IFR ASIA: There has been some recent discussion on securitising some of the municipal debt.

DAVID YIM, STANDARD CHARTERED: Who wants to buy something that is based on some cash flow data that may not be available or isn’t transparent? That may be tough.

FERNANDO MAYORGA, FITCH RATINGS: We haven’t seen many securitisations of local government debt, because normally you can’t pledge taxes. You can’t put them into a box. That just leaves fees and they’re very volatile, because the revenues of local governments are so closely linked to land sales. That’s one of the problems, as well, for local governments in China.

RICHARD DAWSON, KPMG: There’s a huge dilemma there. The central government gathers the majority of tax but the local governments are still responsible for the vast majority of organisation and infrastructure costs etc. And that’s still the challenge. As long as you’ve got a unitary system of tax, I think some of these structures and mechanisms that Fernando has talked about are going to be very difficult.

In America, municipalities have the ability to raise taxes, or to change taxes, so that when they have a problem they can adjust their revenue base.

We just aren’t there in China at the moment. There are two critical pieces – one, that the tax regime, over time, gives local governments more responsibility for funding themselves and two, lifts their capacity to manage debt once they’ve got it.

It’s not just at the point of issuance, it’s also thereafter: how do you make sure you’re keeping investors up to date with events? That whole framework is still relatively weak outside some of the big cities. It’s all right when money is flowing around, but when it gets tight, this infrastructure is pretty critical.

IFR ASIA: Transparency is obviously important, but even in the property sector we’ve heard investors calling for more information when they already get sales data every month!

FERNANDO MAYORGA, FITCH RATINGS: Sometimes you get the information but it’s out of date, so by the time you get it you don’t really know what the situation is.

IFR ASIA: So should we believe the audited number from last year? That was Rmb15.4trn of debt, with another Rmb8.6trn of contingent liabilities.

FERNANDO MAYORGA, FITCH RATINGS: How deep is the iceberg? I don’t know. There may be additional debt that could migrate to local governments at some stage. But it’s difficult to see too deep. The water is a bit cloudy.

IFR ASIA: It’s kind of the crux of the matter, isn’t it? If you are going to bring more of these into the global capital markets, then people need to have faith in those numbers.

FERNANDO MAYORGA, FITCH RATINGS: Yes, and it would be useful if the audit was more granular. If, instead of having one big lump sum, we knew where the debt was, which provinces are highly indebted and which are not.

Some provinces can take on quite a lot of debt, because they have the revenues to back it up; others can’t.

DAVID YIM, STANDARD CHARTERED: International ratings are a way to encourage more transparency.

This is the standard expected by international markets. If you want to play that game, you have to follow that. Therefore some corporates actually use this exercise to improve transparency and efficiency internally. Consolidation can take ages in the bigger companies, so getting a rating opens them to a different way of thinking.

IFR ASIA: I wonder if the anti-corruption drive has anything to do with the push for greater transparency. Would an issuer look overseas for an international stamp of approval, perhaps?

FERNANDO MAYORGA, FITCH RATINGS: I imagine so. Some local governments don’t have the proper admin systems in place, so they may not bother unless the central government tells them they have to provide this information. It can also be a problem if they produce a figure that is higher than they told the central government before. There could be a lot of repercussions.

IFR ASIA: Is there much competition between municipalities – Beijing versus Shanghai or Chongqing, for example – as there is between public sector issuers in places like Korea?

BARRY FUNG, BNP PARIBAS: Different provinces have different characteristics. I think the best we can do is to provide the true picture to the rating agencies and let the bonds be priced according to the ratings.

But it is a challenge because, as you said, some entities may say that they deserve a better rating than others. This is why it is so important, as mentioned earlier, to get all the relevant data and to arrange for the government to meet the rating agencies.

IFR ASIA: If a province, or a vehicle, isn’t going to get the rating it wants, do they still want anything to do with the process?

BARRY FUNG, BNP PARIBAS: Everything is comparative. They compare with the local funding cost. If the rating gives them a competitive funding cost, they will take it. If there is a premium for the first issue, they may take into account their average cost, both locally and elsewhere, and other factors. If the blended cost is still acceptable, they will go ahead.

