to bring you in on. Can you tell us a little bit about EXIM’s experience in the green market and what you take away from that?

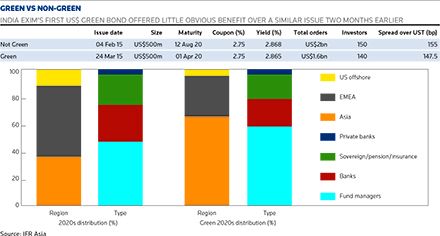

David Rasquinha, India Exim: We have a couple of takeaways, and the first one is probably going to be music to Sandeep’s ears and that is I would say get a good certification.

I’m not entirely happy with the advice we received when we did India’s first cross-border Green bond. We did not get a certification done. Call it a bit of, not exactly arrogance, maybe a bit of overconfidence; we thought our word was good enough. We didn’t know the market. Frankly, it was the first Green bond out of India, we were getting our feet wet in the market and we went ahead with full disclosure.

We disclosed the mass transportation projects that we wanted to fund, as Sandeep mentioned. These are cross-border in Bangladesh and Sri Lanka. We explained why they could be perceived as green, because of the shift from high-intensity road transport to lower-intensity mass transport. We gave all the details but it was essentially our word.

We also offered an audit certification regarding the use of funds. Now when we commenced the marketing, we didn’t really do a roadshow. We just did a series of telephone calls which, again, suggests to you that we probably should have done a bit more homework and taken a lot more care. We found that the green investors had a lot more in-depth questions than we were prepared for. It’s not that we didn’t have the information but we weren’t expecting quite those questions.

Most of the European green investors were going into much greater depth. How does the carbon footprint change? What is the exact change in percentage points down to the second decimal? Frankly, we didn’t have the answer to hand. We had it in the files but we didn’t have it with us.

Had we done a proper certification it would have probably taken an additional week to 10 days, but I think we would have got a far better reception. So learning number one: get an independent certification. It’s not a reflection on your individual credibility, but it does make the investor a lot more confident because that investor also needs to be answerable to his own authorities or his own funding principals.

The second is more of a derived learning. When we went in for this issue, we were looking at investor diversification. We achieved that: we did get in a number of investors who do not normally invest in our bonds, and we’re otherwise a pretty regular issuer. This came from both pure green funds and the green arms of not-so-green funds. So we did achieve investor diversification, that was not a problem. Our issue was about 3.2 times oversubscribed and perhaps about 0.8 of that was the green funds.

That was important, but you should not expect to get a significant price advantage. We knew that, but it reinforced our learning. When you talk to a green investor, focus on the investor rather than the green. Yes, he or she is predisposed to look at your green offering, but at the end of the day they’re looking at the return on investment and don’t expect a big change on that.

IFR ASIA: Some very interesting thoughts in there. Ashok, just to take a step back for a second: why should an investor care about environmental considerations? What is the benefit to them of an ESG strategy?

Ashok Emani, IDFC: Thank you Steve. Actually there’s a strong correlation between the ESG factors and the financial performance of a company. It has been proven and there has been a lot of progress over the years. More and more companies are adopting ESG factors and analysing materiality to their business. Good ESG practices improve access to capital from wider investor base.

As David has said, that independent certification is something which incorporates all these softer issues around ESG, and it’s the same for asset managers. Investors are forcing companies to adopt ESG factors in their analysis and come out very clearly on how they are addressing certain issues.

Unless you take care of your ESG factors, you risk spending your resources – your time and money – on E&S issues which may go haywire after the investment happens. You can see in businesses the world over, up-and-coming businesses are integrating ESG – which is paramount. They are asking for ESG issues to be included in their due diligence. Addressing the ESG issues prior to investment has been going on for a long time already.

IFR ASIA: Avinash, you can represent the arranger community here. What sort of outlook have we got for green issuance? What does it bring to a borrower that a regular financing wouldn’t?

