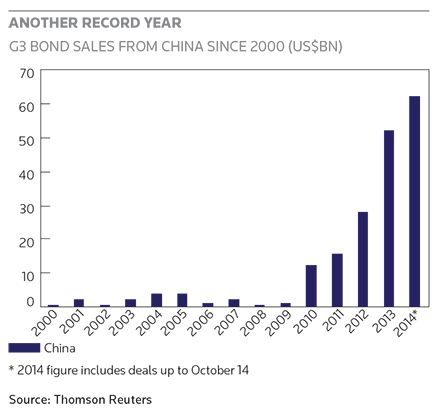

IFR: Welcome. The outlook for China’s corporate sector in the international bond markets is on everyone’s mind after a surge of offshore debt issuance from China over the last couple of years. So to kick things off, what’s behind that trend, and is it going to continue?

WALLACE LAM, HSBC: On one hand, there is a need for capital among fast-growing corporations in China. On the other hand, China corporate bonds offer some very attractive yields as compared to similarly rated entities from around the globe. When there’s a demand for capital and a supply of capital, that’s why we have been seeing a surge in volumes.

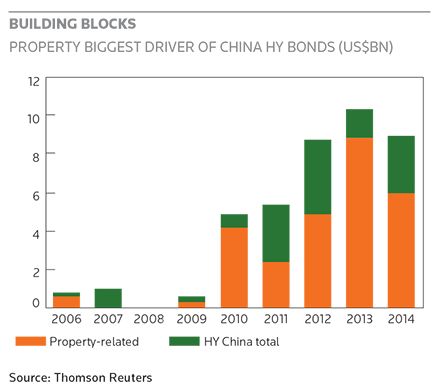

IFR: Does that apply to high yield as well?

WALLACE LAM, HSBC: Absolutely. We are seeing an increasing number of high-yield transactions year on year. Last year was a record year and this year is likely to be the same.

IFR: From the latest numbers I ran, around US$16bn was issued in high yield out of China last year, and this year we’re at US$12bn. We’re down a bit but there could be more to come. Patrick, is that a fair assessment?

PATRICK LIU, UBS: Yes I think so. A number of factors account for the surge in volume. In general, bankers, lawyers and rating agencies have more flexibility in structuring high-yield products. Structural changes such as keepwell agreements allow rating agencies to give a fairer assessment of the issuer itself, and with that some corporates based in China are now able to issue bonds offshore for the first time.

The regulatory environment has also become more benign. For example, the FX regulator, SAFE, has published new rules which allow onshore entities to provide offshore guarantees for financing which, potentially, will allow a much larger client pool to access the market. It is already a big driver of volumes in the market.

WALLACE LAM, HSBC: That’s a very good point. The keepwell structure was actually introduced by HSBC in 2012 with the first issue for Gemdale, and it has become the mainstream issuing structure for mainland corporate entities, particularly for companies that want to bring the proceeds of these issues onshore.

IFR: Well I certainly have some questions about the value of these structures, but let’s come back to that later in the discussion. The big issue we’re discussing here is whether the outlook for China’s economy and corporate fundamentals can support this surge in borrowing.

KALAI PILLAY, FITCH RATINGS: When you talk about this huge surge of borrowing, a lot of it is replacement capital. People are borrowing offshore instead of traditionally borrowing onshore. Are these companies overextending themselves or leveraging their balance sheets? No. Some companies are leveraging more because they’re growing, and obviously there will be some odd ones here and there that get out of control, but generally speaking that part of the equation is sustainable. Going offshore to get longer-term maturities and a lower cost of borrowing is totally sustainable. The fickleness of domestic bank lending is also an issue for many corporates, especially high-yield issuers. So that side of the equation is fine.

The other side, the outlook for investors, I’ll hand that across the table. Will there be demand for Chinese corporate bonds – is that sustainable? From my perspective it seems that Chinese bonds still offer higher yields relative to other reasons – including Indonesia, surprisingly. So why wouldn’t investors want to chase that additional yield?

IFR: That does sound like a question for you, Ben.

BEN YUEN, BOCHK: If we look back at the first three or four months of this year, when the Chinese economy was slowing quite substantially, we saw a lot of bad headlines and a lot of noise around the Chinese corporate sector. Particularly in March/April we saw the risk premium increase, especially in the property sector, and we have had to ask ourselves what type of risks we are facing. Are we facing the risk of increased gearing? Are we facing liquidity risk? All of those questions actually come from the macro picture.

