A bumper year for equity offerings shows investors are still keen to add Indian exposure, despite troubles elsewhere in Asia.

India’s equity capital markets are set for the biggest year in a decade, with a boost from the comeback of IPOs and a string of mega stock offerings at a time when the rest of Asia is struggling to recover from the Chinese stock-market debacle.

At the end of the third quarter, total ECM issuance stood at Rs1.2trn (US$18.5bn) from 104 transactions, according to Thomson Reuters data.

The IPO market, in a deep slumber for the last couple of years, has sprung back to life. According to the Securities and Exchange Board of India, 29 companies have raised Rs48bn through IPOs so far in 2015, compared with Rs4.6bn from 11 floats in the same period last year.

Listings that had been in the works for years, such as Adlabs, Inox Wind and VRL Logistics, finally managed to come to fruition.

“The capex cycle will take another quarter or two to revive as various government initiatives to kick start the economy reach the ground level. We will see a spike in capital-raising activity once that happens,”

“At the start of the year, the volume was expected to be around US$20bn–$25bn. Activity is likely to remain sustained in the fourth quarter and we expect to end the year at the bottom of that range,” said Arvind Vashistha, head of ECM origination at Citi India.

India really stood out in the volume of secondary offerings, demonstrating its appeal even because global investors shunned most emerging markets as a result of the fall in the Chinese stock markets and expectations of US rate hikes.

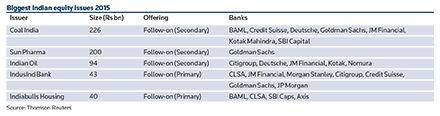

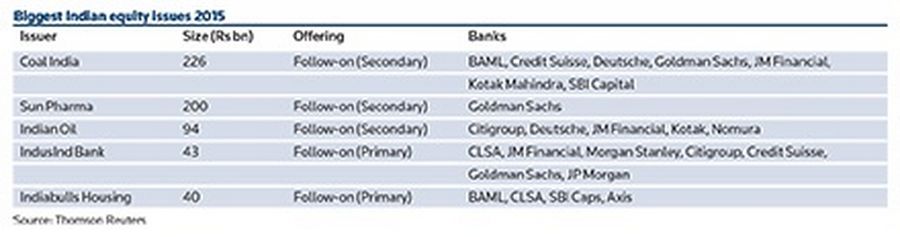

The government raised Rs16.8bn through an offer for sale of shares in Power Finance Corporation in July and Rs94bn from a similar disposal of stock in Indian Oil Corporation in August. In September, Indiabulls Housing Finance conducted a Rs40bn qualified institutional placement during a brief window of opportunity. Later in the month, after the Federal Reserve kept interest rates unchanged, Tata Steel placed a Rs12.5bn block in Tata Motors.

Investors responded well to all these share offerings, although they were tightly priced at discounts of 2%–4%, and have traded well.

High expectations

At the beginning of the year, some bullish bankers had predicted that Indian ECM volume might even overtake that of China. However, this quickly proved overly optimistic and, in the first nine months, China’s ECM volume was way ahead at US$114bn, with the help of a first-half bonanza.

“ECM transaction volumes are, perhaps, not as robust as we expected at the start of the year. Global market conditions have contributed to that, given the volatility issuers have had to deal with,” said Sanjeev Jha, head of capital markets (India) at Bank of America Merrill Lynch.

In addition to global factors, India’s lower-than-expected economic growth may also have also kept down corporate funding requirements, resulting in weaker-than-projected follow-on offering volumes.

Jha, however, thinks it is only a matter of time before activity starts to pick up.

“Perhaps, the capex (capital expenditure) cycle will take another quarter or two to revive as various government initiatives to kick start the economy reach the ground level. We will see a spike in capital-raising activity once that happens,” he said.

Modest IPOs

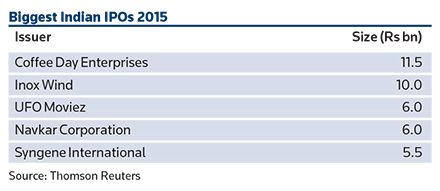

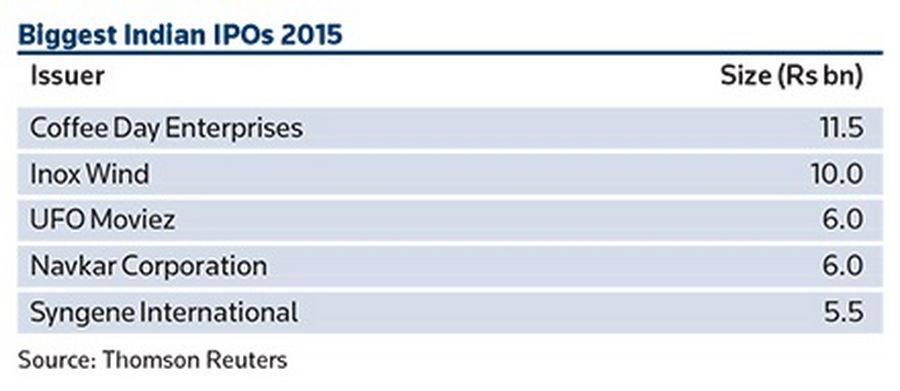

Also, while activity has picked up, most IPOs are in the US$50m–$100m range, the largest to date being that of Coffee Day Enterprises for Rs11.5bn (US$177m). Others, such as Ortel Communications, Adlabs Entertainment and Prabhat Dairy, had to trim the sizes of their IPOs because of weak investor response.