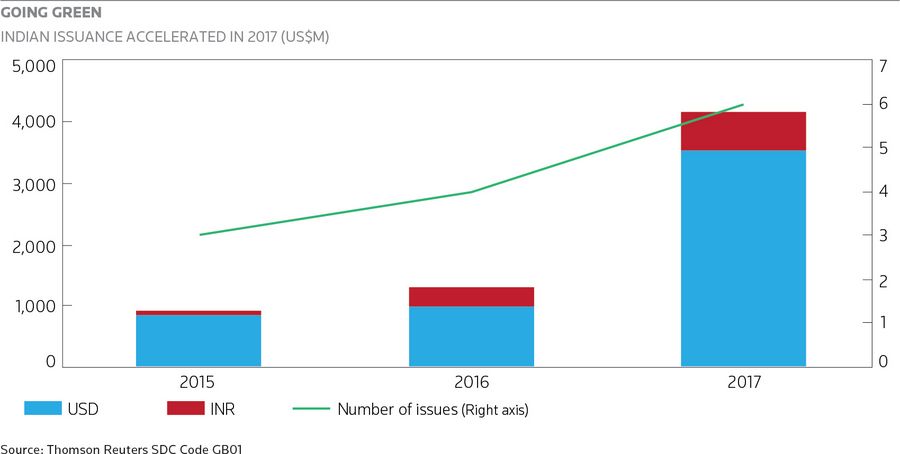

Avinash Thakur, Barclays: I think from an Asian perspective this market is likely to grow. Globally, we’ve seen a huge amount of growth. The green bond market now is in excess of US$250bn and Asia is still a very small part of that.

Now there’s a lot of emphasis from the regulators in the two big markets in Asia – China and India. Regulators have come out with Green bond principles and guidelines, and they are very encouraging of issuers trying to do more green bonds. In fact in China, the regulators have made a lot of concessions for issuers who are looking to do Green bonds.

From our perspective, as David said, it’s not something which has reached a stage where issuers are prioritising this over conventional financing. The reason for that is it does come with some additional work: you need external certification; it does come with end-use restrictions.

The pitch really is that it still has to make economic sense, just as much as it’s a statement that you’re committed to sustainable financing. Unless you see the cost benefit of issuing in the green format, issuers are not going to get attracted in a big way. They will do it for signalling purposes, but that’s once in a while. Once we start seeing the economic benefit, that’s when the market really moves in this direction.

In Asia we’ve not seen that happen so far but globally we’ve seen evidence of that. The total amount of funds looking at these opportunities is now in excess of half a trillion dollars. That liquidity is only available to issuers who follow this format. That liquidity is much more sticky, so in volatile times you will see the green bonds are more stable, because these investors are very committed to this financing. They’re not there to trade the bonds. They’ll hold those bonds for the life of the bond.

There are benefits in terms of where the bonds trade over time, and over time you will see a new issue benefit as well. The amount of investor attention that you can attract if you issue in the green format would be much larger than in the conventional format, which will obviously result in reduced pricing. It’s not happened yet, but I think we’re getting there slowly.

Once we reach that stage I don’t think we’ll have to go and pitch Green bonds. I think every issuer will want to do Green bonds.

IFR ASIA: David, I saw you nodding at the idea that green funds can be more sticky. Have you noticed any difference between the way your deals have performed?

David Rasquinha, India Exim: Yes, Avinash is absolutely right. A typical green investor is not a trader. He’s a buy-and-hold type, which means there’s that much less of your paper actually floating in the market. Bear in mind that even in a green bond, it doesn’t mean that 100% of your investors are green. The dedicated green investors will hold between 15% and 20% of the total issue – it’ll vary from issue to issue. That means that 15%–20% are effectively off the market, because they’re not being actively traded, and your price is looking a lot better. When you go in for your next issue, the secondary market price of that bond will help you because of these technical conditions.

We did see this in fact when the famous taper tantrum happened and during other market movements. The green bonds have been a lot more stable compared to the non-green.

IFR ASIA: Very interesting. Ashok, would an investor ever pay a premium for the green certification? Should that in your view come with a different price?

Ashok Emani, IDFC: Yes, actually there is a premium which comes with the ESG value-add, which accrues to the entire investment. It’s not just the awareness which is being generated around the ESG.

So what we have observed from our portfolio, from day one when we take up the issues on ESG, we identify the potential areas where the ESG in the investment can add value and areas which could go bad. While working with the investment, we get the time to address the issues by allocating sufficient resources to bringing it back to normal operation. That feeds into the expected price at the time of exit.

The awareness is, of course, building up. The UNPRI is one platform, but there are many others bringing more and more investors into their fold. At the moment there is about US$83trn of assets under management across these platforms, like the CDP [Carbon Disclosure Project]. The investor base has also increased over the last two decades. It started off with five investors signing up to UNEP FI in 1991 and now it is over 600. Similarly, UNPRI, which is a commitment to the principles on responsible investing, has moved up from 65 to 1,800-plus investor signatories.

Obviously, there is an awareness which affects their premium at their exits. That’s automatically making investors internalise sustainability in their systems and address the ESG issues. If you are aware and work on these issues upfront, you will obviously get the premium.

IFR ASIA: Sandeep, what kind of incentives do we need to think about to get things moving even faster?

Sandeep Bhattacharya, CBI: Let’s just devote a minute to see what’s the downside if things don’t go well. This all flows from the Paris Agreement and if we don’t follow that, this hotel where we are sitting will surely be under water, and so will the rest of Mumbai.