DAVID YIM, STANDARD CHARTERED: Different kinds of thinking come into play. For many finance people, funding cost is definitely the key consideration. They will simply compare offshore and onshore and go for whichever gives them the best deal. Or they may just forget about offshore because onshore is so liquid and it’s a lot less work.

On the other hand, there are some companies which want to take a look at the offshore market. Some of them may not be able to do an IPO, for example, so having an offshore bond is as close as they can get to the international route and enhancing their profile.

It may be that they are planning acquisitions, so tapping the offshore market and getting an international rating is a step forward – even though, at the moment, the pricing may not be as attractive as the onshore market. They will still make an effort to go offshore, because they have other reasons.

IFR ASIA: Part of the issue has to be whether it’s going to be a one-off issuance, or whether the borrowing is setting up a frequent programme.

DAVID YIM, STANDARD CHARTERED: What we normally see is that, once an issuer has done a first offshore issuance, they like having that regular funding channel to supplement whatever they can get onshore.

BARRY FUNG, BNP PARIBAS: International recognition is a very important factor. Also, once you set up the platform, it can be used for an IPO, acquisitions or follow-on issues. There are some costs initially, but in the long term you get the payback.

RICHARD DAWSON, KPMG: This is also a function of timing. Long term, the Chinese have been focused really strongly on the municipal bond market in the US, as a vehicle to fund infrastructure and municipalities. The direction of travel is there, but it may take some time. It also depends on the economy in China. Things may move quicker if the economy isn’t quite so robust.

I know that some of these municipalities have visited, for example, debt management offices in US provinces or cities, or in Germany, to see how it’s done elsewhere.

IFR ASIA: Let’s hope they were visiting Frankfurt, not Detroit. Fernando, you have a global remit but you sit in Barcelona. Are there any lessons from Europe that China can take on board?

FERNANDO MAYORGA, FITCH RATINGS: Well, in Spain we had a very serious economic crisis and the government pushed for more transparency and control. We now get monthly figures on budget execution and budget revenues from local governments on the ministry’s website. We get debt levels from the central bank, and the government is very clear which municipal companies should be counted as local government debt and which ones should not be counted, on the basis of profitability and external revenues. There is a much clearer line as to what is public debt, and what is commercial. So that’s good.

In this way, even some European countries could improve their transparency. German states are the big borrowers. And yet their level of accounting is not that strong yet, because they only do cash accounting, they don’t do accrual accounting, which we’re going to see in China. If China moves the way it wants to move, it will have a very robust accounting framework in the next four or five years.

You can also look at Australia, which is a very mature bond market. Australian states don’t borrow from banks; they borrow only from the capital markets and rely on market discipline. The Commonwealth government doesn’t say you can only borrow X percent of your revenue, it’s down to the capital markets.

RICHARD DAWSON, KPMG: Some parts of Europe are interesting for different reasons. The UK has sort of moved to a central government issuance model, in which they are granting money to the regions. Housing associations, for example, used to be all bank funded but now, because the bank market has dislocated, they are frequent issuers in the bond market. The pension funds love that, because these are long-term sterling assets.

I know the Chinese are looking very closely at that, because they couldn’t believe that social housing can lead to robust capital markets issuance. You find parallels where China might benefit from changes in its own market, like the move from banks to bonds. Social housing is a good example because there’s a huge amount of it in China. At the moment, it’s funded from the government balance sheet. Over time, you can probably shift that to the capital market.

IFR ASIA: Since we’re looking at past crises, is there any chance of a crisis in China? There have been onshore defaults even from state-owned issuers. Is this something that people should be worried about when it comes to the LGFVs?

BEN YUEN, BOCHK ASSET MANAGEMENT: Yes, I have thought that on a few occasions.

I think if the onshore default rate increases, that is common in other markets and a healthy development. It will remind people they should be more careful about pricing risk before they invest in a bond. As I mentioned, a Single B rated bond, for example, could yield 5% more offshore than it does onshore for a five-year tenor. That type of pricing discussion needs to come from the asset management community.

IFR ASIA: Would a default set a useful precedent in the municipal market? It would make people do some sort of credit work there, at least.

FERNANDO MAYORGA, FITCH RATINGS: There is the problem of moral hazard everywhere, but I think a default at the provincial level will not be allowed to happen in the near term, because it would estabilise the whole sector too much. I also don’t expect any defaults on strategic LGFVs. They may allow them for the more commercial vehicles that are not so closely linked to local governments, but not for those that are funded by local governments.

