IFR ASIA: Welcome everyone. I’m going to ask KathArine to frame this discussion for us at the start. Why is financing sustainable infrastructure so relevant to this part of the world?

KATHARINE TAPLEY, ANZ: When you think about the already existing effects of climate change, particularly in the Pacific region, then the need to fund long-term infrastructure is vital. There really is no choice in my view as to what needs to happen, and I think the sustainable finance markets have a very significant role to play.

We’re seeing significant appetite from investors for so-called green assets, but there is a broader concept around sustainability and sustainable development. There is an absolute wall of capital there waiting to be deployed into infrastructure that helps economies – such as Fiji, for example – and the broader region sustain their economies for the long term.

IFR ASIA: Thank you. Nishimura-san, what’s the role of the local capital markets?

KYOSHI NISHIMURA, CGIF: So today we are talking about financing for infrastructure projects, especially sustainable infrastructure projects. Sustainable infrastructure projects are projects which are sustainable in terms of their climate or environment or social impact. How these assets are financed is also important to their sustainability. Infrastructure projects need long-term funds because of their long-term payback period. Many projects rely on revenues that come only after they are completed. These revenues are generated in the local currency, so if you borrow in foreign currency that creates a mismatch problem for the project. So if an infrastructure project is really going to be sustainable, it should really be financed by long-term local currency funds.

The good news is, if you look at emerging Asia – and it may be different from elsewhere – most infrastructure projects are already financed by the domestic financial system in their local currency. According to World Bank and ADB data 70%–80% of PPP-type projects are financed domestically in the local currency. That is good news. It is better than before the Asian financial crisis, when many projects were borrowing short-term, foreign currency loans.

The problem here is that when we talk about finance in the domestic financial system, it still means in most Asian countries we are talking about the banking system. The financiers are local banks, which may still create a problem in asset/liability mismatches in the banking system, because banks basically rely on short-term deposits to finance these long-term assets.

So that is the reason why the ASEAN+3 governments are trying to develop a bond market to create a more balanced domestic financial system. Long-term infrastructure projects – especially sustainable infrastructure projects – should be really financed with long-term, local currency funds in the bond market.

At this moment some infrastructure projects in emerging Asia are already financed through the bond market, but they’re usually from companies issuing general corporate bonds. We aim to promote more project bonds, which are issued at the individual project level on a project finance basis, just like a project finance loan from the banks. You can issue project bonds which match the cashflows from a project at a longer tenor than a general corporate bond.

In emerging Asia, you don’t really see many project bonds. Malaysia is the only country in Asia that has successfully developed a project bond market, where most projects – even greenfield projects – are funded through project bonds or Islamic sukuk.

“There is an absolute wall of capital there waiting to be deployed into infrastructure that helps economies – such as Fiji, for example – and the broader region sustain their economies for the long term.”

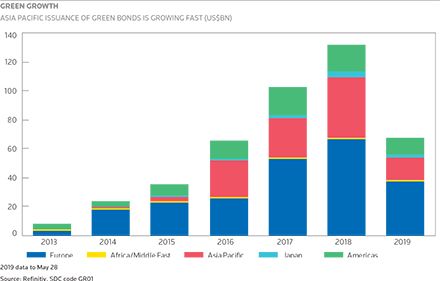

There is also good news about green bonds. As Steve mentioned, growth last year in emerging Asia was 35%. Actually it’s the fastest growing green bond market in the world and has become already the global leader in the green bond market.

IFR ASIA: Lots to talk about there! Clive, where does structured finance fit in this picture?

CLIVE KERNER, CLIFFORD CAPITAL: I think there is an increasing role for structured finance in terms of facilitating the transfer of project finance loans from bank balance sheets into the capital markets and thereby crowding in institutional debt. That’s one of the principal functions that we play in Clifford Capital, and the rationale is that we’re helping banks to recycle their balance sheets, which is increasingly important because of tighter capital and liquidity constraints due to increased regulation under Basel III.

At the moment in Asia, as most people in the room know, there’s very little institutional debt invested in the infrastructure space. Therefore there really is a need to crowd in that asset class, particularly given the huge demand for infrastructure in the region that will require private sector financing.

Nishimura-san has already touched on capital market issuance for single assets. I think there’s certainly a role for that, and there’s more being done, but one of the challenges is that you need to achieve a benchmark issuance size in order to create liquidity and investor demand. Institutional investors are typically also looking for investment-grade ratings, which in the context of Asia – in particular in some of the more emerging markets – is quite difficult to achieve.

