Lower oil prices have given many Asian economies a welcome lift, but policymakers can do more to capitalise on the opportunity by putting their energy savings to good use.

Conventional wisdom says that lower oil prices should benefit Asia. As most countries in the region are net importers of oil and gas, they stand to save on energy bills, while those that run expensive fuel subsidies are enjoying a double lift.

However, the slump in global energy prices has also presented a rare opportunity for policymakers to boost development agendas. Diverting oil savings into infrastructure and social projects allows cheaper energy to be a catalyst for faster development.

“When commodity prices are high, we notice that commodity-rich countries often have trouble diversifying their economies,” said Shang-Jin Wei, ADB chief economist. “When the commodity sector is booming, it tends to absorb resources and labour, which pushes up wages in manufacturing.”

High exchange rates, often a result of strong commodity exports, have also foiled efforts to diversify for countries like Brazil. However, with oil prices much lower, Asian economies now have a rare opportunity to rebalance.

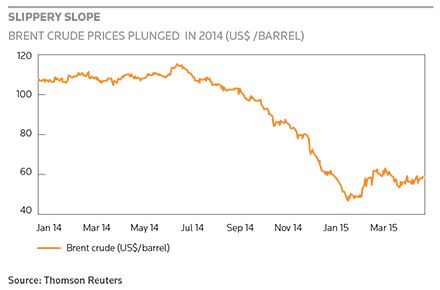

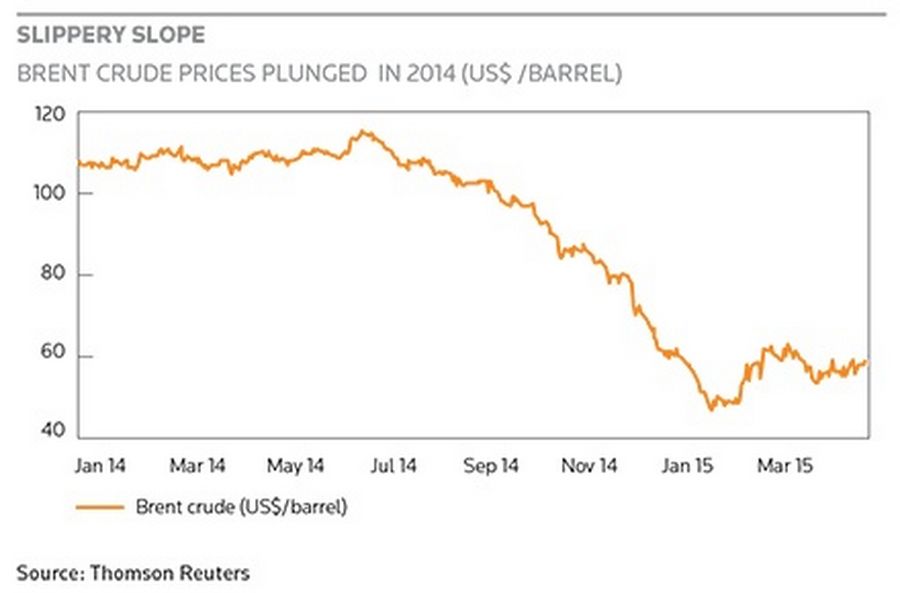

Slippery slope

“Those countries that manage to use this opportunity to develop a competitive manufacturing sector could, at the end, be in better shape even when prices go back up,” said Wei. “You want to be like Norway, rather than Nigeria. Nigeria’s economy is 80% petroleum. Norway has a lot of oil, but it also has a very competitive, modern service sector.”

Rebalancing any economy takes time, but economists are already welcoming moves to cut subsidies and promote fiscal stability.

Barclays analysts estimate that India, Indonesia and Malaysia – the three main fuel subsidy providers in the region – can save a cumulative US$30bn in related outlays. Indonesia is the biggest beneficiary, according to Barclays, saving around US$16bn relative to its 2014 budget.

“Most countries in Asia will benefit from the lower oil price, but its biggest impact is seen in India and Indonesia. In both economies, lower oil has solidified the paths of reform, inflation and growth,” wrote David Fernandes, Wai Ho Leong and Rahul Bajoria in a March research note.

Indonesian president Joko Widodo trimmed fuel subsidies in November before abolishing them altogether on January 1, linking prices to global fuel costs each month and wiping out a Rp250trn (US$19bn) expense from the national budget. Without the subsidy, petrol prices actually fell to Rp7,600 a litre in January and Rp6,700 in February. The April price has been fixed at Rp7,400.

India cut its diesel subsidy last October and now expects to spend 50% less on petroleum subsidies in 2015-16, compared to the Rs602bn (US$9.6bn) bill for the fiscal year to March 31.

Malaysia abolished fuel subsidies in December, removing an expense that had taken up 3% of GDP, or around 11% of all government spending, according to Moody’s. It will see less of a benefit, however, since lower prices also mean lower fiscal revenues from its substantial oil-and-gas exports.

China, Asia’s biggest oil consumer, has also used the opportunity to raise taxes on petrol and other hydrocarbons, in a move, it says, will help target pollution and stimulate renewable energy sectors.

“Even when oil prices are high, fuel subsidies don’t do what the policy is intended to do, which is to help poor people. The problem with a subsidy on fuel is that it seldom targets the poor very well. So, a big chunk is wasted. In Indonesia, my back of the envelope calculation says that, perhaps, two thirds or even three quarters do not reach the people they intend to help,” said Wei.

In order to capitalise fully on the savings, however, governments need to be reallocating those resources to more productive uses.

“For many countries, I think it will act as a catalyst. You need the government to come to that understanding, and a relatively flexible labour market and financial market, so that reallocating resources across sectors is feasible and not too costly,” said Wei.

“This is a good time to act. Reforms that are generally not easy to do become somewhat easier.”

India’s pro-business government has unveiled big investments in railways, highways and urban infrastructure projects, while Indonesia is upgrading its refineries, ports and roads. Central banks have also been able to ease monetary policy without stoking inflation. In the medium term, bankers expect those reforms to translate into improved fiscal positions and, potentially, higher credit ratings.

“We expect the oil growth dividend to be felt much later – in H2 2015 – as lower oil reignites demand in the G3 economies, paving the way for an export-led resurgence in Asia,” the Barclays analysts wrote. “As growth momentum improves, both India and Indonesia could be primed for credit re-ratings, amid improving fiscal and external positions. We expect India to achieve a two-notch upgrade by 2017, while Indonesia could find favour from rating agencies by the end of 2015.”

Ultimately, however, governments also need to be wary of banking on low energy prices for too long. Oil prices have the potential to rebound just as quickly as they fell and some analysts feel the current market price is unsustainable in the long term.

“Overall, you can make the argument that fuel prices are actually too low,” said Wei. “If you levy the same tax on fuel as on other goods and services, then you’re not fully taking into account that fuel consumption and incremental emissions can have negative long-term consequences for future generations.”

“If a country is able to do it, this can even be an opportunity to raise fuel taxes in order to promote conservation, to encourage firms and households to reduce overall emissions.”

To view all special report articles please click here and to see the digital version of this report please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com .