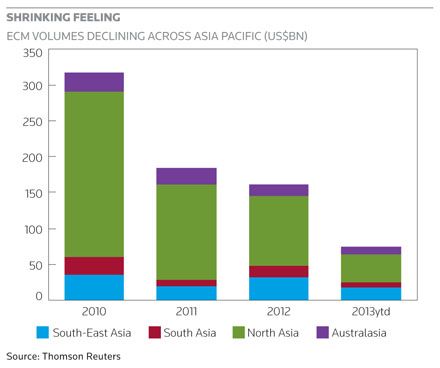

The hunt for yield has proven as important in Asia’s equity capital markets as it has in the region’s booming bond markets, with REITs and similar plays generating huge interest. Those dynamics, however, are changing as investors review their allocation strategies.

Source: Reuters/Ajay Verma

Labourers sift wheat crop at a wholesale grain market in the northern Indian city of Chandigarh.

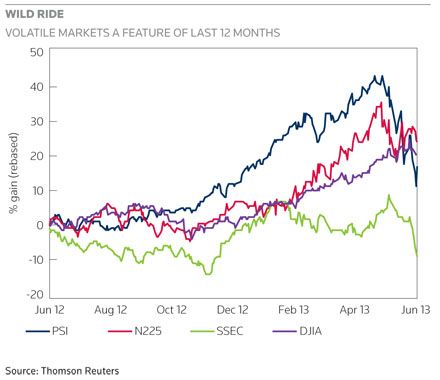

Asian equities are tumbling into the second half of the year as a shock from shifting US monetary policy and ill winds in China take hold, frustrating investors seeking yield in the region’s markets.

The signs of pessimism are difficult to ignore: On June 26, gaming company Macau Legend Development slashed the size of its planned US$788m initial public offering in Hong Kong by more than half. And two other Hong Kong IPOs have been delayed.

Much of the recent trouble began in late May. Asian equities – historically a beneficiary of US quantitative easing – reeled on May 22 when US Federal Reserve Chairman Ben Bernanke warned the Fed wouldn’t throw money at the US economy forever.

“The market response has been pretty emphatic,” said Peter Elston, head of Asia Pacific strategy and asset allocation at Aberdeen Asset Management. “It’s a bit like a drug addict being told by his drug pusher that at some point he’s not going to get any drugs any more.”

The loss of these ‘drugs’, coupled with signs of slowing growth in China, has unleashed a sea change in investor attitudes toward Asian equities. From May 22 to June 25, Japan’s Nikkei has fallen 17%, while Hong Kong’s Hang Seng has slumped 15% and the MSCI Asia ex-Japan has declined 14%.

That turbulence looks likely to persist through the second half of the year. On June 19, Bernanke laid out a roadmap for ending the Fed’s unprecedented stimulus policies. The Fed could begin to scale back its US$85bn a month bond purchases later this year and halt them by mid-2014, he said. The yield on the 10-year Treasury has since touched 2.61%, its highest in almost two years.

Underweight Asia

Asia’s financial markets are particularly vulnerable to “tapering” signals, said Stephen Hull, head of client solutions for Asia ex-Japan at BlackRock. For this reason, the asset manager’s portfolios are “slightly underweight” on the region’s equities.

“We like the long-term structural growth offered by Asian equities, but markets here have been driven partly by the stimulative monetary policy environment in the US,” Hull said.

“A gradual withdrawal of QE in the US implies higher US yields and a strong US dollar. Historically, such trends have led to more challenging prospects for Asian assets.”

Hull’s views are backed up by a June survey of 248 fund managers conducted by Bank of America Merrill Lynch in the wake of the market turmoil. Global fund managers cut their exposure to Asian and other emerging market equities to the lowest level since December 2008, the poll showed.

And a quarter of those surveyed said that emerging markets were the regions where they would most like to be underweight in the coming 12 months.

The performance of stock markets across the region will ultimately hinge on how Asia’s economies adapt to the end of ultra-loose monetary conditions and to the reversal of capital flows that those conditions have triggered. How well they can do so won’t be clear for at least another few months, according to Aberdeen’s Elston.

“That will determine what happens with equities – whether this downturn is prolonged or whether we’ll see some sort of recovery,” he said.

Aberdeen’s Asian Multi Asset Fund is currently underweight Asian equities, with 35% invested in the asset class compared to a 40% benchmark.

The China factor

China isn’t helping matters, either. The world’s second-largest economy – which long dazzled investors with years of double-digit growth – is now predicted to deliver just 7.7% GDP growth in 2013, according to a June World Bank report.

Activity in China’s manufacturing sector, as measured by HSBC’s Flash Purchasing Managers’ Index, hit a nine-month low in June, reinforcing signs of weaker second quarter growth. And the slowing growth trajectory has led Capital Economics to lower its 2013 growth forecast to 7.5% from 8% and 2014’s forecast to 7.0%.