If the central government wants to instil market discipline, that’s the way it has to go, but I don’t see it happening.

IFR ASIA: It also seems that the investor base has a bearing on whether something is allowed to default. Retail investors seem to be always paid back.

RICHARD DAWSON, KPMG: That’s not unique to China! Defaults happen everywhere, but they are managed in a different way.

We are aware of situations where local governments try and bring companies together, or sit down and talk to banks about a rescheduling. Sometimes it’s a reaction to a potential issue, swapping short-term loans to medium-term bonds, and often the debt stays with the same lender. It’s a much more managed process.

Things have to go wrong for people to rewrite the rules. But I agree, fundamentally, that doesn’t mean there will be a wholesale correction in the local government market.

BEN YUEN, BOCHK ASSET MANAGEMENT: Having some defaults is healthy for the development of the market. If this was a perfect, market-driven environment, these things would happen.

FERNANDO MAYORGA, FITCH RATINGS: That’s true, but look at how many there are in the US. The default rate in the US municipal market is very low, but investors do appraise bonds very differently, according to their credit quality. That’s not happening at the moment in China, because they don’t know what the credit quality of local governments really is.

DAVID YIM, STANDARD CHARTERED: Yes, but for bond issuance in China you need to get approval from government before you can issue. So that’s why a lot of investors have this sort of thinking, that it is implicit support from the government. That thinking has to change for the development of the market.

IFR ASIA: Yes, my question around it is whether offshore investors do their own homework on these kinds of deals. We have seen it before with GITIC in the late nineties, where everyone assumed that they had a guarantee from China, and it turned out that that wasn’t the case.

DAVID YIM, STANDARD CHARTERED: Yes, but times have changed. Back then, China was not as strong, reserves were much lower. If you look at it now, a lot of these LGFVs and other SOEs are able to issue with keepwell structures – not a guarantee – so you can see that investors believe in this market, and in these types of issuers. The keepwell structure is not tested, and we know that it’s not as strong as a guarantee, but for certain type of issuers this is accepted. The ratings do reflect the keepwell, in some cases, but it’s only one, maximum two, notches difference.

RICHARD DAWSON, KPMG: Yes. But it’s a function of liquidity as well. The reality is, if people have money to invest then this can impact lending behaviour. They see the keepwell, so to them it’s perceived just like a guarantee.

DAVID YIM, STANDARD CHARTERED: There has to be a belief that, if the worst comes to the worst, the local government will step up – even though there’s no guarantee from the onshore entity at the company level, let alone local government support. There has to be that belief, otherwise you will not buy those bonds.

IFR ASIA: That’s the same reason why Chinese AT1 bonds trades at 4.5% even though they’re supposed to be loss absorbing.

Ben, do you have a view on relative value? There’s been lots of issuance from Beijing, for example. How do you put them in some sort of hierarchy?

BEN YUEN, BOCHK ASSET MANAGEMENT: Yes. First, we look at the company, the SOE, to see the percentage directly owned by the central SASAC or that type of central institution. It it’s 100% owned, then it should have a much closer relationship with the central government.

In the worst case, if government ownership falls to less than 50%, then this type of company will become a corporate type of credit, with different banking relationships and pricing.

IFR ASIA: But how would you view a local government, LGFV bond, versus, say, a Chinese bank?

BEN YUEN, BOCHK ASSET MANAGEMENT: I think there’s quite a difference. For the big four commercial banks that are seen as too big to fail, the level of transparency is much greater.

If you look back to the early 2000s we saw strong government support in the form of capital investment into the banks. But on the other hand, looking at an LGFV or municipal bond, we should be getting less support from the central government, compared with the commercial bank.

So we need more detail on the risk profile to distinguish between different provinces. We need to look at the balance sheets.

This is a healthy trend towards transparency, and I think demand for municipal bonds is definitely increasing, but there needs to be more open data for investors for this to be a really healthy development.

IFR ASIA: So relative value is not easy.

BEN YUEN, BOCHK ASSET MANAGEMENT: It’s not easy at the moment. Honestly. We don’t have anything to base it on.

