ARUNDHATI BHATTACHARYA, SBI: Of course I don’t agree that we don’t have a sound banking system! If you look at India, one of the reasons for the large amount of NPLs was the fact that we had a large amount of infrastructure built in the country at a particular period of time. And all of the heavy lifting was done by the commercial banks. They had 10-year money, and as a result all of this funding was done on a 10-year basis, with the expectation that repayments would happen in an average time of 7½ years. Now you cannot have 30-year assets being paid back in 7½ years. You’re looking at disaster if you do that, and that’s exactly what has happened.

When repayments are crunched into a short period of time, you are front-loading all of your repayments, which means that the infrastructure has to not just come in on time, but it has to ramp up its usage quickly enough to produce that kind of cash flow. India was experimenting with the PPP model and a lot of policy initiatives from the government didn’t come through, and as a result the projects didn’t come in on time. Second, if you have very high user fees, you will not get the kind of usage that you would like from that infrastructure. So initially you need to keep user fees down, and that can only happen if repayments happen over a long period of time. You’ve got a large amount of infrastructure built with short-term funds, and therefore you are seeing a lot of stress.

The regulators have already looked at how to release that stress. They have allowed banks to raise infrastructure bonds, which are long papers of up to 15 years. They have also announced that financing structures should be up to 80% of the life of the asset, instead of scrunched in to 10 years. Both of these should take care of things going forward, but what about things that are already stuck? The asset reconstruction companies (ARCs) were getting quite active, until the regulator revised some requirements relating to being able to pay 15% cash upfront and changed the way they could charge a management fee.

The basic roadblock in India is that the resolution of an asset through the judicial system takes a lot of time. Now the government in its latest budget speech has made two provisions, which are important and will make this easier. The first is to come up with a bankruptcy law, and the second is they will have a separate set of commercial courts. This will enable commercial arbitration to be heard by a different set of people, who will have the expertise but will not be bogged down by the backlog in the regular judicial system. Both of these things will help with the resolution of assets, which at present is pretty slow. Even in the public sector we are now resolving assets faster. For instance, last quarter we had a mega auction, where we managed to auction off 93 properties in the space of three or four hours on a very open, very visible online platform.

As the banks get better at resolving their bad assets, as the legal and policy framework kicks in, as the ARCs see better returns, we will also have more interest from ARCs looking to come in – because in India there is inflation. An asset that today may be stressed, but if you look at the replacement cost of that asset it may be 200–300 times the amount that was initially spent. We don’t have a surfeit of infrastructure, so all these stressed assets have a lot of intrinsic value, and the realisation of those should fetch us good money. There is a lot of interest from foreign investors, but the enabling legislative framework will help. We firmly believe this is something we can work through.

TOM BYRNE, MOODY’S: I just wanted to make a clarification: I didn’t mean to say India’s banking system was not sound. It’s not as sound as others, and that’s reflected in our bank financial strength ratings which are relatively low compared with Indonesia or the Philippines.

LAKSHMI VENKATACHALAM, ADB: There are lessons to be learned here that are also salutary for the Indian banking system. I dare say the first generation of PPP projects weren’t subject to proper risk-based pricing, and the consequences are there to be seen. We know that Basel III will certainly have its impact in this area, but we do need very strong underwriting skills to be able to price risk correctly. If that is done, then the segue into the capital markets becomes much smoother.

ARUNDHATI BHATTACHARYA, SBI: The capital markets also need to develop. The entire heavy lifting can’t be done by commercial banks alone. It is very important for the bond market to be in place if you’re going to see proper infrastructure financing structures.

LAKSHMI VENKATACHALAM, ADB: When you look moving this generation of infrastructure assets off the banks, you need much more flexibility in terms of pricing credit enhancement products like partial risk guarantees. It has to be risk-based, and you need regulatory support to enable that.

QUESTION: I have two questions. First, Asia is dominated by SMEs, and banks often require collateral, so it is very difficult for SMEs to borrow money. What is the role of the capital markets in providing money for SMEs? Secondly, in order to develop a capital market I think commissions and fees are very important. Performance for investors is important, so performance-based fees would create a much better market than fixed commissions, otherwise many investors will run away. I’d like to ask about the structure of fees.

IFR ASIA: Alexi, would you like to take the first question there on SME funding?

ALEXI CHAN, HSBC: This goes to the heart of what we’ve been debating today on the panel, which is that in many areas of the real economy the potential role that banks and capital markets can play may be complementary. We have seen, for example, the development of a high-yield bond market to service companies in the Asian region. This has been denominated at times in US dollars but also in certain Asian currencies, and this can offer an opportunity for companies with a risk profile that may not suit all banks to fund in the capital markets. Sometimes deals come with security, sometimes without, and they respond to the different risk appetites that exist in the fund management community when compared to banks. Clearly, that’s not going to be a solution for all SMEs, and there will be times when bank finance will be important as well. So I think this comes to the heart of it. The development of an in-depth credit culture is one of the important features that we, as a private sector participant, believe can lead to more liquidity in Asia’s capital markets, and more relevance in terms of the sorts of assets that can be financed.

