IFR ASIA: The ADB has been very keen on local currencies within ASEAN, am I correct?

NORITAKA AKAMATSU, ADB: We are very supportive of this integration. The Asian bond market has basically two pillars: one is integration, the other is market development. But market development very much focuses on the frontier markets. Something cannot be integrated until it exists, so the focus there is on middle-income countries where there is a functioning market.

The case of Laos and Thailand is a very special one because Laos is a frontier market. It’s a strange relationship, particularly in terms of electricity: Laos sells electricity to Thailand and the Electricity Generating Authority of Thailand (EGAT) actually buys it and sells it back to the Lao government.

Before the Lao government issued straight, baht-denominated sovereign bonds in Thailand, the ADB was in discussions with Laos about the possibility of securitising the royalty revenues it received from EGAT – or the de facto Thai government, the sovereign. It could establish a special purpose vehicle in Thailand and then issue securitised debt.

In the end the Lao government chose to issue more plain vanilla sovereign bonds, but it was a possibility. You could say a significant part of the revenues of the Lao government is backed by, or coming from, the royalty revenues from EGAT. It’s almost like a Thai sovereign, so if you securitise it in Thailand, people will buy it comfortably. So it’s a very special case.

But the other integration we are supporting is much more complicated.

FAISAL AHMED, BANGLADESH BANK: It has to be backed by trade relations. Intra-ASEAN trade is not that high, so you are right, its potential is limited. In the case of large frontier countries like Bangladesh, we don’t have sufficient two-way trade at this point, so it’s not going to work as a general strategy. Instead, the strategy for frontier countries like Bangladesh remains a plain vanilla approach: external market in either in dollars or local currency, which we haven’t done yet, or developing the domestic market.

ADISORN SINGHSACHA, TWIN PINE: Sometimes you have to try to keep it simple, while not falling into the trap of the Mongolian delegate from earlier, who thought the main thing for his country was selling horses. You have to bridge the language. Trying to securitise debt increases the level of complexity and for me it becomes very one-dimensional, focusing on the source of income or which country is the trading partner.

My approach is different. The way I see it, there is the concessional and the commercial. Eventually, countries aspire to move up the income scale, and therefore they need more financing to be commercial. Either they do it now or they do it later. Myanmar and Cambodia told me they think they will be ready by 2018. If I can expedite it and do it earlier, great.

The Japanese government offers Myanmar almost limitless funding at 0.1%. If you suggest a commercial deal in Thailand at, say, 5%, or in other markets at 7% or 8%, it is hard for the government to see why it should borrow at such an expensive level. You need to be able to explain the pros and cons, and the best way to get that experience is by issuing a simple plain vanilla bond.

But Laos and Thailand isn’t the only example. ADB brought us to a South Asian country wanting to find out how to go about issuing. The first step is the simple vanilla bond but after we had spoken to its representatives two or three times they wanted to look at issuing in Thailand, and use that as an experience they could learn from.

Cambodia is thinking about issuing in 2018 but is also thinking about whether it could do a trial issue before that, for around US$100m, to familiarise people with the process. It’s about holding its hand through the process and completing it. That means completing the prospectus, the roadshow and all the necessary PR.

Having gone through that, Laos understands a bit more. First its representatives were talking about what happens if the gold price comes down, but later they were talking about its diversified sources of income, and how it will be earning more and more from hydro and exporting power. Learning about that is the first step – getting the government out, doing the commercial deals and understanding how capital markets function. Then they can go back to their country and ensure everything is in place, that there are custodians, that they are ready to pay interest rates and the rest of it.

You also have to talk about liquidity, but that is very low on the list of priorities because liquidity will not be there in the early days. So you focus on a short-term bond, maybe three or five years, and that’s it. Then they know the risk for that duration.

FLORIAN SCHMIDT, SC LOWY: Laos is in an enviable position because it has this big market in Thailand, and in some ways Laos is almost an extension of Thailand: they speak the same language and have similarities in their cultures, for example. So selling a Laos bond into Thailand is almost like selling to a domestic investor base, and we know that domestic investors sometimes price risk differently than how offshore investors would price it.

