IFR ASIA: Let’s start with a view from the macro level. How do you see the need for international issuance out of Asia? Is there still a drive for countries to come into the global markets?

NORITAKA AKAMATSU, ADB: There are some differences between the countries we are discussing today, like Bangladesh, Cambodia, Laos, Mongolia, Myanmar, Pakistan, Sri Lanka and Vietnam. Some of them are simply not ready, and even have a policy not to issue bonds, while others do issue. All of them are of course sub-investment grade, but some don’t even have a rating.

From the perspective of ADB or any multilateral development bank, we support them with so-called “concessionary resources”. At ADB this is managed via the Asian Development Fund, while the World Bank has the International Development Association (IDA) resources.

Lower-income countries have access to those resources, which are a very important source of financing, particularly in the public sector, and they tend to rely on them. If they go to the market they have to pay the market rate of interest, which is much more expensive.

Other countries are what we call “blend” countries: they have some access to those concessionary sources, but they also have to borrow from more market-based facilities. At the World Bank it’s called International Bank for Reconstruction and Development (IBRD), at ADB we call it Ordinary Capital Resources (OCR). These countries have an incentive to diversity their funding sources and hasten the development of their domestic market.

Of the eight countries, Mongolia, Pakistan, Sri Lanka and Vietnam are the blend countries. The others – Bangladesh, Cambodia, Laos and Myanmar – are still ADF or IDA countries, meaning they have full access to those concessionary sources. So they have different levels of motivation to tap international markets.

FLORIAN SCHMIDT, SC LOWY: I think when to go from concessional to commercial funding is the single most important decision a country has to make. Quite a few countries in the region have done this very successfully in the past, establishing a yield curve and a track record. They also create and cultivate an investor base, comprising pretty much all types of institutional and retail investors.

Through the maintenance of this investor base, they have managed to raise funds at very competitive levels. If you look at the 10-year part of the curve, in Vietnam we are down at 5%, in Pakistan it’s just below 8.5% and in Sri Lanka it’s just above 8.5%. These are all levels you would consider reasonable.

IFR ASIA: That might be a nice segue into why a country like Laos would want to issue in the international markets. How do they overcome the hurdles of interest payments?

ADISORN SINGHSACHA, TWIN PINE: When I go into these countries they’re talking about the IDAs, the grants and the concessions they get. There are advantages and disadvantages. Flexibility is one thing: if they want a greater degree of flexibility they should start looking to raise funds on their own, because without conditions they get a lot of flexibility.

However, we’re also careful about governance, because when you give flexibility but procedures are not clearly defined that can create governance concerns. We have to help them with that, so they understand paying interest on time until redemption is how credit worthiness is established, which leads to a lower price being offered.

Before I went to Laos there were times when they paid the interest rates just on time. That can result in a day’s delay, despite them thinking they had paid on time. We explained they had to pay a bit earlier to make sure it went through on time, and the next time they paid two weeks in advance via TMB Bank.

But that flexibility meant they could use those funds for anything – schools, water or anything else in the government budget – which they like.

Countries aspire to move up through the stages of their development, from being low-income countries to lower-middle-income countries and then to middle-income countries. We have to help them realise that means sourcing more of their funding from the market, not just from ODAs, because that’s the natural path. Laos understood this. It got funds at a reasonable rate from cross-border issuance, so it made this one of its sources of funding. Now it depends less on official development assistance.

I think Laos was encouraged by agencies such as ADB praising its efforts, and from the market’s acceptance. But the key was it acted when it wanted to, rather than waiting until it needed to. It fuels the progression of the country through those stages of its development and, by doing a cross-border deal, it avoided crowding out its local market. I think the IDA countries have similar motivations but they’re not sure where to start.

IFR ASIA: How likely are we to see Bangladesh looking at international issuance?

FAISAL AHMED, BANGLADESH BANK: Bangladesh became a lower-middle-income country last year. It has a US$200bn GDP, with per capita income of US$1,300. There have been thoughts about issuing an external bond, but the emphasis is on building the initial track record and the governance due diligence. Any external issuance has to be linked to specific projects that not only generate economic returns but also a cash return.

I cannot give a specific deadline for the timing of a Bangladesh sovereign issuance, but we are working with International Finance Corporation (IFC) to issue a taka bond of roughly US$1bn. IFC will issue it in the local currency abroad and invest the proceeds in the Bangladeshi private sector.

On the loans side, the private sector has been allowed to borrow from abroad in the last three or four years. That borrowing is around US$7bn-$8bn. That is currently export-led and they’re borrowing in foreign currencies, but as they mature they will think about issuing other types of instruments.