India will see more extreme temperatures. Northern India will see temperatures above 56, 57 degrees Celsius quite often. That means agriculture will suffer a lot, which in turn means there will be a severe food crisis. The whole of the Gulf Cooperation Council will nearly become unliveable, which means a lot of people – a lot of Indians – who live there will need to relocate and here we have shrinking land, shrinking water, shrinking food supply.

That’s the urgency. That’s the risk. And here I would like to quote Anand Mahindra, chairman of the Mahindra Group who said: “Climate change is therefore the biggest business opportunity.”

Having said that, I’ll try to answer your question about what kind of incentives can help. I know it’s very difficult, but my wish list would be that some of the money in the system is directed to us. This may be by RBI guidelines designating climate investments as priority sectors, which has been a very good way of incentivising the flow of funds. We don’t know when the RBI may change its guidelines – it’s been in the press for around a year that it’s coming, but it’s not yet come. That would be a very welcome moment.

IFR ASIA: So there’s already some discussion about assigning particular lending requirements to green projects?

Sandeep Bhattacharya, CBI: There’s been a lot of press that RBI is coming up with regulations on green finance. We know for sure it coming, is but there is some speculation about what that requirement will be.

There is also some talk about making insurance companies dedicate a certain corpus towards these causes. The issues, I think, are around how you define it. If the definition is not watertight, it can be heavily exploited. This is the first thing on the wish list, to have a certain amount of capital dedicated to green finance.

Having said that, we know that in India these policies don’t move extremely fast. And there are historical reasons for having regulations for insurance companies and provident funds, which possibly should not be moved extremely fast because the sector needs to be trained.

Therefore, we’ve been looking to maybe create a substitute. You might be aware that there is a CSR [corporate social responsibility] fund, where companies beyond a certain level of profitability have to put a certain amount of money into CSR. That fund is about Rs280bn, roughly US$4bn.

About 6% goes into environmental causes. Now if we could somehow pool some of that 6% into a fund which invests in paper from environmental causes, then there will be some incentive to do a green bond in the local Indian market.

So this is a mechanism being worked out by one of the big four consulting firms, and any AMCs here who are interested can obviously take it ahead. It’ll be more about branding initially, but then that’s how the market can possibly take off in the absence of regulatory support.

The other kind of support requires policy changes, which are slowing but are coming in various states for the distributed energy sector, and there’s a lot of other financial innovation necessary from the people in the room to ensure that funds are available for things like rooftop solar. The multinational development banks can also be there to invest in the right structures.

It requires some innovation and maybe some deals will take some gestation. These are some of the things which I think will help.

IFR ASIA: Lots of interesting ideas there. On the idea of pooling money together into a green fund, I think we’ve seen some of this in the global markets, right, Avinash?

Avinash Thakur, Barclays: Absolutely. As I said earlier, over time you will see this become common practice, but to start with, the market will need some infrastructure support.

One important thing is that there’s a big misconception about how can you contribute. Everyone wants to contribute. I don’t think there’s anyone in this room who would dispute that this is the future and this is the way to go. How do you contribute? When I talk to my clients, the issuer community, the question is often: “Can we issue a green bond if we do not have a green business?”

The reality is everyone can contribute. Even companies with exposure to coal have issued green bonds globally. It’s about bringing down the emissions and raising your standards.

Another issue is you may not have a big enough funding requirement to warrant a large bond transaction, and that’s why the pooling becomes very important. If we could have infrastructure debt funds that are dedicated to green financing, that would also make it easier for the smaller players. Sandeep talked about rooftop solar. I don’t think banks or large funds will be interested in financing the small players, but if you can pool assets and create dedicated funds for these smaller players, that’ll help them. Green finance needs to reach where it’s most needed.

Just to give you an international perspective, this market five years back was as small as it is in these developing countries right now. We started the Barclays MSCI Green Bond index in 2013, and that gave the market a big impetus. We also set up a fund which was dedicated just to green investments and we got third-party money into that. That again was a very good way to get things started.

So I think these are some of the factors which are needed while the market is making this transition, until we reach critical mass. As I said, once it makes economic sense then you don’t have to worry about trying to encourage issuers or trying to sell this paper.

IFR ASIA: On the investor side, how much time do you have to spend tracking that investment, making sure that what you’ve bought is actually green? What can you do if it’s not?

Ashok Emani, IDFC: Basically, we follow the standards in terms of social and environmental sustainability. So in the beginning, when we look at a particular investment, we set out our action plan in terms of what needs to be tracked for the entire project, particularly on the environment and social indicators that we have developed, and we track those throughout the investment period.