RUFAT ASLANLI, AZERBAIJAN: I would like to share our experience. We have a listing and advisory project, and together with Baku stock exchange we are working with SMEs to bring them to the capital markets to raise funding. We have found that it is very difficult for SMEs to meet all the requirements for capital market issuance. It may be a matter of time, but in our practice it’s very difficult to bring SMEs to the capital markets.

IFR ASIA: The second question was on fees and commissions linked to investor performance, I think. Arundhati, perhaps you can comment there?

ARUNDHATI BHATTACHARYA, SBI: Well it’s a good concept, but I don’t know whether this is something that is going to happen in a hurry. Our regulator has been trying a number of things to ensure that investors are not impacted – in fact at one point of time they had thought of a safety net for retail investors, where the merchant bankers would be responsible for any depreciation after listing. Obviously that kind of regulation couldn’t come in, because after all this is equity, and equity investors should know the risk they are running. In respect to bonds, I don’t know whether some differential commission could be done, and I don’t think there’s any consideration at this point. The main thing that will protect investors is a sufficiently transparent and open market. The depth of the market matters. The regulations around it matters. Resolving disputes quickly matters. Very stringent action against someone trying to manipulate it matters. I think it’s the strength of the market that is in the best interest of the investor, rather than having things that tweak commissions or put in checks and balances in artificial ways.

QUESTION: Recently we are seeing the dollar strengthening against many emerging market currencies – India is no exception. During recent years we have also seen a gradual depreciation in the rupee. I wonder if this has had any adverse impact on the ability of the banks to enter into future foreign exchange transactions?

ARUNDHATI BHATTACHARYA, SBI: There is no limited appetite. If you look at the Indian market the dollar/rupee is pretty liquid up to three years. It is only beyond that the market gets a little shallow. We are quite comfortable in those matters. In fact the Indian currency has stood out from the rest of the emerging markets in its strength against the dollar, much to the disappointment of our exporters. Those companies continue to want the currency to depreciate faster, and both the government and the regulators have shown a lot of resolve in ensuring that even if the rupee weakens it does so at a measured pace.

When the first talk of an end to QE happened, the so-called taper tantrum, India along with the rest of the ‘Fragile Five’ had a pretty large hit and a large depreciation. But we have come back from that, and the way that it was done was on the fiscal front. The government immediately swung into action. India has two major imports: one is of course energy, the other is gold. And gold is obviously a non-essential item, so the government clamped down very heavily on gold imports. That brought in a lot of duty, and also put in checks and balances on who could import. As a result gold imports fell sharply, thereby cutting the current account deficit. Since then the government has been further helped by the fall in oil prices, so the currency account deficit now is very manageable. That was on the one front.

On the other side, the Reserve Bank opened a special window for the non-resident Indians across the world to put in money at a slightly higher interest rate. I love saying this when the rating agencies are around: no matter what they may say about India, for NRIs India will always be Triple A. The moment you give them a little bit more interest they all come in, and in something like 30 days India was able to get inflows of about US$30bn. That was the kind of strength that was on show. Therefore, we were able to restrict the fall in the Indian currency. We don’t want it to be too strong, because that doesn’t really reflect the true value of the rupee, so there should be some depreciation. Over the longer term, depreciation has been at 2.5%–3%. I think it’s quite well managed.

ALEXI CHAN, HSBC: If I can just add from a regional perspective, the dollar strength we’ve seen in the past few months has affected the region’s capital markets. I think the question that’s pertinent with respect to this debate is whether the growth we’ve seen in dollar bond issuance from Asia has to some extent reflected this trend of the strong dollar. Some of the steps we’ve discussed in strengthening the local bond markets become even more important when we see these very strong movements in big global currencies. The question is whether that development has been more cyclical – reflecting these kinds of macro factors – or structural. Clearly the structural agenda is the critical one, and I think these sorts of movements demonstrate that the underlying strength of Asia’s local currency bond markets will be as important as the overall environment.

IFR ASIA: What happens next when the US starts raising rates is on everybody’s mind. Tom, is Asia as strong today as it needs to be?

TOM BYRNE, MOODY’S: The way we look at it, Asia Pacific has adequate strength to withstand the US Fed’s liftoff, assuming it happens at some time in the near future. One reason why we’re actually positive on India is that the vulnerability to adverse capital flows has been reduced greatly, partly through the Asian financial crisis and the global financial crisis. We see this through banks’ external financing, and also governments’ external financing. Although India has relatively large debt, the foreign currency share of the debt is fairly low at 6%–7%, whereas in Indonesia it’s more like 40%. That’s a big vulnerability for a country like Indonesia.