DAVID YIM, STANDARD CHARTERED: Even though some of these LGFVs are rated similar, when these bonds are priced, they are still different. You can’t just say, oh they are Single A flat or A minus, so they all trade the same, that’s not the case. Transparency and strategic importance to the government are important.

FERNANDO MAYORGA, FITCH RATINGS: It’s a quite recent development as well. I mean, banks have been issuing for many years, and investors have a good feel for things there. This is a very new market.

RICHARD DAWSON, KPMG: On the issue of default, if you look at the private sector, or real estate sector, the experience of offshore bond investors in a default situation has not been very good. If you take that parallel through to a government situation, I think a government would have to look very carefully at a similar situation, because it could create a real impact.

If the issuer is private, or quasi-private, I think investors don’t expect support when things go wrong, even though they may have been treated in a grossly subordinated way. If that happened in a municipal situation, you could have a much bigger issue for China. That would have a ripple effect right through the municipal and sovereign financing function.

I think they would look at these things pretty carefully, and then investors will get the right outcome. But the experience of offshore bond investors in a default situation in China to date has been very tough. We know that onshore creditors often rank super senior.

IFR ASIA: How does the rating work? You might have the same rating for a bank and a lot of government vehicles, but very different prices.

FERNANDO MAYORGA, FITCH RATINGS: We have a corporate team that also looks at some of these SOEs. But from the public finance perspective, the ones that we look at tend to be the strategic or policy ones. For those we have a top-down approach, essentially. So we look at the local government, we do an internal assessment or internal rating for them, and then we either equalise, or notch down, depending on the link. There, we look at factors like strategic control, and the funding base. Some of them tend to be equalised, or we will notch down by one or two notches.

If we were to look at the standalone credit, most of the ones that we look at tend to probably be quite low, probably BB or BB+. They wouldn’t get to the right rating unless we enhance the rating, or – as we do from the international public financing perspective – we notch down. The ones that we’ve seen coming to the international markets so far are the top tier, the cream. And they’re very key to the city, because either they have a very important infrastructure role, or a strategic role, and therefore we can say that they are practically an arm of the city.

IFR ASIA: When we see any lower ratings come out, then that means it’s not quite so strategic?

FERNANDO MAYORGA, FITCH RATINGS: That’s right. If it’s done from the same municipality, then you’ll get to see different levels. Unfortunately, I would love to publish the international rating of the city behind it, but we’re not there yet.

We always ask to meet the local government officials, because we need to assess the city, and we do get a lot of information, much more than is available publicly.

BEN YUEN, BOCHK ASSET MANAGEMENT: I do feel that the rating agencies’ views on China and LGFVs is a lot more open – I don’t want to use the word ‘aggressive’ – than it was two or three years ago. After the audit of the LGFVs, we expected ratings on some of the second-tier or third-tier cities to be much lower than the ratings that we’ve seen recently.

That’s why we have some issuers coming to us, saying that they are not treated fairly because they got their rating four or five years ago and they were rated as a regional SOE, not an LGFV. I think the methodology and the view on LGFVs has definitely changed in the past year or so.

FERNANDO MAYORGA, FITCH RATINGS: Yes, definitely. The central government has gone out there to put some order into what’s going on, and that’s actually given the rating agencies a bit more comfort. As more come out, then you become more familiar, too. Certainly if you’re rating the first one you tend to be a bit more conservative, and then when you get to know more of the market, and how things operate, then you adjust the ratings.

IFR ASIA: So if you’re an issuer, you’d rather be an LGFV, not an SOE!

DAVID YIM, STANDARD CHARTERED: Some of these SOEs would have a higher rating if they were rated now rather than a few years ago. The methodology, especially towards entities with a strong linkage to government, has changed. But the rating agencies aren’t going to go back and move everyone another two or three notches up.

FERNANDO MAYORGA, FITCH RATINGS: I suppose there has to be a rationale for upgrading, but sometimes we do reassess. Not so much in China, but in other countries where we get to know more of the market.

We do rate on the basis of support. But your knowledge of support changes over time, and as a result of central government directives. If we expect a certain level of support, then it doesn’t happen, then our view of the sector will change, and we take rating action accordingly, for the whole sector.