That, however, may be a healthy sign, says Biswajit Chatterjee, partner at Squire Patton Boggs, because it shows that even “mom and pop investors have become more careful”. Still, “some IPOs have done much better than expected even in volatile markets.”

V Jayasankar, head of ECM at Kotak Investment Banking, says the typical IPO size will remain in the US$75m–$200m range due to the nature of the Indian companies wanting to raise money from the capital markets.

A larger IPO currently in the pipeline is that of Interglobe Aviation, which aims to raise Rs30bn (US$462m). If it crosses the finish line, it will be India’s largest IPO since Bharti Infratel’s Rs41bn float in 2012.

Biggest Indian IPOs 2015

Phased-out disinvestment

The pace of disinvestment in state-owned companies has been slow, with cheaper oil prices removing some of the pressure for fiscal-deficit reduction and investor sentiment definitely mixed.

Biggest Indian equity issues 2015

The 10% stake sale in Coal India in January for Rs226bn set a record as the largest equity offering on record in the country and attracted both local and global investors – thanks to an appealing 5% discount.

However, the government misjudged the timing of a Rs94bn sell-down in Indian Oil, launched in late August during the Asian stock market turmoil. As a result, state-owned Life Insurance Corporation ended up buying most of the 10% stake.

The government has also struggled to line up underwriters for its usual nominal fee of Rs1. A poor response from banks at the beginning of the year resulted in the auctions for Indian Oil and NMDC being delayed.

The auction process was subsequently modified to make it possible for banks would have to bid for mandates encompassing a basket of companies instead of a single one.

The first attempt at bundling attractive sell-down candidates, with less attractive ones met with a mixed reception. Deutsche Bank was the only foreign bank to participate in the bidding process and the government eventually had to scrap one of two baskets it had assembled as there were not enough bidders.

Deutsche Bank, Edelweiss, ICICI Securities and SBI Capital were hired to handle the so-called Basket 2, aimed at selling stakes of 5% in Bharat Electronics, 5% in NTPC, 10% in Engineers India, 10% in National Aluminium and 15% in Hindustan Copper. At current prices, the transactions will total a maximum US$1.5bn.

Reform agenda

Basket 1, made up of stakes of 10% in Oil India, 5% in Container Corporation, 10% in NMDC, 15% in MMTC and 12% in ITDC for a maximum of US$1.5bn, was scrapped.

In order to introduce the new bidding process, the government has also had to do away with its nominal Rs1 fee and will end up paying around Rs185m to the banks mandated for Basket 2.

How 2016 pans out will depend largely on the effect of government reforms on the economy. Citi India’s Vashistha is of the view that larger follow-on offerings will materialise only when the investment cycle picks up. “Global headwinds should recede and there has to be continuous reform momentum and regular monetary easing,” he said.

Planned economic reforms include bills on the Good and Services Tax and Land Acquisition, which the government wants parliament to pass into law next year.

Kotak’s Jayasankar, who is cautiously optimistic about the market, says investor interest is likely to be strong in share issues from the consumer, healthcare and banking sectors. In infrastructure, the port and road sectors are likely to remain popular. In the power industry, while the traditional thermal and hydro power sectors continue to face uncertainty, the green energy sector has the potential to grow.

Even though currently cash-rich domestic funds have offset the impact of selling by foreign funds since August, India is not immune to global market conditions.

“While India stands out in the emerging markets basket, it will be wrong to say that we will not be impacted by a broader emerging-market correction,” Jha said. “However, once the uncertainty over the FOMC actions declines and emerging-market funds start seeing a reversal, we will not be surprised to see India getting a disproportionate share of those funds.”

To view all special report articles please click here and to see the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

| Biggest Indian IPOs 2015 | |

|---|---|

| Issuer | Size (Rs bn) |

| Coffee Day Enterprises | 11.5 |

| Inox Wind | 10 |

| UFO Moviez | 6 |

| Navkar Corporation | 6 |

| Syngene International | 5.5 |

| Source: Thomson Reuters | |

| Biggest Indian equity issues 2015 | |||

|---|---|---|---|

| Issuer | Size (Rs bn) | Offering | Banks |

| Coal India | 226 | Follow-on (Secondary) | BAML, Credit Suisse, Deutsche, Goldman Sachs, JM Financial, |

| Kotak Mahindra, SBI Capital | |||

| Sun Pharma | 200 | Follow-on (Secondary) | Goldman Sachs |

| Indian Oil | 94 | Follow-on (Secondary) | Citigroup, Deutsche, JM Financial, Kotak, Nomura |

| IndusInd Bank | 43 | Follow-on (Primary) | CLSA, JM Financial, Morgan Stanley, Citigroup, Credit Suisse, |

| Goldman Sachs, JP Morgan | |||

| Indiabulls Housing | 40 | Follow-on (Primary) | BAML, CLSA, SBI Caps, Axis |

| Source: Thomson Reuters | |||