The bottom line is that a different macro outlook will drive different risk premiums, so from an investor’s point of view we have to pick carefully to justify the value of our investment. Bad news in the market doesn’t necessarily mean a bad investment environment, but on the other hand if the market is too bullish we have to think whether that is a good time to be investing.

WALLACE LAM, HSBC: Let me answer that by saying, further to Kalai’s comments, that we see that China-related credits offer a premium over similarly rated entities in more developed markets such as the US and Europe. But if you look at the historic default rates from China it’s actually on par with the US and lower than those in Europe and Latin America. What you also find is that covenant packages for Chinese high-yield companies are actually more robust as compared to their US counterparts. So when you have yields that are higher, a default rate that is lower, and the covenants that govern the behaviour of the company are more robust, there’s value, and that is obviously one of the contributing factors.

IFR: So investors are getting a good deal, in that case.

BEN YUEN, BOCHK: That’s definitely a good point. We always compare corporate credits not just with Asia but also with the US and Europe, and we have to input a couple of things: one is the fundamentals of that region, and two is the risk premium.

If you go back to early this year, European and US high yield was outperforming Asian high yield, definitely in the property sector, so the spread differential between Europe or the US and Asia widened out quite substantially. At its peak it was at its widest in the past five years, excluding October 2011 and excluding 2008. So we asked ourselves whether the market was pricing in too much good news in Europe and the US, and whether it was pricing in too much bad news in Asia and in the Chinese property market. We shifted our focus towards Chinese property in April and May. That was a judgement of value versus the fundamentals.

IFR: That must be good news for the two gentlemen on my right. Do you agree that too much bad news was being priced in?

MICHAEL LEE, GUANGZHOU R&F: In terms of the macro picture, we’ve been dealing with the macro and the cyclical nature of the property sector for quite a while now, and the way we manage is on more of a long-term basis. If you react to all the short-term cycles it becomes a bit hard to manage the business, when our development cycle is 12, 18 or 24 months. So we plan for the medium term and the long term. As Kalai mentioned, the offshore market is a way for us to term out the financings, so it doesn’t become a two-year or three-year horizon, it becomes a five-year or seven-year horizon. So I think that has helped us manage the macro changes and the policy changes. It has helped us plan the business.

We can’t always time the market and time the investments, but in the last 10 years, as the markets suggest, there haven’t been that many defaults. Rates have been coming down for us as issuers, and I think people are getting to a point where the market is becoming more efficient. Macro or policy wise I think people are pricing that in, and we take a look at the market and assess our own development cycle and hopefully mitigate some of the short-term uncertainties.

IFR: Have your financing needs changed at this point in the cycle? Are you slowing your development plans because of declining sales?

MICHAEL LEE, GUANGZHOU R&F: For us, there’s always a balance between slowing down too much and maintaining a development cycle either for growth or to maintain your own scale. There’s always a balance, and that balance will come back to the availability of financing and the amount that you need to sustain that growth or maintain that growth. If you have achieved a certain scale you need to access the markets to maintain that scale, and we’ve seen the investor market gravitating towards the larger players – more so this year.

Having that advantage means you can tap the market for slightly larger sizes than you could historically, with mid-size players looking at US$500m and above now rather than US$300m–$500m in the past. Definitely the appetite is larger, both on the investor side and on the corporate side, but investors are certainly gravitating towards the better-quality and larger players. If the market does deteriorate than those players are going to have more flexibility in terms of their operations.

IFR: is that the same for you, Albert?

ALBERT YAU, CIFI: When we look at the industry outlook, we believe the growth in demand from the middle class in China for housing should be sustainable in the markets where we are focusing – the big cities, first purchase, first upgrade type of market. The industry has been undergoing consolidation for the last three years, but there are still too many property developers in China. The ones you see in the bond market are the bigger ones, and even at this stage we see differentiation, as Michael just mentioned. The differentiation, in fact, is getting more distinct. The range of credit spreads for developers even with the same rating can be as much as 300bp. That means the market is getting more sophisticated. The market itself has become more able to appreciate the credit of different developers. That is definitely a good step for our sector.

In our case, our business model requires us to sell our properties in a short cycle and then go into the land market to buy land within, say, three or four years, so each year we have funding needs based on both our cash inflow from the property sales as well as from the financings. We see offshore funding, including the bond market, as becoming more likely to replace onshore funding. We are a relative newcomer; we were listed less than two years ago. Like any other unlisted company in the sector, we were only accessible to the higher-interest trust market before. One third of our exposure before the IPO was in the trust loan market, other than that it was the onshore bank construction loan market. Within the last two years we have almost replaced the trust loans with bonds and syndicated loans raised offshore.