IFR ASIA: What are the prospects in the rest of the region? There has been some less than positive news around Mongolia recently. What’s going on there? Has it learned anything from its experience in the international markets?

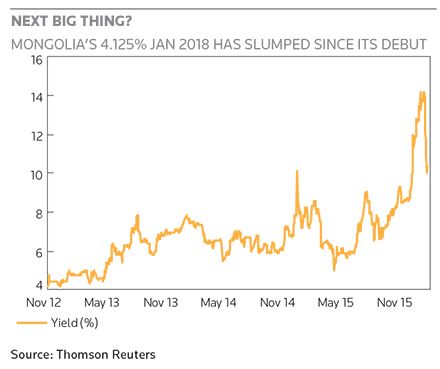

FLORIAN SCHMIDT, SC LOWY: Mongolia issued in late 2012, five- and 10-year bonds with coupons of 4.125% and 5.125% – a lower headline coupon than the yield on Italian 10-year bonds at that time, when it seemed to be exiting the euro crisis. Mongolia was certainly on the right track to cultivate its investor base and I was involved in some of these transactions. What went wrong for Mongolia was its association with commodities, and all emerging markets in that position have been penalised very, very harshly.

If you look back at the performance of dollar bonds in 2015, the worst performers were names that are related to commodities. In Africa, Zambia lost about 20% of its value, while Brazil, which is also viewed as a commodity country, lost 13.7%. The worst performer in the Asian sovereign universe was Mongolia where the bonds I just mentioned, the 4.125% and 5.125%, are currently yielding 13.8% on the five-year and 12% on the 10-year.

If you see a yield curve being inverted like that it tells you that investors perceive a looming payment risk. It will be interesting to see how the Mongolian government deals with these perceptions because, at the moment, the response from investors is not positive. As we all know the Mongolian government did try to raise funds recently and that roadshow failed.

Part of the problem is political: the speaker of the house tried to impeach his own Prime Minister while the country was on the roadshow, which is certainly not helpful. So it’s largely about commodities, but there are also political factors in play.

IFR ASIA: How does the buyside account for all of those risks? How do you pick an emerging sovereign to invest in when there are commodity prices falling, there are currency issues and all sorts of political things that can go wrong?

ARTHUR LAU, PINEBRIDGE: For investors everything comes with a price. If the compensation is there for the risk being taken, there will be a buyer. Buyers must be aware, not only of the risk but of the structure of the bonds and the purpose of the funding. In the countries we are talking about, issuers need to have a very consistent and credible story.

Exposure to commodities is of course one risk factor, but I think the communication and transparency investors get from the government delegate is even more important. In some frontier countries, my experience has not been entirely satisfactory, and it’s not just about commodities but also policy consistency. I have seen situations where governments tell us they are opening up the commodity sector to neighbouring countries and, all of a sudden, policies shift and they shut everything down, break contracts and try to rewrite them. That is something international investors do not want to see.

It comes back to political stability. A few years back, we had the privilege of having a private discussion with an ex-Prime Minister of a frontier country that drives most of its GDP growth through commodity exports. But shortly after he had made certain commitments, the government changed and we were back to square one. That is a problem in frontier markets: the instability means it is difficult to have much confidence that a country’s policy, development plan or even funding plan will survive changes of government. That’s a characteristic of emerging markets generally, actually, not just frontier markets: political elements always come into play, as well as fundamentals.

Some frontier markets are infrequent issuers but, because they are part of an index, investors need to buy paper to benchmark with the bond index. Having a more internationally savvy investor relations or communications person may help, because when we do due diligence meetings with various frontier market delegates, we find that sometimes the levels of communication and the understanding of international language is lacking.

I remember a conference organised by an investment bank two years ago. There were a number of frontier markets delegates on the panel, including representatives from Bangladesh, Vietnam and Mongolia. They’re supposed to be selling their country. An investor asked the delegates to highlight one key feature about their country that investors should look at, and one delegate cited the country’s horses. This makes me wonder why should we, as investors, participate in a country when its cites horses as the most salient investment feature? More useful information is needed and more professional communications could help with that.

FLORIAN SCHMIDT, SC LOWY: When a frontier country comes to market, the first thing that the issuer looks at is cost. It wants to know what it gets if it borrows concessionally, how much it can get, what the cashflow stream is and how constrained it will be in terms of how those funds are allocated to specific projects – which is often dictated by the lending institution.

The alternative is to go commercial, which means it can do practically anything with the money. Of course, it still has to deliver a good story to investors, but it has more freedom – if it is willing to pay up, because the rate is commercial.

