Asia’s bond market veterans may be patting themselves on the back for lifting the region’s debt markets to new heights, but not everyone is so easily impressed. IFR Asia’s resident debt market columnist looks at the real reasons behind a record-breaking year for Asian bonds.

Was 2012 as good as it gets for Asia in the G3 bond markets? The answer hinges on whether you’re of the belief that this record-breaking year for new issues represents secular – and sustainable – market growth, or if it is simply inflating a bubble that is set to burst with inevitably painful consequences for all concerned.

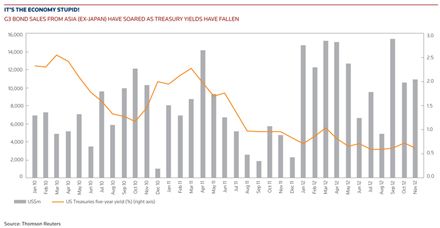

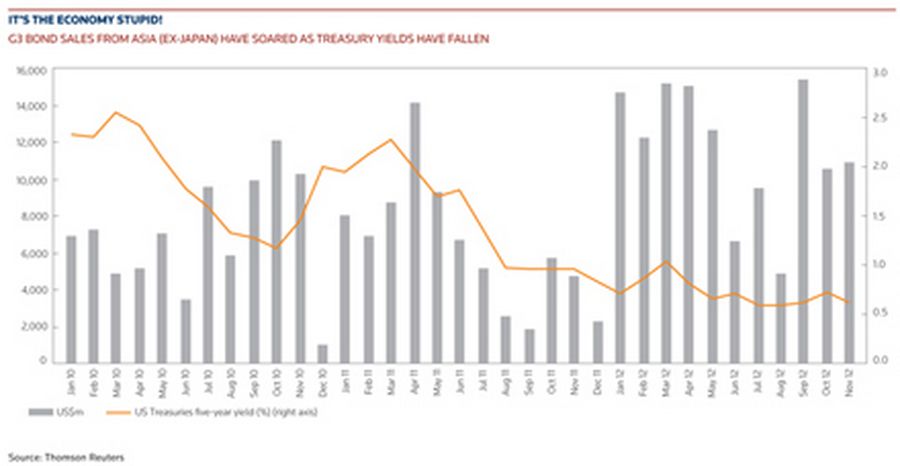

Time, of course, will tell. Yet, there can be little doubt that one element of the debt equation – the US rate curve – was a crucial component of the perfect storm for Asia’s G3 markets in 2012.

The fact that Asian issuers (excluding Australia and Japan) placed US$134bn of new debt against the backdrop of some of the loudest headline noise yet out of the eurozone and low-octane growth in the US, China and India was nothing short of remarkable, and there was no repeat of the eurozone-inspired market shutdown of late 2011. Indeed, if 2012 was anything, it was the year that 2011 should have been, with eurozone fatigue, perhaps, explaining why the Asia G3 juggernaut has kept rolling along so relentlessly.

Undoubtedly, the credit component came of age in Asia’s primary markets this year, with unrated paper, perps and challenging high-yield and credit-enhanced issuance managing to cross the line. However, 2012 would have been different had the US Treasury market not spent the year drifting down to yields not seen since the Second World War.

In the process, the global “quest for yield” became a well-worn cliché, used to explain why so many new issues were coming to the market, and why they were greeted with such dizzyingly high order books – whether in Asia, or North and Latin America. Investors didn’t want the microscopic yields available on Treasuries, so they went for anything that gave them something above that. In those circumstances, investment grade became effectively a proxy for US Treasuries and was the easiest asset class for syndicate bankers to bring to market.

The ease with which deals priced was in part a reflection of the fund inflow dynamic that was in place for much of the year. As of November, according to research firm EPFR, emerging-market funds had registered their 21st week of inflows, with EM-dedicated bond funds averaging inflows of around US$600m per week.

Also, in a year when Asian private-bank portfolios weighted fixed-income more heavily over equity than before, the bid was there for anything offering an optically attractive return.