I also see a trend – as Kalai mentioned – that access to construction loans is getting harder and more expensive, so there is an opportunity of using, for example, the Dim Sum bond market to gradually replace the onshore loans.

IFR: Is there any evidence of stimulus in China? We’ve seen some liquidity injected in the top five banks, but the property sector is very much affected by policy.

MICHAEL LEE, GUANGZHOU R&F: From our perspective the recent policy changes, leaving aside the financing market for the moment, have been more structural. Rather than focusing on pricing changes or policies restricting capital for developers, it’s about making affordable housing, or relaxing purchase restrictions in cities where they may not be relevant at this particular point in time because the population is growing or there is a structural need for new housing.

In the financing market, as Albert mentioned, things are definitely getting tighter. The scrutiny by banks in the construction loan market may be higher than in the past, but it’s still focused on lending to the better players. I don’t think that financing is flowing to everyone in the sector – nor is it meant to – but it is providing alternatives for certain businesses. The onshore market is still reliant on construction loans, trust financing and, more recently, the perps, but for us to maintain a solid balance sheet we still need to be focusing on longer-term money and that will come back to US dollars or Dim Sum, which is now maturing from three years to four years with more investors able to buy than there were a few years ago. In Dim Sum, the first wave was about using your RMB deposits, and the next wave is about looking at the RMB as a source of more sustainable capital versus the Hong Kong dollar or any other investment. For us, the end result is cheaper financing offshore, longer-term financing offshore, and more access offshore.

WALLACE LAM, HSBC: To echo a couple of key points, the investor base is certainly deepening. In the property sector alone, there are probably 50 major issuers but at the latest count there’s more than 20,000 developers in China. So what investors offshore are seeing is probably the cream of the crop. These companies are larger sizes, have better access to capital. When the overall market is experiencing some volatility – if you look at the overall market the sales for this year went down about 10% year-to-date versus last year. Some companies within that space are still growing, even when the pie is shrinking. They are growing at the expense of the smaller players, and therefore some consolidation is inevitable. We don’t need 20,000 developers in China. For those who do their homework, it could be rewarding.

IFR: So is consolidation going to keep offshore financings going? If sales are falling you would expect less overseas funding, wouldn’t you?

KALAI PILLAY, FITCH RATINGS: This is an iceberg you’re looking at. You think it’s a big sector, but it’s really so much bigger. Consolidation is going to take people out of the bottom, but the big players are still growing. They need capital. Even if you’re reaching a steady state, the level of competition in the sector will still be very high, and it’s going to be even harder to eke out an extra percentage point of margin. Funding costs are a big component of your margin, so people like Albert and Michael will be working extra hard to find a lower cost of funding, and inevitably that is going to be offshore.

You can talk about the perps onshore, but markets are not very deep, so it’s very unlikely that onshore markets are going to be provide you a lower cost of funding. The search for structures that can give you a lower cost of funding offshore is going to continue, even in a downturn or even in a steady state environment. For the good property developers, it’s all about getting proper cost of funding.

WALLACE LAM, HSBC: And getting access to capital is also very important. If you look at the figures, the lending market grew by Rmb385bn in July this year as compared to market expectations of Rmb780bn. It was way below expectations for credit growth. That means capital from banks is very valuable in China, and companies that have access to cheaper funding offshore have an advantage. The PBOC had a quantitative measure rencently with a Rmb500bn injection into the banks.

IFR: Is it still significantly less expensive to issue offshore, assuming you are able to issue at a similar size and tenor in the onshore bond market?

ALBERT YAU, CIFI: The offshore bond market is a market that no listed developer can ignore: it is getting more and more important. As I look at the 40–50 issuers in our sector, other than the blue-chip China developers who might get 90% of their total lending from bonds, most of the developers like us have about 40% from offshore funding – maybe even less for the newer companies. The industry has been undergoing fundamental changes over the past three years, and the sector is adjusting its business model from high margin to high volume. That means the cost of funding is getting more and more important. It is key to the differentiation between profit margins nowadays. So when we look at funding costs at different maturities, there is consistently a 200bp difference between onshore and offshore. We compare five-year US dollar bonds with the trust market in China, or three-year Dim Sum with the domestic construction loan market in the same denomination in RMB, consistently it is less expensive offshore.