This is where the commodities issue kicks in, because countries that are commodity-driven have been penalised. A Single B rated country like Zambia, with no real history of defaulting, is yielding 14% at the moment, while Triple C rated Belarus is yielding 7%. It’s pretty clear that commodity-driven places have been severely penalised.

IFR ASIA: How does the rating take into account things like commodity factors and political risks?

ANDREW COLQUHOUN, FITCH: All ratings balance a wide range of factors. We routinely track over 100 indicators. There are about 18 that feed more formally into the sovereign rating model that we use, but of course analyst judgement applies on top of that.

I have been looking across the spectrum of frontier credits to try to identify some common themes and it’s actually surprisingly difficult. There are some low-income countries but some, like Mongolia and Sri Lanka, are higher income than investment grade credits like India or Indonesia. Some have low government debt while others have high government debt. Some have weak external liquidity, like Mongolia or Sri Lanka, while others have quite strong external liquidity, like Bangladesh. So it’s pretty difficult to identify a common theme. But across the range of indicators that we look at, the common theme is Double B minus and below ratings.

IFR ASIA: And how much does consistent messaging and clear marketing factor in the ratings?

ANDREW COLQUHOUN, FITCH: We have similar kinds of meetings to those the investors have, and yes, we like to think that we look through to the fundamentals. Where access to data is problematic, or there are issues with the quality of the data, the narrative around it can help to make the case. But we hope we’re not suckers for just a good story.

ARTHUR LAU, PINEBRIDGE: How a story is articulated is very important. When we met with delegates from Vietnam shortly after the yuan devaluation, we asked about their FX policy – the Vietnamese dong remains very strong and it was even stronger than the yuan at that point. It was very interesting to me at that moment when the government delegate said it didn’t have a policy. In fact it probably does have a policy, but the delegate couldn’t articulate it properly. But it demonstrates the inherent problems in poor communications which only undermines confidence.

FLORIAN SCHMIDT, SC LOWY: Currency risk should be at the front of investors’ minds, alongside political risk and transparency, when it comes to frontier investments. If you look back at the emerging markets crisis, if you want to call it a crisis, it really started with a very strong currency depreciation. You had the rupee in India in 2013, followed by the Russian rouble in 2014, and then in 2015 the Brazilian real, Turkish lira and South African rand.

In frontier markets, the Kazakh tenge dropped by 20% in one day. What does that do to the balance of payments of the country? What does that do to the sustainability of a debt stock if you decide to borrow in a currency other than your own?

In countries like Vietnam, and even more so Mongolia, where the management of the currencies seems to be opaque at best, this exposes investors in these countries’ offshore debt to very substantial risks.

ANDREW COLQUHOUN, FITCH: Imagine a country with a reasonably large sovereign dollar bond programme outstanding faces external liquidity stress. At what point do multilateral institutions start to think about moral hazard? When might they look for investors to be bailed in? Investors may be compensated for the risk they take, but if the multilaterals come in and take the risk off the table then that calculation unwinds a bit.

NORITAKA AKAMATSU, ADB: That’s a very tough question. Moral hazard for countries is an issue for the IMF but also for multilateral development banks like the ADB. We have a facility called counter-cyclical loans, designed for when a country is hit by a commodity crisis or a similar situation. We have to stand ready to support, and that is the latest product we have.

But then how can we make sure the country will follow the necessary reform programme? We have some other instruments, like programme loans. The World Bank has Development Policy Loans (DPL), a more conventional lending programme, lending against the promise to implement certain reform programmes. But for counter cyclical loans, how do we attach conditionalities? In fact we no longer call it conditionality, we call it the policy trigger, but it’s similar, basically a less stringent version of the conditionalities of the past. But it’s weakened our leverage and there is a question as to how we guard against moral hazard. It’s a judgement call in many cases.

FAISAL AHMED, BANGLADESH BANK: Many of these things happen at such a fast pace, you absolutely have to weigh it based on the specifics. So it’s very difficult to give a specific answer to such a general question. But my sense is that even the multilaterals’ views, including the IMF’s, have evolved. The views in the 1980s and ‘90s are different to those of the last five years.

Recent views have become more nuanced. The multilaterals are much more aware of this difficult trade-off now than they were 20 or 30 years ago. Partly that reflects the changes in global integration. It’s a much more fast-paced world, so the trade-off is more complicated. But the good thing is that multilaterals are much more aware of this issue.

IFR ASIA: Conditionality has never been popular, but if you think that sovereign bond investors may have to take the hit, then sovereign bonds become a less attractive investment. Has that already happened? After the eurozone crisis, and the situation in Argentina and elsewhere, is sovereign debt still seen as a safe asset class?