Doomsayers claim that the PB bid is a toxic phenomenon, rooted in rebates bookrunners paid to wealth managers, leverage offered to customers and the cause of the rampant book inflation that was 2012’s signature theme.

Private parties

Moreover, they envisage that, when the rate cycle turns and a full-scale portfolio switchback into equities occurs, the PB bid will quickly evaporate. That would help hammer the secular growth theory, but, as the year comes to a close, there’s no sign of that bid retreating.

This was starkly evident in one of the year’s most “risk-on” propositions: a US$500m unrated perpetual from China’s Shui On Land. Some 55% of that trade went into the hands of private banks in early December, marking the culmination of another seemingly unlikely phenomenon in 2012 – the return of the China property bond.

After the bloodbath in China property stocks and bonds in October 2011 – stemming from fears that the sector was in hock to China’s shadow banking industry at sky-high rates and facing an insurmountable refinancing burden – issuance from the China property companies dried up. To many, a revival was unthinkable, in the face of not only the refinancing pressure, but also contracting sales and declining prices. In the end, China’s property companies managed to get financing onshore and hoarded cash, while sales and prices picked up.

Just as it rounded off the China property issuance year, Shui On also reopened it in launching a US$400m three-year in February, flamboyantly defying the sceptics with two further taps of the deal and paving the way for further issuance from the sector.

If anyone needed reminding that capital markets are subject to changing fashions and fads, then the sharp decline of Dim Sum issuance in 2012 certainly did the trick. This is not to suggest that the market has died with a bang, but it has certainly been reduced to a whimper now that investors no longer regard the renminbi as a one-way appreciation bet.

Frankly, although there was long-tenor issuance in the Dim Sum market this year, the inability of issuers to book long-dated swaps in renminbi was always going to be a natural brake on issuance in that market. It will take the opening up of China’s capital account and the full convertibility of the renminbi before that happens – both of which are some years away.

This year, the standout domestic market in Asia was Singapore, and judging by the spate of perpetual bonds, the longest-dated format possible seemed to hit the sweet spot. With the city’s banking system awash with offshore cash seeking a safe haven, it’s not too surprising that the Singapore-dollar market received a shot in the arm. Whether or not this ticks the secular growth box, of course, is anyone’s guess, but there’s no doubt that size and tenor are now available – to issuers both from Singapore and beyond.

The Singapore market became a surprising fundraising venue for liquidity-starved European banks, with ABN AMRO blazing a trail last October via a S$1bn (US$820m) Lower Tier 2 deal that demonstrated the Lion City’s ability to deliver chunky deal sizes with onshore liquidity building an overwhelming S$17bn order book.

This year, the standout domestic market in Asia was Singapore, and judging by the spate of perpetual bonds, the longest-dated format possible seemed to hit the sweet spot.

Still, the trade remained anchored in the arbitrage back to floating-rate dollars, with the Dutch bank saving 55bp versus its implied cost of US-dollar funding.

The ability of Asian issuers to attract capital from within the region was a crucial development in the debt markets in 2012. The heavy oversubscription from Asian investors on sizable Reg S-only deals was telling, gripes about the padded PB bid notwithstanding. US investors are also increasingly willing to put in the credit work on Asian names, with many now conducting their research and investments out of Hong Kong or Singapore, with the likes of fund giants Loomis Sayles and T. Rowe Price having recently set up shop in the region.

Nevertheless, when it came to high yield, not every name could cross the line and there were some signal failures – especially where investors saw the faintest outline of hair on the credit. As Asian corporate balance sheets weaken in the face of structurally lower long-term growth, the offshore high-yield market will become more crucial to meeting corporate Asia’s funding needs.

This region’s corporate treasurers will be hoping for another banner year in 2013. It has to be asked, however, what the odds are of another perfect storm for the second year in a row. As they did this year, US Treasury yields hold the key to the outcome.

To see the digital version of this report, please click here.