This level of engagement happens with any investee company from day one. It gives clear signals to the company that they have to really look at the indicators and parameters set out for them, and they are also tuned to deliver on that. It is an integral part of the entire deal.

The emphasis here is on working with the company from day one. That way you are able to review the performance, take corrective measures, and do you value-add and prepare a business case out of that. Every year you have to set goals and objectives for that particular ESG aspect and that’s how we track until we exit.

IFR ASIA: I see. David, based on your experience, how much time and effort does that reporting and ongoing requirement take up?

David Rasquinha, India Exim: Frankly, since we did not go in for the original certification, it doesn’t really take up much time. I essentially get my outside auditors to confirm that the funds have been used for the projects we committed to at the time of the issue.

Had we gone in for the certification, given that we have all the data with us I would not see that as a constraint. For EXIM, we have large projects, so it’s not that I am giving a range of about 20 different projects, it’s probably 4 or 5. So it’s easier for me to demonstrate that.

To my mind, the time to receive the certification or even the cost – Sandeep, you didn’t hear that – is not really too significant in terms of the diversification that we can achieve. The cost/benefit is very clear.

AUDIENCE: I work for Moody’s. My question is around certification. How much importance do investors place on certification for the annual monitoring process, basically the use of proceeds? And does it help to tighten the price of a new issue in the offshore market? Second question: is there any scope for other players to provide Green bond or assessment services?

Ashok Emani, IDFC: When I said we work with the companies, we look at getting the right environmental and social management systems in place. They mirror the certifications given by ISO14000, EMS certification and so on. It may be advisable for the investments to go for certification at a later stage, but we don’t stress that you get certification from day one. We look at the requirements embedded in the ISO and other systems, and on similar lines we help the investee company prepare itself to that stage where it can secure the certification.

David Rasquinha, India Exim: Just to come back to the point on pricing, to give you the actual case study of our bond, as I said, we were 3.2x on book. Now without the green investors we would have been perhaps 2.4x something like that. To that extent our ability to tighten the price would have been less.

Now how do I quantify that in pricing? It’s a hypothetical situation. In theory, yes, given that your universe of investors expands and there’s going to be that much more demand, so logically you should see a benefit in pricing. But if that’s your primary aim in issuing a Green bond, I don’t think you’re going to be very satisfied.

AUDIENCE: I have a question to Avinash. Let’s say, an issuer sells a Green bond and commits to certain efficiency gains over the life of the bond. What happens if the issuer commits to 100 but only reaches 90? What happens to the pricing?

Avinash Thakur, Barclays: Typically, most issuers will not overcommit. So if you think that you’re going to hit 100 you’ll probably set the requirement at much lower than that. That’s still acceptable to investors. You don’t need to go to 100 to sell bonds. It’s not very different from the way we put covenants on a financing. You give them some headroom.

The idea is to encourage this kind of financing. It’s not to make life difficult for the issuer. The investors also want to encourage it, so whether you brought down emissions by 100 or 50, it does not matter so much to them. The fact that you’ve committed to bringing it down is more important for them. Even if a situation arises where you’re not able to deliver on the target, I see the investors still being very supportive, because at least you’ve moved in the right direction. The important thing is that everyone can contribute, and should contribute to addressing this climate challenge.

IFR ASIA: Sandeep, I read recently that you are looking at securitisation in India. What’s the potential there?

Sandeep Bhattacharya, CBI: Yes, and we are soon going to come out with a full version of that report. As Avinash mentioned, for any institutional investor to come in you need scale. You need a pooling mechanism. In that case, securitisation can be very effective. Right now, we are trying to support two such proposed transactions where rooftop solar systems or other small assets are being pooled together for institutional investors or multilateral development banks.

I know that securitisation is not a very stable product in India. It has gone through a lot of regulatory topsy-turvy and there for a while a tax on the SPV that nearly killed the whole market. But it’s seeing a revival, and last year we saw the structuring of India’s first proposed Green securitisation, even if that was possibly a bit too ambitious to get placed immediately.

We talked earlier about how all renewable energy is financed by the banks, and the banks rely on short-term deposits. So inevitably the loans will be for 20 years with a five-year reset, which means borrowers effectively get only five-year money. If we can make securitisation work, a bank can actually provide part of the financing with a 20-year or 25-year fixed rate and then sell it down to a provident fund. That would then create a market for long-dated loans, which would then pump in a lot more money into anything with a long-term concession. It could be a water concession, waste management concession, or a pool of assets.

Securitisation can work as an instrument both to bring long-term money into long-term assets and to help small developers to refinance even if they don’t have a treasury. They can concentrate more on how to be more efficient in generation. We are doing whatever we can to promote that idea.

IFR ASIA: Ladies and gentlemen, thank you for your time.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@tr.com