ARTHUR LAU, PINEBRIDGE: While I am a strong believer in the market being more efficient than any individual, there will be situations where the market breaks down. Ten years ago or more, Argentina started restructuring its sovereign bonds in order to avoid an outright default. A decade later, Argentina still faces a restructuring. So you have to balance both fundamental and technical considerations.

We assume it is always possible that a country will default, that is the nature of credit – however unlikely. So we analyse the sources of payment, the willingness and the ability of credits to make those payments and – especially in emerging markets – the domestic political situation. Some sovereigns prefer domestic investors over international investors, while for others it is the other way around, depending on the motivation and the policy of the government.

Ultimately it’s a basic credit assessment. Some investors may want to see a track record before they can be comfortable with the price. Sovereigns need to build a track record to gain the confidence and trust of investors, which will help them for subsequent issues if they are going to rely on international issuance. If they try to save pennies today by not honouring their obligations, they will end up paying more in the future, because the market does not forget.

IFR ASIA: Andrew, were you thinking of any particular examples of IMF assistance for countries borrowing in the international markets?

ANDREW COLQUHOUN, FITCH: We can all think of examples of countries that have accessed dollar markets and then subsequently turned to the IMF.

Typically, when we visit a country to do a rating review, we will meet with the authorities, and if there’s a resident fund representative, we often meet them too. If there’s no fund programme then the IMF representative will usually be quite stern, emphasising the need for reforms and to fix the budget. As soon as there’s a programme in play the tone usually shifts. This is not about the IMF specifically but multilateral institutions as a group. The tone can change and become much more positive, which is presumably because a rating downgrade could make a situation more difficult while they’re trying to stabilise it.

IFR ASIA: Coming to some of the alternatives to the dollar market, what opportunities are there for a country looking to borrow or attract new investors in its own currency? That is the holy grail, where possible, but how realistic is it? What’s the ADB’s experience in helping stimulate local markets?

NORITAKA AKAMATSU, ADB: ADB definitely encourages countries to develop their local currency markets. Even where countries are eligible for concessional resources, we will warn them that those resources come with foreign exchange risks, as well as flexibility risks. Of the four countries we are looking at that have access to these concessional resources – Bangladesh, Cambodia, Laos and Myanmar – only Cambodia is now still classified as a low-income country. Bangladesh and Myanmar last year joined the middle-income club, which means they are moving towards blend status. Then they have to start preparing for diversification of their funding sources, including developing their domestic currency markets.

When you look at gross national income (GNI), which is one of the benchmarks used to classify countries, Bangladesh is only a little bit ahead of Cambodia, so Cambodia should soon also join the middle-income club. Then it will have to start preparing for domestic currency-based funding too.

Vietnam is a good example. It was growing very fast and it anticipated the issues raised by joining this blend country club and started preparing its domestic market years ahead. By the time it joined this middle-income, blend country club it already had an essentially functioning domestic government bond market.

For now, Laos is still basically only using treasury bills, as is Myanmar, though it is aware of the need for domestic currency markets and is making some efforts there. Among those ASEAN countries, one should look at the experience of Vietnam as the example to follow. That’s the message we try to deliver.

FLORIAN SCHMIDT, SC LOWY: There have been a couple of very good examples of how Asian countries manage to attract international investors in their own currencies, but I think the best example was the global peso market. The Philippines did some spectacularly successful transactions. At times I accompanied the secretary of finance on his roadshow in Europe and everybody was aware of global pesos. A number of European accounts invested.

About 30% or more of Indonesian rupiah-denominated government bonds were held by foreigners during the best times. More recently, the CNH market is an example of investors looking at local currency bonds.

Among frontier markets there were a lot of relative value trades between onshore or dong-denominated Vietnamese sovereign debt versus dollar debt. There were quite a few people figuring out what the appropriate swap level should be.

We sold plenty of tugrik-denominated assets with credit-linked notes to global investors between 2007 and 2012. The tugrik at that time was stable, a perfect currency for a carry trade versus US dollars. Of course, given the correlation of the currency with commodity prices, that has changed quite a bit.

But from an international investor’s perspective, Asian – including frontier – currencies were attractive, as long as investors saw appreciation potential. As soon as these currencies go down you see selling, as with Indonesian rupiah bonds: international investors are the first out the door. The CNH market has become dormant, close to non-existent, given that the yuan is not appreciating any more.

So it’s an appreciation play, or possibly a carry trade if the opportunity presents itself. In the 22 years I’ve spent in Asia, I don’t think any investor has really bought this paper for the love of the currency, it’s about the commercial thinking behind it.