So the question is how big is the domestic market you can sell into? Laos has a US$182m US dollar deal maturing in 2025 outstanding which yields 4.6%. That clearly reflects the name recognition from the Thai financial institutions who bought it. It’s a Libor-based instrument, so I assume it went to Thai banks. That also answers the question about the liquidity of such instruments.

But not all countries have the luxury of a domestic market they can sell to, and those countries have to consider securitisation instruments. There have been examples in Latin America when those countries were considered frontier. Pemex, PDVSA and Petrobras did offshore receivables securitisations at times when their sovereigns could not come to the market because investors simply did not trust Venezuelan, Brazilian or Mexican sovereign debt risk at that time. Venezuela may unfortunately find itself back in this scenario in the not too distant future. But those companies wouldn’t have a domestic market – although the one in Brazil is very large – where they can necessarily raise funds, so they have no other choice.

This may be something Mongolia, for example, should be looking at, if there is mistrust among investors because of the political situation in the country. The off-takers of Mongolian commodities are, in some instances, very highly regarded companies in places like China, Australia or Japan. If you securitised such payment streams, that could enable the country to raise funds. So there are options, but you have to look at the context, in terms of volume or in terms of the target investors.

ANDREW COLQUHOUN, FITCH: Is there a minimum level, particularly for a new sovereign frontier issuer? I have heard it said by people active in DCM that it would be very difficult for a sovereign to come to market for much less than US$500m – or even US$1bn. That’s an issue for countries that have quite low GDP. If a country with a GDP of US$10bn does a US$1bn bond, the ratios explode.

If we’re looking at a credit for the first time then it can almost be a binary proposition: the debt ratio is 20, but if they do the bond, which after all is the whole reason that they want the rating, then it goes to 30.

ARTHUR LAU, PINEBRIDGE: There are emerging market corporate and emerging market sovereign bonds indexes – in Asia we don’t have separate corporate and sovereign indices because the sovereign universe is very small. I think part of the reason some issuing countries prefer local currency sovereign issuance rather than the dollar is because the government may be unable to meet the international expectations around effective communications and transparency. For corporate debt, the issuance size is simply too small for an index.

There’s a fine balance between the size of issuance and the rating it can achieve. If an issuer comes out with a very small deal – around US$20m or US$50m – it may not be feasible for us. But in the high yield corporate market you can get issues of around US$100m-$150m equivalent that are viable, especially if the investor knows there will be a continuation of the programme.

IFR ASIA: Does that not apply to sovereign debt as well?

ARTHUR LAU, PINEBRIDGE: I think it does. We look at the motivation behind this issuance. Say a country has a Medium Term Note programme and a US$2bn or US$5bn deal is coming. It may not issue that in one big chunk. It may issue in different series and at different tenors and the investor may like to have the choice. We like sovereigns to build out their curve over time. Not everyone wants to invest in the five-year paper, for example, some may want a longer or shorter duration profile to balance their exposure.

There are a host of different dynamics we can play, but, in a nutshell, if investors think an issuer will come to market frequently it’s a more welcome proposition. On the other hand, if people know countries will be issuing non-stop after having done a US$1bn deal, that could be a problem. So there’s a fine balance.

IFR ASIA: Bankers work on commission, so deals will tend to be bigger.

FAISAL AHMED, BANGLADESH BANK: But issuing billions after billions could make investors nervous too!

ANDREW COLQUHOUN, FITCH: I’ve certainly noticed these programmes usually come with a glossy presentation booklet and a sexy title like Project Phoenix, presumably that makes a difference!

ARTHUR LAU, PINEBRIDGE: Yes, the name can be another gimmick. It’s the communication. Sometimes I can appreciate why a sovereign has come to market. Sometimes there are commercial reasons. It can look like an international deal makes no sense they have to invest in roadshows and educating investors and offering all this transparency. But then I think, actually, they need to do all this to build a longer term relationship with international investors, even if it doesn’t make sense in the short term.

From the investor perspective, sometimes we need to have our hands held and be walked through what the sovereign is thinking. Then we can find common ground which will give us more confidence to invest.