For the big players like China Vanke, their offshore portion is still smaller, so from the supply side we would expect more developers to come out. From the demand side, too, we can see the market is getting more sophisticated, being able to differentiate between players and assign different costs to different developers. This is definitely a good development.

MICHAEL LEE, GUANGZHOU R&F: When you look at the yields for the mid and larger players, they’ve come down because investors have become more selective and are not applying the same standard to all companies in the sector. If you come back to the steady state scenario, then the cost of capital becomes more important. No longer are you chasing volume growth or sales growth, you’re chasing profitability, and in that case if you can maintain or lower your funding costs then there is a mid-point between investors and issuers where you are able to come to the market. But if you are still chasing higher margins and your cost of capital is not in line, then investors are going to take a view on your costs and decide whether or not they are going to give you a lower cost of funding. In the steady state there comes a point when everyone is chasing longer-term, more stable and cheaper financing, which will be predominantly in the offshore market.

PATRICK LIU, UBS: Apart from the cost of funding issues, there are other reasons for issuers to consider offshore funding. Chinese property developers acquiring property in other countries, for development purposes or for investment, require offshore funding to finance growth. Also, although it is not yet prevalent, I would expect some major M&A activity in the sector. Notwithstanding the cycles of recent years, there has been no significant consolidation in the sector.

IFR: Will the overseas markets have a role in domestic M&A?

PATRICK LIU, UBS: It could happen in two ways – either with Chinese companies buying overseas or when there is consolidation among companies that have been listed overseas. Typically, these types of acquisitions will need to be financed offshore. There is also general refinancing. You can see that clients are reducing their positions in trust loans, and looking for other options in the US dollar or offshore renminbi bond market or other local currency options. In light of this, the trend for Chinese developers to consider offshore fundraising can be expected to continue.

KALAI PILLAY, FITCH RATINGS: It all sounds exciting, but I think there is a segment of the market that will have problems, and that is the smaller guys who are coming out now. This market is very, very competitive, land prices are still very high, property prices are not picking up and sales are difficult whichever way you look at it. The recent IPO companies, for those to try to raise funds at this time is going to be very tough. For that segment I think it’s going to be a very challenging to raise bonds. And correlated to that, you’re not going to see that many more names being added to the club of 40–50 names that issue offshore. The boat has sailed, the train has left the platform, and it’s going to be very hard for a new company to come to IPO, do your offshore bond, get the land, do your first round of property development and go back to market with that scale. That is going to get very much harder now.

IFR: We’ve seen some industrial names try and fail to get deals done in US dollars this year.

KALAI PILLAY, FITCH RATINGS: Yes, but even in property some haven’t managed to price their bond offerings. Their stories are not very different from other companies two or three years ago, it’s just that at this point it’s going to be very difficult for them.

IFR: Albert, you’re smiling at that.

ALBERT YAU, CIFI: It’s always difficult for a new credit to come out to the market, but over time I think investors are looking at both the track record and the funding strategy. The strategy is very, very important.

IFR: So in your experience, you listed late in 2012 and then sold bonds in 2013 at a 12.25% coupon.

ALBERT YAU, CIFI: We then did a tap in the third quarter last year and the yield went down a little bit to 11%, and then we did a new issue early this year at below 9%. It is a very difficult process, but once our credit has been accepted by the bond market then it gets easier. If you look at onshore versus offshore, the loan growth onshore for this year is basically stagnant. So for companies like ours that are pursuing growth, we are relying more on the offshore market for new financing.

IFR: So 12.25% in the end was a good price to pay to get that access?

ALBERT YAU, CIFI: When you come out for the first time you definitely need to offer more to investors, but over time any corporate in our sector needs to have a clear objective of pushing down its funding cost. You can’t do double-digit funding costs every time you come out when the profit margin in our business is normalising.

WALLACE LAM, HSBC: Going back to one of the first comments I made, in this sector many issuers need to pay some premium to come to the market for the first time. CIFI is a very good example of the market dynamics. The yield compression from the first one until now has been very substantial. So for investors who do their homework and are able to identify the key winners and the industry champions, it will be very rewarding for them.

IFR: So if Albert was in the market tomorrow, what would they be paying?

ALBERT YAU, CIFI: I think it should be lower than last time, when we issued in January.

KALAI PILLAY, FITCH RATINGS: And now you have a BB– rating!

WALLACE LAM, HSBC: It shows that when the whole sector is under pressure, you can still find companies that have experienced growing sales and might even get upgraded. That’s encouraging for investors.