Figures indicating a slowdown in China are also exacerbated by long-held fears about the country’s economic foundations, including its accounting and corporate governance standards. Investors are now worried about how China will wean itself off an investment and credit driven economic model and transition to a more balanced, consumption-led economy.

“The question is: can they do this painlessly? I suspect not,” said Aberdeen’s Elston.

The investors surveyed by Bank of America Merrill Lynch identified a China hard landing and commodity collapse as the greatest tail risk – surpassing even the failure of Japan’s reflationary policies, an EU banking crisis or US fiscal tightening.

“We’ve been very sceptical about China for many years,” Elston said. “Yes, from an economic perspective it’s been a strong story but when it comes to finding good investments it’s a disaster. It’s always been somewhere we have been underweight.”

For some market makers, however, the gloomy outlook for China-linked assets makes a compelling contrarian play.

“The lows in emerging-market equity and commodity allocations suggest the market has over-positioned itself for a shock from China,” said Michael Hartnett, chief investment strategist at Bank of America Merrill Lynch.

Dividend stocks lose allure

China gloom, coupled with the end of an ultra-easy monetary policy, is likely to dampen the ‘yield hunt,’ a dominant theme for the region’s equity markets.

REITs and similar yield-driven stocks have accounted for a spate of public offerings in Hong Kong and Singapore as investors showed a clear preference for income-generating assets. In March, Mapletree Greater China Commercial Trust – whose assets include a mall in Hong Kong and offices in China – soared more than 10% on its first day of trading after its US$1.3bn Singapore IPO.

Now, the changing market dynamics mean that even these yield-driven stocks are losing some of their allure. Hong Kong’s REIT Index has shed 16% since May 22, more than the Hang Seng’s 15% drop over the same period.

“Yield as an investment determinant makes more sense when investors are searching for yield or safety than when the global economy is on a cyclical recovery and growth is a more sought-after attribute,” said Nomura Asia ex-Japan strategist Mixo Das.

“Given our expectation of higher bond yields, it would mean that yield stocks remain out of favor.”

This could cast a pall over the upcoming US$1bn Hong Kong IPO of three hotels by New World Development and the REIT IPO planned by Overseas Union Enterprise, which aims to raise US$638m in Singapore.

However, HyungJin Lee, head of Asian equities at Baring Asset Management and manager of the its Asia Growth Fund, is not so quick to dismiss a strategy that has served many investors well during the low-interest rate environment of the past three years.

“Even with all this talk about tapering, they (interest rates) are likely to remain on an absolute basis very low for yield investors in general,” Lee said.

Value emerging?

Undeterred by the white-knuckle ride over the past month, a few investors are cautiously re-entering the market, with some Asian stocks seen offering good value.

The MSCI Asia ex Japan index is currently trading at 9.9x forward earnings, about an 18% discount to its long-term average.

“Asia still offers high structural growth in a low-growth world,” said Marc Desmidt, head of alpha strategies for Asia Pacific for BlackRock.

BlackRock believes South Korea and its export-focused companies could benefit from accelerating global growth and a stronger dollar, while ASEAN countries like Thailand, Philippines and Indonesia boast a growing consumer class that makes hypermarket operators and real estate developers attractive.

That’s a view shared by Lee at Barings. He likes South Korea’s global brands like technology firm Samsung and automaker Hyundai and is overweight on Southeast Asia. While neutral on China overall, he favours healthcare companies that will benefit as the country’s aging population increases its spending on health.

“In the long-term, it’s a good entry point. Asian equities are cheap on a relative basis and absolute basis,” said Lee at Barings.

The Nikkei’s dramatic fall from its May peak has led to speculation of a reversal for Japanese stocks, but the country may still be a source of good returns if Abenomics delivers as promised.

Elston at Aberdeen Asset Management said that Prime Minister Shinzo Abe will likely outline further economic reform if the ruling Liberal Democratic Party secures a majority in the upcoming July elections.

“It is a very bold strategy and got a lot of people excited. I suspect he will come out with more detail of the third arrow of plans to restructure the economy and I think that could probably see a bit more interest return to the market.”

However, Elston cautions that longer-term demographic forces and a conservative business culture make Japan a tricky bet: “As an investor, you have to be very nimble playing these short-term themes relating to what’s going on in the political front.”

Moderating growth in China, the end of cheap money and the associated change in fund flows will make the second half of 2013 a testing time.

But investors see reasons for optimism once the storm passes. While a strong dollar has traditionally had a negative impact for Asian markets, a strong dollar in the context of more robust global growth should be positive for the region, making companies more competitive.

“It’s a process of readjustment to a different economic landscape,” said Lee at Barings.

“That’s the cause of the short-term volatility but as the global economy recovers– albeit at a very gradual pace – Asia will benefit.”

To see the digital version of this report, please click here.