FAISAL AHMED, BANGLADESH BANK: When it comes to PR, how much of this is your way of getting a proxy for the overall economic management, rather than the communication itself?

ARTHUR LAU, PINEBRIDGE: It is partly about the ongoing monitoring. For example, we invest in a frontier agency, in its dollar debt. And in the last crisis, when there was a situation in the local currencies, we wanted to assess its ability to make payments, and whether it had sufficient foreign reserves to repay the foreign debt. So we were trying to get in contact with its communications, marketing or investor relations people, but we got no reply. We found out one of its delegates was in Hong Kong attending a conference, so we tried to arrange a private meeting but the person didn’t show up. If you don’t get that information you can’t assess the risk and the best option is probably to get out, because you don’t know what you’re facing.

ANDREW COLQUHOUN, FITCH: I think there’s a question about the quality of advice that sovereigns receive. Many of them work with banks that provide advisory services, I think it’s generally for free, upfront, and obviously the banks hope to benefit in terms of building a relationship further down the line. I’m routinely surprised at what sometimes seems to be the quite low quality advice sovereigns are getting in that process.

Perhaps it’s because the sovereign market is very small. I think the banks often lack dedicated services in this area – people with an economics or macro sovereign credit background. So instead they deploy people with a corporates or financial institutions background, who may not grasp the kind of questions that macro-focused investors would tend to ask.

FLORIAN SCHMIDT, SC LOWY: It makes sense for every emerging market or frontier country to aspire to access commercial funding. No country should live on 0.1% grants from Japan for eternity. At some point these countries have to learn to stand on their own feet and broaden their investor bases. That means bank borrowing and capital market funding and, for emergencies, concessional funding. That is something to fall back on if things go wrong, if commodity prices collapse by 90%, which is typically not the fault of these countries.

It is important to engineer a path for these countries to access international, commercial funding, and from a bond market perspective, to build and cultivate a solid investor base with 500 or 600 investors regularly participating in their transactions. That is a great achievement.

Consider where the Philippines was in the late 1990s. It was a credit that had just come out of the doldrums, it had a very small investor base, it had to pay double digit coupons to fund itself. In its most recent transaction it achieved coupon levels at which very solid investment grade countries have been funding themselves – very low single digit levels. That is a massive achievement. That’s the path emerging markets countries and frontier countries should take.

IFR ASIA: Let’s talk about the taka programme that Bangladesh is working on with IFC, which is a precursor to achieving the international access we are talking about. How do you see that developing, and what’s the real rationale?

FAISAL AHMED, BANGLADESH BANK: A lot of this discussion has implicitly centred around the issue of sovereign access. The way we’re looking at the taka bond issued by IFC is it will give us a currency risk benchmark. We hope and expect that currency benchmark will then be used by domestic corporates who want to issue abroad. That’s the first rationale.

The second is that our government securities market right now is fairly modest in size. In dollar terms it’s not that small, it’s around US$35bn or US$40bn. But with that currency benchmark, that risk benchmark from the taka bond, it will be easier for foreign investors to price domestic government securities in Bangladesh. It could also allow domestic corporates to issue taka bonds, either in the domestic market or offshore.

So it’s basically getting a benchmark. We hope it will be a catalyst that will allow us to do other things. Foreign investors currently look at the currency risk in Bangladesh and they see US$27bn of reserves, a manufacturing economy without commodity risks – all those macro fundamentals are there. But when you’re looking for a price you need a sense of the currency risk. The taka bond will help, giving a benchmark for that currency risk.

IFR ASIA: Have you considered jumping that hurdle yourself? Would Bangladesh or Bangladesh Bank be a viable issuer overseas in the taka currency?

FAISAL AHMED, BANGLADESH BANK: We have thought about it but you have to look at the external liquidity we have. It’s a lot of external liquidity. The domestic market is currently also flush with a lot of liquidity.