DAVID YIM, STANDARD CHARTERED: One interesting observation I have found from Chinese issuers, is that these government-related entities are encouraged to act more like commercial entities in the domestic markets. They may not like to be called an LGFV. For the offshore market, however, if they are strategically important to the government, like the LGFVs, their ratings maybe equalised to whatever the implied rating for that particular city.

RICHARD DAWSON, KPMG: Some of these issuers are quite diversified as well, and can be the main funding vehicle for a particular province. They’re not unattractive issuers, from a portfolio point of view.

BARRY FUNG, BNP PARIBAS: Sometimes these companies would like to explore a way to have a credit rating which is better than the municipal government!

IFR ASIA: We’ve covered a lot here, so to close it off let’s see if anyone will dare put a number on how many LGFVs are going to make it to the international market.

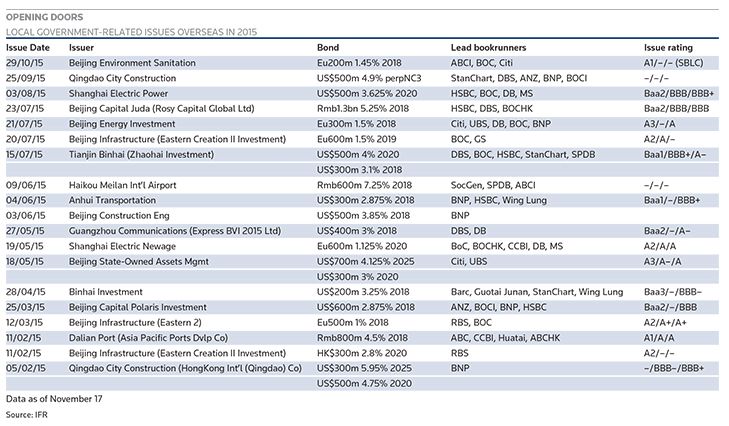

BARRY FUNG, BNP PARIBAS: This year so far there are five that can be defined as an LGFV: Beijing Infrastructure, Qingdao City Construction, Anhui Transportation, Guangzhou Communication and Tianjin Binhai. My view is that infrastructure companies like these will have huge funding needs, especially under the new One Belt One Road policy, and they’re happy to explore the overseas market. But it really depends on the market situation, the cost of funds, and if they need the money urgently.

IFR ASIA: So if we’re on five in the first three quarters of this year, where do you think we’ll be this time next year?

BARRY FUNG, BNP PARIBAS: I would think maybe as good as this year, because some of the infrastructure companies really do need funding. Some companies have offshore acquisition plans, so it is an obvious opportunity for them to raise a sizeable amount of funds at an acceptable tenor.

RICHARD DAWSON, KPMG: I think the direction of travel will be pretty quick. If you look at where the Chinese were three years ago, in municipal finance generally, and where they are today, I think they’ve come a long way quite quickly. Some of the directives that came out on municipal bonds and PPP are pretty ambitious. Now, as usual in China, they have to fill in the details behind that, but you’re going to see more municipal finance in the capital markets, and I think investors offshore have the appetite for this as they look for diversification.

We’re probably not that far away from one of the provinces or cities issuing in the international market. That could come faster than we think. But a lot of it will come down to factors including politics, and the general state of the economy on the mainland.

So it’s the usual caveat, but my sense is there’s a huge ambition to really sort this out. Transparency is a big driver, but it’s also about urbanisation. There’s a huge amount of infrastructure to build, and the central government can’t continue to fund all of that.

I’m not going to predict, because there’s better people for that here than me, but I’m quite excited about this as a topic.

DAVID YIM, STANDARD CHARTERED: There may be around 10 LGFV issuers in total so far. I do agree that there will be more. There are thousands of LGFVs, and there are so many that still want to take a look at the offshore market. But of course, the external factors have to be right. After the NDRC regulation changes, we expect SAFE will also support overseas issues especially with onshore remittance, and if remittance is made easier, then definitely there will be more.

There are still a lot of companies that want to look at the offshore market. They will not, or cannot, use it as a main funding channel, but they will supplement their funding in dollars, euros and also in CNH – if that market returns. So I expect more to come to the market.

BEN YUEN, BOCHK ASSET MANAGEMENT: Yes. The onshore market is already starting to see municipal bonds, so that will bring more focus for the investor base. There are more good mechanisms for municipal issues, and that allows the local governments to find better ways of raising suitable funding. Investors like that, and I think they will be interested.