More fundamentally, looking beyond the headline statistics, what’s important going forward is that the countries with large fiscal deficits find a way to work that down. That would help give markets more confidence in placing more money in a country, which leads to tighter government yields and brings down funding costs in the whole local bond market. Certainly, you can look at India versus Indonesia to see which country has the biggest success in fiscal reform and reducing government deficits, bringing down borrowing requirements over time.

IFR ASIA: We have two of the few Asian entities that have issued Green bonds on our panel today, and I wonder if there is an opportunity for this part of the world. David, you launched your first one this year, if I remember correctly.

DAVID RASQUINHA, INDIA EXIM: Yes, we did the first ever US dollar Green bond out of India, and that is just the third Green bond out of Asia. So it does show that the market there has a way to go, but if I give you some numbers, last year in 2014 the total Green bond issuance volume was about US$35bn–$36bn. That’s not very much, but the projections for 2015 are as much as US$100bn. Even that may not be very much in absolute terms but the growth is quite phenomenal for a segment of the market in the space of a single calendar year.

Our experience was actually quite positive. We had tapped the Reg S market in February for a half a billion, and the market does not normally look favourably on repeat trips too close together, so we were looking at US$200m–$250m as a test of a new market. The response was so positive that we ended up with an oversubscription of 3.2 times, and upsized the issue to US$500m. The pricing was almost exactly the same as the regular Reg S format. We had expected that we might have to pay a slight premium to access a new market and diversify investors, but we priced both times within our secondaries and the Green bond came flat to the earlier issue.

We found this was a very interesting exercise. We had to do a lot of investor updates and due diligence calls. You can say there are various shades of green, if I can use that term, and the Green funds themselves were very interested in going into the micro level in terms of the use of the funds, and how we could assure them that the funds would be used only for those projects. But we also found there was a lighter shade of green, where fund investors with a regular portfolio also have a subset of funds with a green angle. They were a little less insistent, but at the same time wanted the assurance as to the use of funds. It was a very interesting experience, and given the level of demand I expect we will see a lot more out of India and out of Asia.

IFR ASIA: Did you find much support from the Asian investor base?

DAVID RASQUINHA, INDIA EXIM: Yes indeed. There was a significant contribution out of Asia – I think 30%-35%. The Middle East was quite strong, which was not something we’d expected. Europe was a little less strong, and the conclusion we drew was that perhaps we need to do a little more work in conveying exactly what we are doing to prospective European investors, who tend to be a little more demanding on the green side, and perhaps provide some additional reassurance in that area.

IFR ASIA: What does the panel think about moving more infrastructure into the capital markets? What’s holding that process back?

LAKSHMI VENKATACHALAM, ADB: We’ve faced some challenges in developing the project bond markets. We believe that this is the way to go, but we also know that it requires a huge push factor, and we believe this can really come from innovative credit-enhancement schemes, such as partial credit guarantees and other risk-sharing arrangements. Accordingly, we got off the ground with support to IIFCL a couple of years ago, where we agreed to participate in their credit-enhancement initiative. Unfortunately, it took quite a while to really get project sponsors to bite into this. And there were also issues in terms of the enabling environment for pushing these assets into the bond markets: the interest rates at that time were not really conducive, and the price differential was not working in favour of the project sponsors.

It brings me back again and again to the need for very concerted action in developing a product like this. You need investor interest, but you also need the regulatory push factors. It has to be expensive for banks to hold these assets, and you’ve got to incentivise institutional investors to put away part of their investment capital into products like project bonds. We also need to develop the infrastructure for creating the necessary exit and entry points for these bonds.

Awareness is also a huge barrier, because people still don’t understand the dynamics of this. Look at the way in which the developed markets are promoting credit enhancement. I can recall the experiment that’s going on currently in Europe, with the EU providing budgetary and guarantee support and the EIB being able to ride on this to provide partial credit guarantees. We need a lot of players to really dig in.

As a multilateral bank, we are really ready to experiment and provide the signature support – the catalytic support – to bring this product in. In fact, we think it would be useful not only for brownfield projects, where you’ve dealt with the construction risk and there is a strong case for putting these bonds into the market, but also for capital restructuring, to balance out the capital structures of companies who might have put in a lot of equity in the first place. We are looking at structures like this in the Philippines as well, where there is investor interest. We can play the role of the connector in bringing these actors together, and we are hopeful we will be successful as we go on.

IFR ASIA: Is there international appetite for these kinds of structures?