It’s not so much about jumping as about jumping properly, and building a track record. We look at it in a holistic way, because the Bangladesh story is not an SOS story. We want to set a track record both for the public sector and subsequently for the private sector, because it will be a private sector-led growth story. So it’s about setting that benchmark, and we want to do the due diligence properly. That’s why we are taking this methodical approach, rather than issuing it and then using the proceeds for general government purposes. We want to avoid that, the focus will be on specific projects looking at relative issuances.

IFR ASIA: How closely have you been watching the experience in India and the Indian rupee? This seems to follow on very much from what IFC and ADB did in that currency?

FAISAL AHMED, BANGLADESH BANK: The Indian model is a very good, relevant story for Bangladesh. One difference is the economic structure of Bangladesh compared to India: India is more of a service-led, take-off story, whereas Bangladesh is a manufacturing-led, take-off story. But both are private sector led.

The Indian issuance that initially set up the rupee benchmark was subsequently taken up by corporates. Our hope is that a very similar evolution will take place for us, with corporates using the taka bond both in the domestic market and also in the offshore market.

IFR ASIA: Is this something on your radar Arthur? Have you looked at these issues, like the offshore rupee deal from the IFC?

ARTHUR LAU, PINEBRIDGE: We do, and not just in India, there have been some local corporate issuers in Asia that have offered Dim Sum-like versions of their own bonds. I think usually the first batch of issuance will come from the supranational agencies, which offer more credibility in terms of lower credit risk but are still a direct play on the FX and the local market. These instruments have the advantage of overcoming some of the infrastructure issues that I mentioned, like the settlement issues, because they’re more internationally focused, in terms of the way the securities are structured.

But one problem we have had is the lack of follow through with these kinds of instruments. For example, we were talking about the replication of Dim Sum bonds in the Indian offshore market, for local currency bonds. You get an issue, and maybe a second, but it is hard to know whether the programme will be continued or if there will be a meaningful size in the market.

Dim Sum is of course a successful story, but in recent months it has had some problems and the market seems to be shrinking. So there is a question as to whether this is a viable alternative to the dollar market for these frontier issuers. We have every incentive to look at the market, but whether it is likely to be a one-off, or whether there will be a steady supply, is another question.

NORITAKA AKAMATSU, ADB: I actually question this notion of multinationals and supranationals coming to issue in the local currency market and being the benchmark. As you rightly said the issue is whether there will be a follow-up, which seems unlikely. If these instruments are going to be a true benchmark there needs to be regular issuance, and the only party that can do that is the government.

Another issue is that supranationals can never beat the host country government when it comes to looking at local currency funding. The price is always going to be the host country government plus a spread. Our reputation and credit rating doesn’t matter. When it comes to the local currency market, only a government can print money, we can never do that. I am not sure this notion is well understood. If the World Bank or ADB issued in the yen market, we’d still get priced Japanese government plus spread. The Bank of Japan can keep printing money for the government, we can’t.

ANDREW COLQUHOUN, FITCH: We’ve come across this question quite a lot: why isn’t every sovereign Triple A in its own currency? But we have seen countries choose to default on local currency debt, rather than take the inflationary consequences of the money printing route. Russia did it in 1998, when it defaulted on its rouble debt whilst maintaining payments on its dollar debt. Jamaica did it more recently, in 2010 and again in 2013. And Argentina did it in 2002. So we do have experience of local currency default and countries preferring to service foreign currency debt, although we do often have sovereigns rated around a notch higher for local currency debt.

And it’s not just about money creation, given that advanced countries have been doing that more than emerging markets, recently. There are other factors that lead to a strong demand for government debt among local financial institutions: banks need a certain amount of government debt to meet a statutory liquidity requirement, or to match against a local currency liability.

ARTHUR LAU, PINEBRIDGE: I agree the only viable frequent issuers will be governments, but unfortunately some just don’t have offshore local currency government bonds. Even China has offshore government bonds (CGB) but they’re hard to buy. We’d love to have more sovereign liquidity but the fact is some governments prefer not to issue it.

So the next proxy is the supranational. And I think investors feel some supranational organisations issuing local currency bonds in the international markets offer slightly better credit-worthiness than some governments issuing in local currency in the offshore market. It’s because of the trust, as we have discussed – because of the superior communication.