IFR ASIA: There has to be relative value in there somewhere. Arthur, how do you see it? What is your experience of the local bonds in your portfolio?

ARTHUR LAU, PINEBRIDGE: There are two considerations. One is whether we have a natural need, driven by our clients, for local market debt, in which case there is less concern about the FX mismatch or FX risk. Some clients are long the local currency anyway, so you just enhance the return from the local perspective.

For other portfolios it is more about how much potential alpha we will be able to generate from these local currency exposures. In normal circumstances that means looking at the appreciation trends of the currencies against different parts of the portfolio, which are dollar-based. So it’s basically an FX trade, and whether you can have a sufficient hedging mechanism to protect your downside, or whether the carry trade will be able to compensate your potential FX risk.

Putting that softer investment market perspective aside, the other consideration is the logistics. I have followed the Asian Development Bank’s work in local currency market development projects for many years, and have contributed to some of their local currency market surveys, given our exposure in the region. The common theme is that the market infrastructure just isn’t there yet, for example in terms of the settlement and custody arrangements, and also the liquidity of our counterparties.

In Asia, particularly Indonesia and Malaysia where there are basically no hurdles for you to invest, and more liquid and open markets like Singapore and Hong Kong, you can go in and out. There is no withholding tax and you don’t need a licence. But it’s subject to the volatility we have spoken about, driven by things like commodities or political risk.

So market infrastructure is very important to us. We want to know what we’re getting into, how easy it will be to get out, the liquidity characteristics, the size and types of issuer, the duration and the curve. Usually we invest in government securities first, but even then securities can be very different to what you see in more developed jurisdictions. All this needs to be understood, it isn’t just about market potential.

FLORIAN SCHMIDT, SC LOWY: Developing Asia’s local currency bond market has been at the forefront of everyone’s mind since 1998 – that is 18 years ago. So it’s mind-boggling how little has been achieved in terms of liquidity and creating hedging instruments. I’m not going to buy anything I don’t know I can exit if I need to, and I may not buy something if I don’t have a measure to hedge the risk, including currency risk. Pretty much nothing has been achieved in these two key areas over the last 18 years.

FAISAL AHMED, BANGLADESH BANK: We have to be candid and admit they governments dealing with very difficult issues. You can’t look at liquidity issues in isolation, for example, they’re linked with foreign monetary policy implementation, foreign exchange policy and political circumstances. All these issues are interlinked and there is a reason why they’re taking such a long time.

When I worked at a multilateral on the government bond market it was easy to write working papers, and offer ten sets of recommendations, but these are ultimately evolutionary processes. Western markets developed over decades. The evolution of bond markets starts with government securities and local currencies and will gradually move to the private sector. It’s like a fitness exercise: we make promises and then work throughout the year but we end up making the same promises again next year.

NORITAKA AKAMATSU, ADB: I think we need to give a little more credit to the countries in the region. We are discussing frontier markets, but the frontier markets of 15 or 17 years ago, right after the 1997 crisis, have seen their local currency markets develop to around 17 times the size they were on the eve of the crisis. That is 17 times bigger in 17 years. So in terms of size they did achieve something. Of course a lot of this can be put down to China and South Korea, but today even middle-income ASEAN members, like Malaysia, Thailand, Indonesia and the Philippines, have become fairly significant markets. In the context of the broader ASEAN Plus Three it’s small, but the markets in Thailand and Malaysia are healthy and diversified, and they deserve some credit for their size.

ADISORN SINGHSACHA, TWIN PINE: I would echo what has just been said about the importance of size, infrastructure and understanding the local custody arrangements, and the payment of interest rates. We have been trying to do just that in Laos. When you are in discussions with a corporate that is looking to launch a bond, but you don’t know the size, it is very difficult. We use a local financial advisor to do the market survey, and we end up having to do about three rounds, because you get different answers depending on how you ask the questions. In the end you come out with an issue of US$20m or US$30m equivalent in key bonds, but you can work on that for over a year without anything obvious being achieved, only small, incremental progress behind the scenes. It just takes a lot longer to get these deals out.

We talk about US dollar bonds and local currency bonds, but I want to touch on the third option, which is an alternative-currency bond. We see this in Laos and Thailand because they’re large trading partners. So you can see Thai baht bonds issued in Laos – and also in Myanmar. There’s a natural kind of hedge there.

I don’t know enough about Mongolia and China to say whether you will see it there, but if a big chunk of trading is in Chinese yuan it could be an alternative to a straight choice between US dollars or the local currency. These third-country, alternative currency bonds are something that smaller frontier countries should be exploring with their larger trading partners that are more established in the market.

To view all special report articles please click here and to see the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.