On the other hand, I think there is a risk of over-supply in the market. So my perfect number would be one per month. I think that’s reasonable.

IFR ASIA: There we go. That’s a good target. Fernando, what do you think?

FERNANDO MAYORGA, FITCH RATINGS: I think there certainly will be more issues than we’ve done so far. We’ve got some ratings out there that are just waiting for the window to open, so hopefully they will come out in the next month or so. There are certain cities with large investment needs that would probably go out and borrow, and some infrastructure companies, so there’s a lot of potential.

IFR ASIA: Gentlemen, thank you all very much for your time.

To view all special report articles please click here and to see the digital version of this report please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

| Opening doors | ||||

|---|---|---|---|---|

| Local government-related issues overseas in 2015 | ||||

| Issue Date | Issuer | Bond | Lead bookrunners | Issue rating |

| 29/10/2015 | Beijing Environment Sanitation | Eu200m 1.45% 2018 | ABCI, BOC, Citi | A1/–/– (SBLC) |

| 25/09/2015 | Qingdao City Construction | US$500m 4.9% perpNC3 | StanChart, DBS, ANZ, BNP, BOCI | –/–/– |

| 03/08/2015 | Shanghai Electric Power | US$500m 3.625% 2020 | HSBC, BOC, DB, MS | Baa2/BBB/BBB+ |

| 23/07/2015 | Beijing Capital Juda (Rosy Capital Global Ltd) | Rmb1.3bn 5.25% 2018 | HSBC, DBS, BOCHK | Baa2/BBB/BBB |

| 21/07/2015 | Beijing Energy Investment | Eu300m 1.5% 2018 | Citi, UBS, DB, BOC, BNP | A3/–/A |

| 20/07/2015 | Beijing Infrastructure (Eastern Creation II Investment) | Eu600m 1.5% 2019 | BOC, GS | A2/A/– |

| 15/07/2015 | Tianjin Binhai (Zhaohai Investment) | US$500m 4% 2020 | DBS, BOC, HSBC, StanChart, SPDB | Baa1/BBB+/A– |

| US$300m 3.1% 2018 | ||||

| 09/06/2015 | Haikou Meilan Int’l Airport | Rmb600m 7.25% 2018 | SocGen, SPDB, ABCI | –/–/– |

| 04/06/2015 | Anhui Transportation | US$300m 2.875% 2018 | BNP, HSBC, Wing Lung | Baa1/–/BBB+ |

| 03/06/2015 | Beijing Construction Eng | US$500m 3.85% 2018 | BNP | |

| 27/05/2015 | Guangzhou Communications (Express BVI 2015 Ltd) | US$400m 3% 2018 | DBS, DB | Baa2/–/A– |

| 19/05/2015 | Shanghai Electric Newage | Eu600m 1.125% 2020 | BoC, BOCHK, CCBI, DB, MS | A2/A/A |

| 18/05/2015 | Beijing State-Owned Assets Mgmt | US$700m 4.125% 2025 | Citi, UBS | A3/A–/A |

| US$300m 3% 2020 | ||||

| 28/04/2015 | Binhai Investment | US$200m 3.25% 2018 | Barc, Guotai Junan, StanChart, Wing Lung | Baa3/–/BBB– |

| 25/03/2015 | Beijing Capital Polaris Investment | US$600m 2.875% 2018 | ANZ, BOCI, BNP, HSBC | Baa2/–/BBB |

| 12/03/2015 | Beijing Infrastructure (Eastern 2) | Eu500m 1% 2018 | RBS, BOC | A2/A+/A+ |

| 11/02/2015 | Dalian Port (Asia Pacific Ports Dvlp Co) | Rmb800m 4.5% 2018 | ABC, CCBI, Huatai, ABCHK | A1/A/A |

| 11/02/2015 | Beijing Infrastructure (Eastern Creation II Investment) | HK$300m 2.8% 2020 | RBS | A2/–/– |

| 05/02/2015 | Qingdao City Construction (HongKong Int’l (Qingdao) Co) | US$300m 5.95% 2025 | BNP | –/BBB–/BBB+ |

| US$500m 4.75% 2020 | ||||

| Data as of November 17 | ||||

| Source: IFR | ||||