So the risk perception is lower but you get paid more – so why not invest in supranational, local currency paper? These supranational or international agencies like the World Bank or IFC or ADB seem to be more willing to be the pioneers, helping local governments issue local currency debt in the international market. As an investor we will usually be more than happy to support it because it provides a higher degree of credit-worthiness.

FAISAL AHMED, BANGLADESH BANK: But when foreign investors look at the yield on local currency offshore debt, how can they judge how much of this is coming from currency risk and how much is from the sovereign risk? For a supranational it’s very easy to work out.

But ultimately as has been said it’s a good start, it is all about the evolution of the market. There is no shortcut.

ANDREW COLQUHOUN, FITCH: One of the characteristics of the most successful countries, with the biggest, deepest bond markets in the region, is the low and stable inflation, and a rate structure that reflects that. And you need the right domestic macroeconomic structural characteristics, like a good savings base in the country. That allows the Thai sovereign to issue at 50 years in the baht market.

ADISORN SINGHSACHA, TWIN PINE: The key for sovereign issuers is they have to start some place where investors are familiar with their credits. So for Myanmar, Cambodia or Laos, maybe they should be looking at Thailand, Malaysia or even Singapore. Look at that small group first, rather than going straight to the international market. Start somewhere familiar.

And they need to get good advice from somebody dedicated and committed to helping them. The IMF is already helping Myanmar to start its Treasuries programme, to familiarise them with the process, like making regular interest payments. They need to find people that are willing to spend time, not come in, do it quickly and then leave and then five months later send another team. That commitment and dedication means working with the issuer at all levels, understanding the government, meeting the ministers and the director generals and the people working on the ground. If it’s something imposed from above, it won’t get done. It means spending time educating, on the policy level and on the execution level.

And finally it’s about the evolution of the bond market experience. So start with the government bonds, maybe in the international market, and then move on to the state enterprise or the leading local corporates issuing bonds once the benchmark has been established. And only then, if the local market is not developed, do you go back and do the local currency market. After that you can do project bonds, securitised bonds, perhaps guaranteed by something like the Credit Guarantee and Investment Facility (CGIF).

FLORIAN SCHMIDT, SC LOWY: It depends on the country’s specific circumstances, which route will be best. Clearly, a commodity exporting country may prefer to do a securitisation transaction, in the absence of a domestic market.

Or take Mongolia. It didn’t have a domestic tugrik market, it’s now building one. The sovereign didn’t even understand how the bond market worked, but back in 2006 a commercial bank, the Trade and Development Bank (TDB) – which sounds state-owned but it’s not, it’s a private bank – decided to do a small, US$50m bond transaction. It had a fantastic management and understood what it means to come to the bond market.

Many, including in the financial media, thought it couldn’t be done. But sometimes you just have to jump into the pool and see how cold or warm the water is, and in this instance the water was very pleasant! The deal was completed in January 2007 and it had an order book of about US$700m, it was supposed to be a US$50m deal, so we upsized it to US$75m*. It was still a small start, but there were about 100 investors in it with a mandate to buy Mongolian risk, something that had never been done before.

When the same bank came back three years later, having repaid the US$75m, it did a US$150m deal. The bank had grown quite dramatically, in line with Mongolia which at that time was one of the strongest growing economies in the world. During those three years, more and more investors were applying for country limits for Mongolia, because a lot of investors wanted the paper but couldn’t buy it because they didn’t have the country limits.

TDB came to market a few more times, it did a renminbi issue as well, and then in 2012 the Mongolian sovereign finally made up its mind. It sent its development bank first, which got a US$580m deal done with a US$6bn order book and 300 investors. And then the sovereign came with a very similar dynamic.

So for some countries it will not be the sovereign that goes first. Some countries use a commercial bank to test the water and if that does well then the sovereign may go second.