ALEXI CHAN, HSBC: Absolutely, there is significant appetite from certain types of international investors looking to fund Asia’s infrastructure requirements on a project basis. Globally, we have a developed insurance company and pension fund industry which is well suited to taking on some of the longer tenors that are required to fund infrastructure and projects in the region. The challenge really is to bring together – as others have mentioned – the different types of stakeholders involved in infrastructure financing, and to share the risk between banks and capital markets in a way that is suited to each party’s requirements. The banks may be better able to fund the greenfield phase of selected projects, where the cash flows are less certain, and the capital markets may come in for the longer term pieces. Bringing those together efficiently is the key challenge.

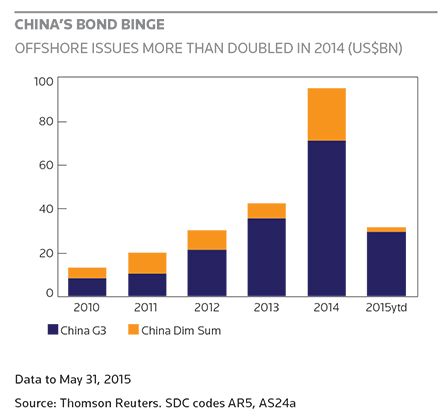

IFR ASIA: We’ve talked a bit about the model for an offshore local currency market. How much of a guide is the offshore renminbi, or Dim Sum, market?

ALEXI CHAN, HSBC: The RMB’s importance in the global capital markets is going to increase tremendously. It’s already becoming much more significant in trade flows, and we are seeing greater interest from investors around the world. Without full capital account convertibility we have seen the development of an offshore RMB bond market, where the securities are genuinely denominated in RMB but are distinct from the onshore market. The appeal that has held for Chinese entities has been an ability to fund in their own currency, in RMB, but using a format in the bond markets that is very similar – if not identical – to a Eurobond in terms of governing laws, clearing systems and disclosure.

I would stress that the market is distinct to the onshore RMB bond market. While the Dim Sum market clearly offers an interesting model as to how an Asian currency can very quickly become relevant to a wide range of issuers – both those using the currency as their own and also international market participants – the larger challenge will be around the onshore market. We are certainly seeing greater interest and a greater willingness from market participants to gradually open up the onshore market. Bringing in the factors we’ve talked about in terms of international best practice, aligning the local markets with practices we see elsewhere in the region and globally, is another big exercise that we’ll be looking at alongside the offshore market.

IFR ASIA: Do you think the onshore market will kill off the Dim Sum arena, if full liberalisation does occur? Wouldn’t people just go directly to the onshore investor base?

ALEXI CHAN, HSBC: I think we will see interest in the offshore market for some time to come, certainly in the run up to full liberalisation. Beyond that, we are going to see benefits for investors, in that holding an Asian currency asset in offshore format will continue to be very attractive to the international market. Clearly, we will see greater convergence of the two markets – in terms of tenors, terms available and market practice – as we move towards full capital account liberalisation in China, but we think the offshore market will remain relevant for some time to come.

IFR ASIA: Tom, I wonder if you might have a view on how long it might take for China to fully open up?

TOM BYRNE, MOODY’S: Well it won’t happen this year, despite some statements by (People’s Bank of China Governor) Zhou Xiaochuan. We think it will happen at a gradual pace. The Chinese authorities are continuing to experiment: the link between the Hong Kong and Shanghai exchanges is another example, and they may build on the QFII schemes. But the RMB is still largely used for trade settlement. International transactions are still only about 1%–2%, whereas US dollar transactions are way more than 40% globally. There’s still a long way to go for this market. The Chinese have to get the sequencing right, and make sure the financial system can withstand a lot more scrutiny.

QUESTION: Thank you very much for your insightful discussion. I have a question about cross-border transactions. Could you share you idea how we can increase the cross-border bond transactions in Asia please?

LAKSHMI VENKATACHALAM, ADB: Part of it would be through infrastructure development and the harmonisation of various regulations, so that cross-border issuance becomes almost a seamless activity. But, most importantly, the demand pool will really grow as investors raise capital to fuel their investment plans, so I dare say the push factor will come from investors looking for projects where they can channel their investments. Policy dialogues will have to continue with governments to ease the enabling environment, and we also need more intermediation from agencies who can delve deeper into individual segments, understand investor interest, tailor products, understand sector demand and so on. And then of course we can ease the whole issue of disclosure and other requirements, to simplify procedures and so on. There’s a lot of work to be done in that space.

Remember, when we’re talking about Asia we’re talking about countries at varying levels of development. Right now if you were to ask me, I would say that ASEAN+3 still presents the most promising space, because ASEAN is moving towards becoming a single economic community by the end of this year. They have the right sentiment and the right, compelling argument to really push forward on this agenda.

IFR ASIA: Ladies and gentlemen, please do join me in thanking our distinguished panellists, and thank you for your attention.

To view all special report articles please click here and to see the digital version of this report please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com .