ALBERT YAU, CIFI: I have a very interesting observation for this year when you look at the bond market versus the equity market for securities. This year is definitely a year of correction for our sector, but what I’ve seen is a lot of funds were very smart at seeing the value in the low months in April/May – Ben is one of them, but he is not the only one. A lot of other investors, including those sitting in London, are very close to the market. They know what’s happening, and when I look at the reaction in the bond market it is very rational and a lot more sophisticated than we thought, and to a certain extent it could be even more sophisticated than the equity investors in our sector. We see that the equity market fluctuation in our sector is just too wide.

MICHAEL LEE, GUANGZHOU R&F: Yes, it’s definitely much more short term. And, as Albert pointed out, when you went to London or New York for investor meetings two years ago, the first thing they would quote is what they read in the newspapers. Now when you go to the meetings they’ll talk to you about your company and other peers, and are going into the micro of your strategy. There’s no longer as many quotes from the newspapers. They’re making trips down and taking more interest in you as a name rather than you as a sector. That comes back to the whole theme of how it’s no longer a blanket approach to the sector, and that’s why the credits can be differentiated by investor meetings, dialogue, strategy, and how they fit each individual investor.

IFR: So what can we do to bring down funding costs? Patrick mentioned the keepwell agreements, SAFE guarantees and other credit enhancements. From an investor’s point of view, are they worth the additional complexity?

BEN YUEN, BOCHK: The keepwell is a new structure that looks better than what we’ve had in the past. But on the other side, the keepwell structure has not been tested in a default situation, and bankruptcy law in China is a big question. We have to ask ourselves about that.

To the question of whether the funding spree can keep going, as an investor we would like to see issuers have more funding channels. I’m very happy to see more issuers come to the offshore bond market or the Dim Sum bond market, but if I’m seeing the gearing ratios increasing that is much more of a concern from an investor’s point of view. If the equity market is good, we should see more issuers coming out with rights issues for the other side of their long-term capital structure.

It’s the same situation it the issuer can issue more bonds onshore because of regulatory changes that increase the demand for onshore corporate bonds. We can see RQFII fund flows increasing quite substantially, and investors are going into policy bank bonds and government bonds as well. I can foresee this demand will keep increasing, and that this type of investor will gradually expand into the corporate bond area as well. So, as an investor, if we can see more funding channels for the issuer then we feel more comfortable. At the end of the day, their funding costs will be gradually reduced as well.

WALLACE LAM, HSBC: I’d like to go back to your point, Ben, when you mentioned about the keepwell not being tested. Just to make one comment – since we introduced the structure back in 2012 we didn’t stop there. First of all, when the regulation allowed the parent company in China to provide renminbi-denominated facilities to its offshore subsidiary, we’ve also put that in. Wanda’s keepwell was the first one to include a renminbi-denominated standby facility, which became permissible under the new SAFE rule. For Gemdale, for instance, there was actually a change of control event last year. As a result, investors were putting the bonds back to the company. What the company did was they actually channelled money from onshore to offshore by means of the credit facility from the parent to pay off the bonds. It was not reported as it was seen as business as usual. To me, it was a very good test case where the keepwell worked and investors got their money back.

MICHAEL LEE, GUANGZHOU R&F: We’re obviously one of the biggest beneficiaries of the keepwell structure. Before then, we were only reliant on the ability to issue off a holdco guarantee, and even then the market didn’t know how to price such a guaranteed structured bond appropriately – it was still being priced at double digits. Since then, people have appreciated that a guarantee is a stronger credit, but the keepwell innovation has allowed us to revisit the market as an option.

With the Gemdale keepwell, people obviously bought into the company, the background and its status, but initially it was a struggle for investors to buy the concept, because the keepwell basically meant that you had hurdles to jump or hoops to go through in order to satisfy the keepwell commitment. We argued our keepwell was different in the sense that we already have assets in there. It’s not a guarantee, but there are safeguards behind the keepwell.

Every keepwell may not always be the same in application. Some may be more of a perception, that the parent company will step in if anything happens, but there are situations (like us) where if anything does happen, we do have assets that we can use to enforce the keepwell. I think it was initially very hard for investors to grasp that it’s not a bank guarantee, it’s sort of an “I support you” from the parent in a contractual form. But over time investors realised that it’s a credit enhancement tool that signals the parent’s strategic support for the issuing offshore subsidiary, which wasn’t readily accepted in the past. Over time, investors have appreciated that, and now people don’t even ask questions about the keepwell, they accept that as a structure for this kind of company.\

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.