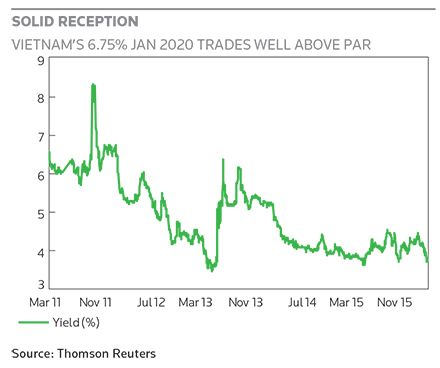

There is a Bangladeshi issuer out there, Banglalink, which is a mobile phone company. They did a deal in 2014 which was an absolutely spectacular success, pricing at a 8.875% coupon, and trading today above par at an 8% yield. Considering all the concerns about emerging markets and frontier debt at the moment, that is an absolutely fine performance for the bond.

So there is no template. Some countries will lead with the ministry of finance, some with the central bank. Some go domestic, others go international. Sometimes a bank goes first, other times it’s a corporate. There is no template, but there have been a couple of very, very decent success stories here in Asia.

FAISAL AHMED, BANGLADESH BANK: The important thing is to create the success stories.

IFR ASIA: Would a credit wrap or a partial guarantee help some of the lower-rated, lower-income countries access markets? Last year in Africa, Ghana did a US$1bn 2030 bond which was 40% credit wrapped by the IBRD, the World Bank. It paid a coupon of 10.75% so it wasn’t cheap, but it got Ghana into the market when otherwise it would have been closed. Is that a route Asian frontier nations could look at?

ADISORN SINGHSACHA, TWIN PINE: I think they could look at that, and it would actually take them more international. A credit wrap allows investors to look at much lower credit names. For the issuer it reduces the interest rate gap. So yes, it’s a good idea. CGIF is active on this and we are already talking to a few organisations about it. In one instance we are talking to a commercial bank that might not wait for the government and might come out first. If this happens and is a success it can encourage others to follow.

And I agree with the point about success stories. My example is Laos, which was unrated when it issued US$50m and US$100m. Then EDL-Gen got rated because it wanted to issue and the law said it had to be rated. It got rated and came out with a US$200m deal that was around two times oversubscribed. So then the Lao government decides to get a rating after three years because it wants to do a bigger deal. So ratings, like credit guarantees, play an important part.

NORITAKA AKAMATSU, ADB: ADB was very happy about the CGIF supporting the issuance of a Vietnamese company, Masan Corporation. CGIF for a while did guarantee, which made issuance possible.

The CGIF does two things: it enables strong companies that are constrained by their sovereign to issue in the international market; and it supports marginal companies, which are otherwise not able to issue, enabling them to issue bonds. Masan’s case is an example of the latter.

We strongly believe CGIF should not only support the local market development, it should also support integration.

FLORIAN SCHMIDT, SC LOWY: When it comes to third party credit enhancement there are three aspects here to consider. The first is the ability to access the market – can a frontier market company or sovereign access the market, or would it be a step too far for investors?

We did the first high-yield international bond from Vietnam back in late 2013 for Vingroup, a leading property and retail company in Vietnam, a big deal. After that we scaled down, looked at other companies to see if they might also have access. We did look at Masan Group as well, but we felt it was probably too early for a standalone issue.

The second issue is cost, and for some issuers cost is the overriding objective. And the third thing – and this one may be related to the poor quality advice some receive that was touched on earlier – is the development of a credit culture. Frontier issuers should aspire to produce a yield curve, whether in the domestic or the international market, because it is the only appropriate reflection of credit risk available.

The 0.1% concessional funding they might get doesn’t tell anybody a thing about the credit quality of Myanmar, or how much progress it has made. Frontier markets need to embrace the risk culture and the price discovery process. The bond market has traditionally been better than the loan market in Asia, there is too much relationship lending in this part of the world.

FAISAL AHMED, BANGLADESH BANK: Issuers need to keep in mind that the Philippines’ success is based on its economic performance in the last decade, the lessons it learned from the mistakes made in the 1980s.

IFR ASIA: Does a partial wrap of 40% or 50% for a credit like Ghana introduce any kind of credit risk? Do investors look at that as sovereign risk?

