Green bonds face a tough sell in Asia, where climate concerns have long taken a back seat to development. That mindset is changing, but the right incentives will be key to creating a vibrant local market.

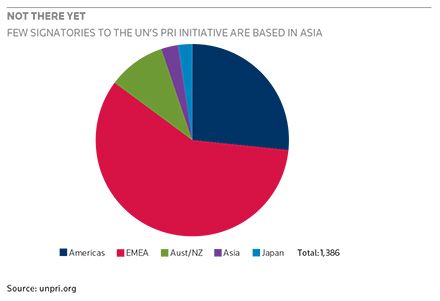

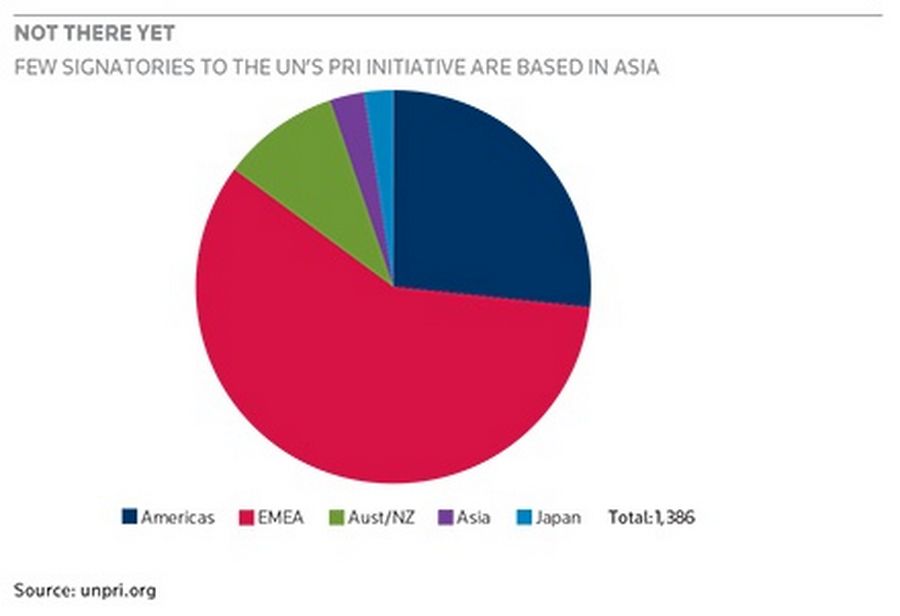

Searching for an Asian fixed-income fund that targets environmentally sustainable investments is a frustrating exercise. Outside of Australia and Japan, only 39 of the 1,386 signatories to the United Nations Principles for Responsible Investment – which cover environmental, social and corporate governance issues – are based in Asia, and the big regional investors are conspicuously absent. Narrow the field further to fixed income, and it’s no surprise that the Green bond phenomenon has been slow to take off in Asia.

That, however, may be about to change. After a decidedly lukewarm start, recent developments are raising hopes that the region’s capital markets can be part of the solution to the world’s climate challenge.

The Climate Bonds Initiative, a non-governmental organisation that works as an advocate for Green bonds, expects China to be the world’s largest Green bond market by 2018 – even though the first such deal has yet to appear. India has already seen two Green issues, and bankers expect more to follow as the government pushes banks to help meet its target of generating 100 gigawatts of additional power from solar energy over the next decade.

“Crudely speaking we’re expecting to see US$300bn of issuance in 2018. I think China is going to be about US$80bn, and I think that will come quite quickly from the development banks involved. In 2020 our objective – not so much projection – is US$1trn of issuance,” said Sean Kidney, CEO of the Climate Bonds Initiative, speaking at an IFR seminar in Singapore on June 22. “That will be a material contribution.”

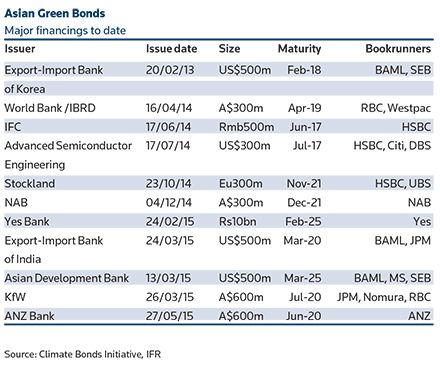

Global Green bond issuance tripled in 2014, according to the CBI, reaching US$36.6bn. So far, however, that growth has come from Europe and the US. Only a handful of issuers in Asia Pacific – including the Asian Development Bank and two Australian banks – have sold Green bonds to date, and market participants face a challenge in convincing others to embrace the concept. (See Table.)

Asian Green Bonds

Asian issuers see the format as an increased cost that produces no tangible benefit, while many of the region’s biggest investors have yet to establish socially responsible investment portfolios.

“In general, Asian investors are not as far along as European and Scandinavian investors in their Green investment strategies, but there is definitely a lot of interest in the region and we are seeing some movement from investors,” said Samantha Sutcliffe, Green bonds principal for Asia & the Middle East at SEB, a bookrunner on Asia’s first Green bond from Export-Import Bank of Korea in 2013. “We believe that growth will come alongside the increase of Asian Green Bond issuers.”

Not there yet

The challenges to developing this market are by no means unique to Asia.

The CBI defines Green bonds as financings for projects with a positive environmental impact, and tallies all bonds labelled as “green” whether or not they come with any third-party verification. Even that definition, however, is a touchy subject for some.