So that’s where securitisation can play a role. The transaction that we concluded last year was Asia’s first project finance loan securitisation. We managed to come to market with a portfolio of 37 loans, of which quite a number were related to projects in deep emerging markets that otherwise would not have been able to achieve capital markets treatment.

Notwithstanding that, because of the diversification in the portfolio, the impact of the subordination in the capital structure and the fact that all the underlying projects were operational or close to operational (and therefore de-risked), it was possible to structure the transaction so that the senior notes offered to investors – which represented 70% of the capital stack – were rated AAA by Moody’s. Therefore what we’re doing is offering institutional investors high-quality paper and at the same time giving them access to a high quality diversified Asian infrastructure credit portfolio. I think this is one of the key benefits of the securitisation approach.

IFR ASIA: Katharine, we mentioned a little bit about green bonds and green finance. Can you give us a little bit more of an update on recent developments there?

KATHARINE TAPLEY, ANZ: Yes. Our experience is that every time we go out on a roadshow – whether it’s for ANZ or for a client in New Zealand, Australia, or anywhere in Asia – there are always more investors wanting access to green, social or sustainability bonds. We’re certainly seeing an increase in appetite, and a change in the way that these portfolios are being made up. There is a significant slant towards sustainability and sustainable development, and within that towards green assets in particular.

For me that’s a real trend and I think that’s only going to go one way. With the growth of the millennial generation, as they come into a significant part of global wealth over the next 10 or so years, that will continue to be a very strong force as investors become very picky about where they want their money to go.

The other trend and interesting development that we see is the broadening of asset classes to which these transactions can be applied. Initially the green bond market was dominated by renewable energy – solar farms, wind farms, for example. We’ve seen a broadening of that into transportation, in particular, and sustainable land use. There’s a lot of potential in the agriculture sector. Energy efficiency is also a theme. Significant amounts of investment dollars are being spent on upgrading lighting, and demand management for power, solar installations, etc. One very recent transaction we did in Australia was with Woolworths, which is a well-known supermarket brand in Australia and New Zealand. Over a relatively sustained period of three or four years, Woolworths has been consistently investing in upgrading the efficiency of its supermarket properties. We were able to construct a baseline with the Climate Bonds Initiative for measuring the emissions intensity of their properties and constructed a green bond off the back of that. It’s a really significant transaction because it shows that the green capital markets are available to companies outside the renewable energy sectors. That’s really exciting.

IFR ASIA: So does that mean that anybody can issue a green bond?

KATHARINE TAPLEY, ANZ: It’s not quite that simple. Under the Green Bond Principles, you do need a green or definable asset base for a start, so that can present challenges. For us – as an arranger and certainly also as an issuer – it’s really important that there is an agenda and a strategy around sustainability. That’s really important when we’re choosing our partners with whom we do these transactions.

IFR ASIA: Nishimura-san, I understand green bonds are a growing focus for you at CGIF. Is that right?

KYOSHI NISHIMURA, CGIF: Yes. We supported the first green bond in Philippine pesos, together with the ADB, three years ago, and we have a number of potential green bonds in the pipeline. Actually this is really my favourite subject. To see where we are going, we need to really understand the context of green bonds in developing and more developed countries.

Green bonds started in the developed markets in Europe and North America and have grown quite significantly, and their growth was market-driven, because there are dedicated investors for green or socially responsible bonds..

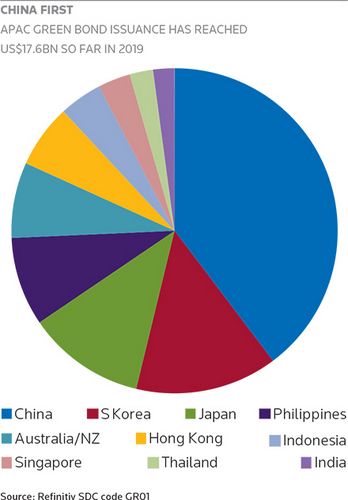

However, if you look at the development of green bonds in emerging Asia, the situation is different. The typical case is China. China now has become the second largest green bond market globally within a few years, but it was not created by a market-driven or bottom-up approach. Basically domestic bond investors don’t really differentiate between green bonds or normal conventional bonds. It was policy-driven, because regulators introduced guidelines and encouraged issuers to sell green bonds.