ARTHUR LAU, PINEBRIDGE: Any kind of credit enhancement is an improvement, it brings in another layer of due diligence to the credit issuer. It means, at least, that there is someone who understands credit who has provided that guarantee. But there is also the question of price. If the wrap is for 40% or 50%, rather than for 100%, you have to consider potential credit situations and what the recovery process will be.

So you have to look at the credit enhancement itself. If it covers 100% of the issue the risk will be very close to the guarantor. The further away you get from that the more you have to look at the underlying credit story.

IFR ASIA: The multilaterals have different approaches, don’t they? IFC is keen on partial guarantees because it wants to develop the credit curve and the credit culture. Others offer 100% guarantees.

FAISAL AHMED, BANGLADESH BANK: Either way it’s a bridge. It’s not a loan.

NORITAKA AKAMATSU, ADB: At the ADB and the World Bank the guarantee is always partial because of the moral hazard risk.

ANDREW COLQUHOUN, FITCH: Speaking theoretically, for a credit enhancement or a credit wrap to be useful, presumably the multilateral has to identify some kind of market failure or deficiency. If there’s a corporate which as a standalone credit is stronger than the sovereign in which it is domiciled, maybe it makes sense for the multilaterals to eliminate the country risk. That allows the corporate to issue purely on the basis of its own credit profile.

But from a credit standpoint my first question would be what are the terms of the guarantee? You need transparency. The second question would be what is the market failure that this credit wrap is addressing?

The other question is whether this guarantee is explicit or implicit. How much weight do you put on an implicit guarantee? You can make assumptions but if push comes to shove it can turn out to be less clear cut.

IFR ASIA: That is probably a good point at which to round up. Thank you all very much for taking the time to talk today.

To view all special report articles please click here and to see the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

*This article has been updated since publication to correct the size of the order book for Mongolia’s TDB.

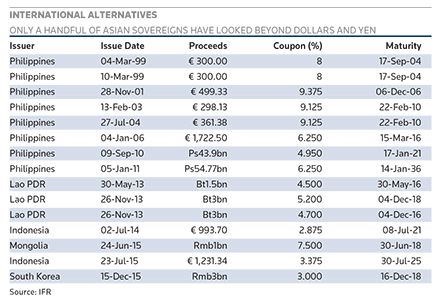

| International alternatives | ||||

|---|---|---|---|---|

| Only a handful of Asian sovereigns have looked beyond dollars and yen | ||||

| Issuer | Issue Date | Proceeds | Coupon (%) | Maturity |

| Philippines | 04-Mar-99 | € 300.00 | 8 | 17-Sep-04 |

| Philippines | 10-Mar-99 | € 300.00 | 8 | 17-Sep-04 |

| Philippines | 28-Nov-01 | € 499.33 | 9.375 | 06-Dec-06 |

| Philippines | 13-Feb-03 | € 298.13 | 9.125 | 22-Feb-10 |

| Philippines | 27-Jul-04 | € 361.38 | 9.125 | 22-Feb-10 |

| Philippines | 04-Jan-06 | € 1,722.50 | 6.25 | 15-Mar-16 |

| Philippines | 09-Sep-10 | Ps43.9bn | 4.95 | 17-Jan-21 |

| Philippines | 05-Jan-11 | Ps54.77bn | 6.25 | 14-Jan-36 |

| Lao PDR | 30-May-13 | Bt1.5bn | 4.5 | 30-May-16 |

| Lao PDR | 26-Nov-13 | Bt3bn | 5.2 | 04-Dec-18 |

| Lao PDR | 26-Nov-13 | Bt3bn | 4.7 | 04-Dec-16 |

| Indonesia | 02-Jul-14 | € 993.70 | 2.875 | 08-Jul-21 |

| Mongolia | 24-Jun-15 | Rmb1bn | 7.5 | 30-Jun-18 |

| Indonesia | 23-Jul-15 | € 1,231.34 | 3.375 | 30-Jul-25 |

| South Korea | 15-Dec-15 | Rmb3bn | 3 | 16-Dec-18 |

| Source: IFR | ||||