When it comes to defining a project as “green”, it is also proving hard to agree global standards. Are electric trains still green if they are run off a coal-fired grid? Can an oil company ever issue Green bonds, even if the proceeds are ring-fenced for an environmental project?

The Green Bond Principles, agreed with a quorum of market participants and overseen by the International Capital Markets Association, call for issuers to appoint independent verifiers to assure investors in each deal that the proceeds will be put to good use – a requirement that some issuers see as an unnecessary expense.

The CBI and others are working hard to promote global standards, but guidelines are voluntary and there are no penalties for issuers who fail to comply. The bigger SRI funds, many of which are based in Scandinavia, may be prepared to place that kind of trust in a European issuer, but the same approach may not fly in Asia.

One recent Asian issuer described the process as far more rigorous than expected, with lengthy questioning from global green funds as to the precise use of proceeds.

Those green funds are predominantly European, driven by a mandate from pension investors and individual savers to avoid carbon-intensive industries and promote green growth. That suggests Asia’s price-sensitive issuers will need to pay for external consultants to vet their projects – without any immediate benefit to their cost of funding.

Sutcliffe at SEB argues that the hard work involved in a debut issue can pay dividends later on.

“We often find that companies already have the information needed for reporting. There is some extra work involved in presenting that information in a way that suits Green bond investors, but once the process is in place future transactions become more straightforward,” she said.

In Asia, recent deals have hinted at a brighter future. The ADB’s US$500m 10-year benchmark in March confirmed that Green bonds price flat to conventional credit curves, while Export-Import Bank of India and Yes Bank each increased their deal sizes after receiving a strong response.

Still, without a homegrown investor base, the real catalyst for Asian Green bonds may come from government policies.

Indian and foreign businesses are rushing into the solar sector after Prime Minister Narendra Modi announced his ambitious target for renewable energy.

Adani Group announced a 5GW solar park in Rajasthan, part of a plan to generate 10GW from solar power by 2022.

Bharti Enterprises and Japan’s Softbank in June announced plans for a US$20bn joint venture to develop renewable energy projects, including at least 20GW of solar power. Taiwanese manufacturer Foxconn will be a minority partner.

US-based SunEdison and First Solar have each announced plans to build solar plants in India.

At a total cost of around US$100bn, an extra 100GW of solar energy will require financing from more than just the banking sector, where lenders are already under pressure to boost their capital or trim risk-weighted assets to meet Basel III requirements.

The government has already asked infrastructure financing companies to issue Green bonds to help spread the burden.

Yes Bank, which has committed to funding 5GW of renewable energy under Modi’s plan, was the first mover, with a Rs1bn (US$157m) Green bond in February.

Export-Import Bank of India followed in March with a US$500m deal, the country’s first in US dollars, and bankers are busy pitching for similar mandates. Most of India’s biggest banks have pledged to fund a minimum amount of solar infrastructure – as much as 15GW in the case of State Bank of India – and the likes of Power Finance Corp and Rural Electrification Corp are also expected to issue.

Change in China

The People’s Bank of China and the United Nations Environment Programme published a joint report in April on the establishment of a green financial system in China that called for the use of Green bonds among a diverse range of financial products, even naming Industrial Bank as the first issuer of Green bonds in China – a deal that market participants will be watching closely.

The report listed the development of Green bonds among its 14 recommendations. For Green bonds specifically, key recommendations included establishing the scope of Green bonds, creating incentives and setting up a tracking and evaluation system.

HSBC climate change strategist Wai-Shin Chan sees vast potential for Green bonds as China works to clean up its environment.

“Only around a third of environmental financing comes from the government, so Green bonds could bridge some of the balance and help China channel additional money into green projects,” said Chan.

China’s control of its financial system gives policy makers the opportunity to create a big market for green instruments from scratch. Doing so, however, will require careful planning.

“We have not seen bottom-up demand in China, so the government needs to incentivise issuers and investors with appropriate regulation,” said Chan.

China’s central bank is working on a draft framework for Green bonds, and market participants expect further clarity later this year when the government unveils its thirteenth five-year plan.

Measures may include tax breaks for green investments or a shift in energy policies to promote low-carbon power and tackle pollution, but China faces a challenge in bringing together the many different regulators that oversee various parts of the domestic bond markets.

Once regulations are in place, Kidney at the CBI believes the first Chinese issuers will target overseas investors, while the local market will ultimately account for the vast majority of Green issuance.

Chan and credit analyst Desmond Kuang said in a July 6 report that policy banks, local governments and corporations could all become major issuers, while they expect the National Social Security Fund to be a “champion” investor to showcase the government’s support for Green bonds.

Sutcliffe at SEB sees China having a positive impact on the wider region.

“If China can unlock climate financing, including Green bonds, there is clearly huge potential for that market. It would show leadership for the region as a whole and help speed up Green bond issuance,” she said.

The debate around the virtues of Green bonds often focuses on the question of additionality – whether the instruments actually encourage any new investment in climate-sensitive projects. Critics argue that Green bonds merely provide window dressing for existing loans, while others believe that is a necessary starting point that will encourage other investors and governments to rethink their own strategies.

In Asia, where environmental awareness is growing fast, demand for green investments has the potential to shape the region’s response to climate change.

“In the longer term, more funds being actively deployed for green purposes would be a signalling mechanism for governments to develop more concrete environmental policies,” said Chan at HSBC. “That creates a virtuous circle, as stronger policies would in turn attract more investors.”

To view all special report articles please click here and to see the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.