Green bonds have also grown quite substantially in other Asian emerging markets, like the ASEAN countries. At this moment six of the 10 ASEAN member countries have active domestic bond markets, and you see green bond issuance in all six. Having said that, most of these markets – probably Singapore is a little bit different – do not have a strong domestic investor base for green bonds. It’s really policy-driven. ASEAN countries have introduced a regional green bond standard and some incentive schemes to try to encourage green bond issuers.

“In emerging Asia, you don’t really see many project bonds. Malaysia is the only country in Asia that has successfully developed a project bond market, where most projects are funded through project bonds or Islamic sukuk.”

Multilateral development banks are also supporting the creation of the green bond market. Some green bonds have been bought solely by multilateral development banks, rather than local investors.

So the challenge for developing countries is, if you want to really grow the green bond market to a sustainable level, you need to create a domestic bond investor base which is really dedicated to investing in green bonds.

That means first of all it’s very important to raise awareness of why green bonds are important, and the impact of ESG on investment decisions. There may be some regulatory ways to incentivise investors to invest in the green bond. Otherwise it’s going to continue to be policy-driven, so it may not be really sustainable in the long term.

IFR ASIA: If there’s no dedicated investor base, what’s the advantage to an issuer from making your financing green?

KATHARINE TAPLEY, ANZ: Typically with these transactions, we tend to see more investors coming in and in much greater volume. So you are tapping into brand new money, as well as new funds within existing investors that you didn’t previously have access to. That diversity and granularity has to be an advantage to a borrower, and that’s a trend that we’re seeing right across our region.

The other piece that often gets underestimated when a borrower goes into a transaction is the strengthening of the relationship with their investor base. Typically fixed income investors haven’t had a great deal of dialogue with the companies that they’re funding. There tends to be minimal interaction between transactions.

The key difference with the green bond market is that a well-structured green or sustainability bond comes with a whole lot of transparency and reporting. That’s an advantage both to the issuer and the investor, because they get this dialogue that wasn’t otherwise there.

The fixed income investor base has an opportunity to help steward this change. I think that’s incredibly powerful in the bigger picture around mobilising large amounts of capital in order to ensure that we have a sustainably developed world.

IFR ASIA: Clive, you are a regular issuer in the capital markets. Have you considered making any of these deals green?

CLIVE KERNER, CLIFFORD CAPITAL: We have and we’d love to do more, but I think when you’re talking about securitisation you need to focus on what is already available out there in the market. One of the key criteria for successfully executing our securitisation is that institutional investors don’t like greenfield risk. You need to work with brownfield projects or assets that are close to completion. Over time, certainly there’ll be more green assets coming through as the stock of completed projects increases.

IFR ASIA: Can you tell us a bit about the demand that you see from investors?

CLIVE KERNER, CLIFFORD CAPITAL: The view we formed – and it’s looking at the other end of the spectrum in the power sector – is that we don’t think we could include any coal assets in a future securitisation. The market is increasingly gravitating away from coal and towards renewables.

So as we structure these transactions we need to be very conscious about what institutional investors are looking for. This shift in the negative attitude to coal on the investor side has continued since we did the first deal last year, so I think that will also help to drive more sustainable and green projects coming to the market.

IFR ASIA: Was it difficult to find the assets to put into that securitisation? We hear a lot about a lack of bankable projects, but you managed to find 37 of them to put into a deal.

CLIVE KERNER, CLIFFORD CAPITAL: We did. Individual banks have tried to do this for a long time and they’ve struggled, because one of the challenges they find is that they don’t have enough loan diversification on their own balance sheets. We’re not a bank and, because we have support from the Singapore government, our project was heavily sponsored by the MAS. I think that helped us to get access to banks who were willing to open their books and have a discussion with us around what types of assets they were willing to transfer. I think that was a key success factor. The banks we ended up dealing with were our three shareholder banks – Standard Chartered, SMBC and DBS – and also two others, HSBC and MUFG. I think the banks also view us as a neutral player rather than necessarily being a competitor.

In terms of identifying the assets we looked at just over 50. We set out some fairly clear criteria with the banks in terms of the assets we thought that would work for the structure. We ended up with 37, so a few fell along the wayside but that was a fairly okay process. However, it was quite time-consuming, in the sense that we needed to undertake a detailed credit evaluation on each of the assets. Also Moody’s produced what they call a Credit Estimate, which is like an informal rating on each of the assets. So the process took a number of months. The bigger challenge was selling the CLO structure to investors, because it was the first of its type. That took about six months but we eventually got there with a good outcome.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@refinitiv.com